Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

The Central Bank of Nigeria (CBN), through its Monetary Policy Committee (MPC), last weekend, held all rates steady, in a decision that doused the tensed environment, which was stoked by anticipation of devaluation and rate hike in several quarters.

The Central Bank of Nigeria (CBN), through its Monetary Policy Committee (MPC), last weekend, held all rates steady, in a decision that doused the tensed environment, which was stoked by anticipation of devaluation and rate hike in several quarters.

Specifically, the Monetary Policy Rate (benchmark interest rate) was retained at 13 per cent with a corridor of +/- 200 basis points around the midpoint and the Cash Reserve Requirement (CRR) at 31 per cent too.

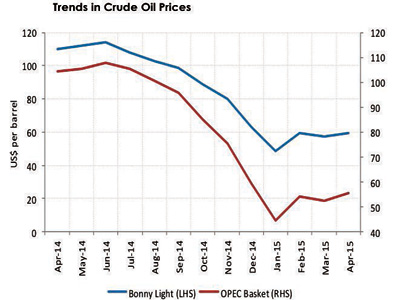

The apex bank , in reaching this decision, said it considered the underlying fundamentals of the economy, the evolving international economic environment, developments in oil prices, as well as the need to allow the unveiling of the economic agenda of the Federal Government.

Of course, the lingering inauguration of the Presidential cabinet and non-definite decision over the protracted fuel subsidy, as well as the volatile crude oil prices, coupled with the security issues and recent record of vandalisation of oil installations is surely keeping some investors on the sideline. The mention of the planned devolution of the powers at the Nigerian National Petroleum Corporation, though strategic, is all encompassing and as such, may not hit the ground running.

Analysts and market operators have corroborated these views as they said decisions on cabinet selection, subsidy, security and the mimed regrouping by militants, have a direct bearing on the future of the foreign exchange developments, the position-taking of investors and foreign direct investments’ inflow.

The domestic economic front has already been hit with several headwinds. For example, CBN Governor, Godwin Emefiele, lamented the adverse effect of the sliding global crude oil prices on the fiscal position of government, which is becoming increasingly obvious.

Also speaking on the steady rise of inflation, Emefiele stressed that some of the drivers of the current inflationary pressure on consumer prices are transient and outside the direct influence of monetary policy.

Specifically, he said that the resurging inflation reflects a rise in both the core and food components of inflation and traceable to transient factors such as energy, arising from scarcity of petroleum products around the country and poor electricity supply and these challenges are expected to be part of the changed economic plan.

“Early resolution of fuel scarcity would dampen transportation costs and improve food distribution across the country, while improvements in electricity supply could steady output at lower costs.

“Some of the reassuring measures of the administration, including efforts aimed at resolving fiscal challenges at the sub-national levels, and the fight against corruption and improving the business environment would unlock the inflow of foreign direct investment,” Emefiele said.

In recent times, the equities market has been on a free fall due to political and macroeconomic headwinds. For example, the All Share Index (ASI), between the inauguration of President Muhammadu Buhari till date, has shed 8.7 per cent.

Afrinvest Securities Limited in a note to The Guardian said: “Vague policy direction by the new administration leaves investors uncertain about equities investment. Also, lower global oil prices, that weakened the revenue base of the Federal Government since late 2014, remained a concern to investors. Closely linked to the above is the devaluation and continuous depreciation of the naira- mostly at the parallel market, amid apex bank’s efforts to conserve the external reserves.”

But analysts at WSTC Financial Services Limited said the decision of the Monetary Policy Committee (MPC) to maintain status quo despite the growing inflationary pressures and increasing volatility in the parallel segment of the foreign exchange market underscores the fact that the apex bank is getting to the limits of monetary policy options at its disposal.

“We believe the CBN may remain incapacitated in this way until there are clear policy directions from the fiscal side of economic management (government), particularly on issues bordering on fuel subsidy and economic administration. Given this, and the retention of status quo by the MPC in its meeting today, we do not expect any significant change in the course of the financial markets.

“We generally expect the bearish trend in the financial markets to remain within the short term outlook.

“We strongly believe that the decision to hold on to its tight monetary stance in the face of waning economic growth is borne out of the need to keep the Naira “afloat” without necessarily devaluing the Naira.

“However, given the stern realities presented by softening crude oil prices and increasing volatility in the parallel segment of the foreign exchange market– a condition that has intensified speculative activities and round-tripping, we retain our position on the imminence of currency devaluation,” the analysts said.

The uncertain operating environment for the corporate organisations is already showing negative on their results, though the case is not peculiar to Nigeria, but to other nations with their respective brand of economic headwinds.

In Nigeria, since the end of June, half year corporate releases have been dampening investors’ sentiments and enthusiasim. This is evident in the unimpressive earnings posted by few of the companies from the banking to conglomerates sectors.

“These earnings’ results published so far underscore the tough operating environment in the economy, as ASI has lost 10.3 per cent year-to-date. Evidently, several factors suggest that the current equities market lull may persist…,” Afrinvest added.

With the earnings season in full swing, performances of the various markets are expected to be driven majorly by investors’ reactions towards the anticipated earnings results and macroeconomic fundamentals.

Yet, in a turn of fortunes for a vast majority of the global equities markets, they trended southwards, especially in the last one week, when all the developed markets closed in the red- United Kingdom’s FTSE declining the most, -1.9 per cent week-to-date; United States’ S&P 500 and the NASDAQ depreciating 1.3 per cent and 1.0 per cent week-to-date respectively.