Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover With the sustained stability of the naira trading value and zero arbitrage, Nigeria’s foreign exchange (FX) market as it is known today may be transforming, GEOFF IYATSE writes

With the sustained stability of the naira trading value and zero arbitrage, Nigeria’s foreign exchange (FX) market as it is known today may be transforming, GEOFF IYATSE writes

Foreign exchange (FX), globally, thrives on spread. One can only make or lose money because there is a gap between two time periods – when one buys and sells units of a certain currency. The wider the spread, measured by the volatility ratio, the more profits or losses (which are determined by a blend of factors, including expertise and fate) traders make.

[ad]

Naira trading has been a lush business since the post-Structural Adjustment Programme (SAP) because the spread, a cause and effect of manipulation, has been extremely wide. The trend assumed a crisis proportion in recent years as the swings became more regular. After the 2023 market liberalisation, for instance, inter-day deviations from the mean were as high as 20 per cent in some cases.

The high volatility ratio provided an opportunity for smart traders to make quick money. It is also a source of worry for investors and players in the real economy. Dr Muda Yusuf, a private sector advocate, in many instances, raised concern about the potential damage a highly volatile naira posed to the economy.

As the crisis continued, foreign fund managers and holders became increasingly worried about the economy. And they started holding back their capital. For the first time in over 10 years, capital importation was at its lowest at $3.9 billion, which was 40 per cent of the inflow received during the COVID-19 year and a mere 16 per cent of its peak performance, that is, in 2019 when the country pulled was $24 billion.

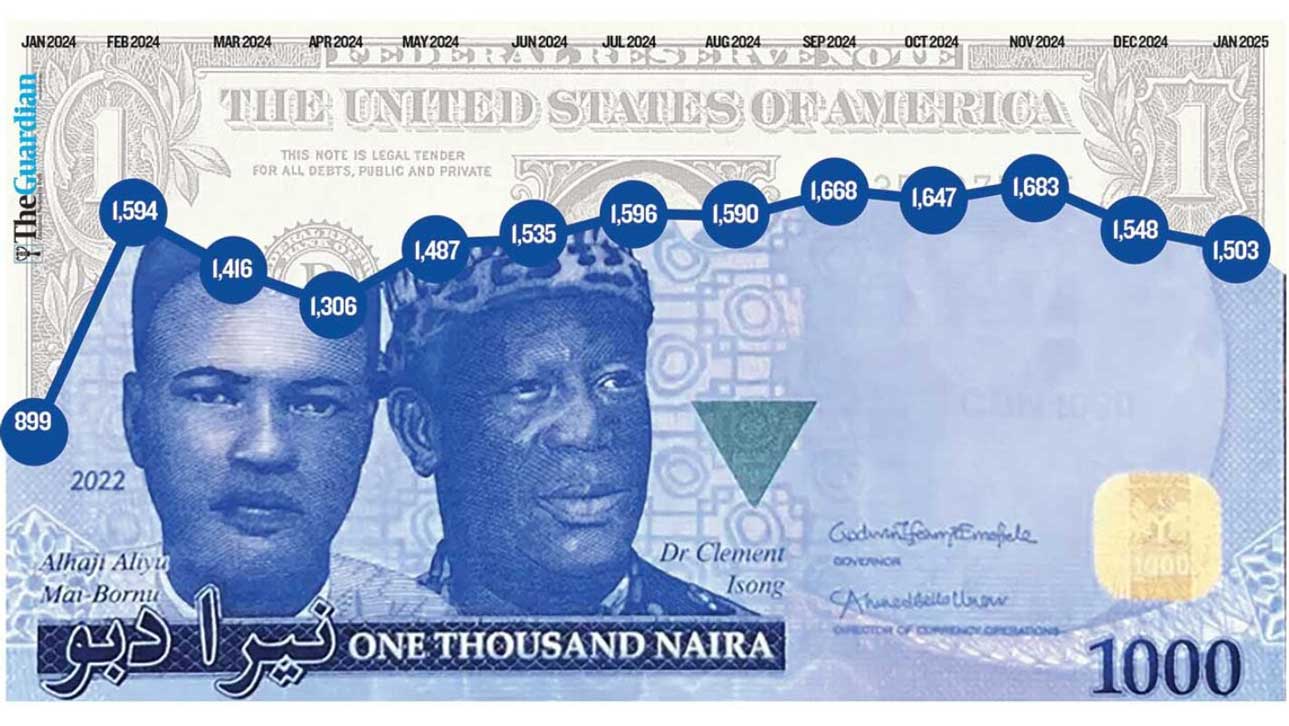

As capital inflow fell so also was naira exchange value stability, which hit its height In January and February 2024. From January 26 to March 15, the naira fell from N900/$ to N1610/$, losing 44 per cent of its value in less than two months only to regain over 60 per cent of its loss value in the subsequent 30 days in what has become the most volatile era of the currency.

[ad]

The currency crisis was turbocharged by the wide arbitrage, which had become a reoccurring feature of the naira since the 1980s. In the run-up, the premium on the black market had risen to 100 per cent, reinforcing the market rigidities, increasing round-trip transactions and heightening the financial loss tension. FX loss, for the first time, became the major cause of corporate losses just. At the sovereign level, Nigeria slipped to the fourth position of African economic leadership.

The pro-market reform did not stop the currency crisis. Shortly after the liberalisation announcement, the domestic currency fell from N460/$ to below N700/$ and the official and black, indeed, converged. But it was momentary as the official market became increasingly inaccessible. At some point in 2024, the divergence was still much higher than five per cent, and many streams of thought put the peg arbitrage above which it becomes a major distortion.

But for the first time in over a decade, Nigeria is seeing a sustained FX convergence, perhaps, a possibility driven by sustained reforms in the market. In the past two weeks, the naira has traded around N1480/$ at the black market, a marginal discount of the moving average of the official market, a reversal of the historical trend.

Naira has also been trading around a narrower range in the past three months, giving it out as a more predictable currency. Perhaps, the currency had not been more stable. In the past month, the currency closed at N1,501/$. With its best outing at N1483/$ and the worst closing rate at N1510.5/$, the highest monthly deviation at 0.6 per cent.

[ad]

The new FX trends point to new realities that could, in a positive feedback loop, feed on themselves to consolidate the gains of the naira. First, there is zero incentive for round-tripping in the market. This means more liquidity in banks, which is perhaps the reason banks have resumed personal and business travelling funding. Also, there are no sufficient catalysts to fuel manipulation, an anti-market practice that thrives on arbitrage. If this continues, FX trading margins could reduce drastically, eliminating the ‘old horses’ and triggering a new trading era.

Also, a less volatile official exchange rate suggests a growth in the economy. As confidence grows, both foreign portfolio and direct investments, in principle, will increase. With a possible fall in artificial demand for FX – a subset of manipulation – Nigeria is likely going to see a divergence in FX demand and supply curves, which will force the market to set a new price equilibrium. In this case, naira will continue in its value, which suggests a lower exchange rate.

The currency’s monetary and prudential environment gives credence to a strengthening naira. Setting the tone for the year, the Monetary Policy Committee (MPC), the rate-fixing arm of the Central Bank of Nigeria (CBN), retained the interest rate at its elevated 27.5 per cent. With its asymmetry corridor at +500/-100 and cash reserve ratio (CRR) of 50 per cent, the high interest rate means restrictive nominal money balances, potentially relieving the naira of pressure.

In the context of FX stability, the MPC members highlighted the benefits of the improvements in the external sector to naira positive outlook and convergence between the Nigeria Foreign Exchange Market (NFEM) and the Bureau de Change (BDC) rates.

[ad]

The committee saw rising banks’ liquidity as a sign of a continual strengthening of the naira and acknowledged the Electronic Foreign Exchange Matching System (B-Match) and the Nigeria Foreign Exchange Code as key transparency support mechanisms. The MPC also attributed the stability to their firmer handshake between the monetary and fiscal authorities, saying both had embarked on new measures to unlock foreign direct and portfolio investments as well as diaspora remittances while improving on the confidence level.

Indeed, the improvement in oil production, which was 1.54 million barrels per day (mbpd) at the end of January 2025, has enhanced the country’s current balance of payments account and the general external sector position. But there is still much to do to scale up the gain of the collaboration. For instance, there are still questions about what proportions of monthly state allocations and what is left for infrastructure development.

The pillaging of public resources and robust infrastructure investment are two extremes with attendant effects on the naira movement. The corruption proceeds, for ease of concealment, are often dollarized, which puts enormous pressure on the naira. Secondly, when the government, whether federal or state government, increases local production, there will be reduced demand for foreign goods.

The monetary authority may not have any say in how elected officials handle their affairs, including the resources they manage. Sadly, the transmission efficiency of its interventions adversely affected the activities of the chief executives, which suggests that an engagement on how to reduce the leakages coming from their actions or inaction should be very active and ongoing as part of monetary and fiscal authority collaboration.

[ad]