Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

• Capital projects get N14.5 trillion in eight yrs

• Recurrent spending items, debt gulp N55.7trillion, 80% of total budget

• National debt increases by average of 20% yearly

• Administration piles up N29.4 as fiscal deficits

• Number of unemployed Nigerians estimated at 39 per cent

• Total budgetary allocation to CAPEX is 22% of FG’s debt

• 20.2m more Nigerians fall into extreme poverty net since 2016

In a matter of hours, President Muhammadu Buhari will mount the rostrum to tell Nigerians how hard he has worked in the past eight years to fulfill the promises of his change mantra. Thereafter, he begins his long-awaited journey from Aso Rock, Nigeria’s seat of power, to his hometown where he hopes to refine after decades of cumulative active public service.

[ad]

But the departure does not suggests that Nigerians have escaped, entirely, the grip of his eight-year leadership, at least, not the consequences of his ‘rare’ approach to national economic management.

Neither is the transition going to be a walk in the park for the President. Perhaps, he would need to pause to defend his role in the mounting national debt that has become a sticking point in the effort to achieve fiscal stability, the bleeding public finances that raise fear about government’s near-term ability to pay its basic bills, the runaway inflation that has turn living into unbearable trauma for millions of households, the inefficient power sector that has sent thousands of entrepreneurs out of business, and most importantly, the sputtering economy.

Otherwise, he would, occasionally, stop to ruminate on the effectiveness of his handling of the frightening insecurity that has made the north, including his ancestral home, a hell for residents and visitors. The road from Abuja, which served as the retired general’s control room in the past eight years, is rife with bandits – a word that has assumed new currency under Buhari. Once, his convoy was attacked by criminals armed to the teeth. If the attack was surprising, the ease at which the assailants escaped arrest and judgment was jaw-dropping.

Exactly eight years ago, Buhari made history as the first candidate to unseat a sitting president in Nigeria’s democratic journey. That came after three previous failed shots at the top job, during which he was seen by his supporters as the messiah the country needed to restore probity in public space and remedy the social injustice an average Nigerian had borne for decades like a second skin.

His eventual victory, which came four years after he wept over a country that had failed to give him the much-desired opportunity to right the wrongs in the society. Hence, his feat was hailed and attributed to his popularity, integrity and many other values on which he rode to power.

This morning, he makes another history – the first Nigeria’s president to hand over a near-50 per cent unemployed citizenry. The first African leader to hand over a nearly 100 per cent debt-to-revenue ratio.

And millions of Nigerians, who supported him to make the historic victory now question their judgment as they look back to the horror of a journey Buhari had pulled them through in what has now been described by many as a lost era.

[ad]

Of course, Buhari has touched a few areas positively. For instance, his flagship programme – the rail system reform inherited from the previous administrations, has recorded some milestones. For instance, the 156km Lagos-Ibadan rail service came to life and started operation under him. The 327km Itakpe-Warri Standard Gauge Rail was completed and commissioned 33 years after construction kicked off while Abuja Light Rail, though now abandoned, was also opened for use.

Across the country, federal roads are transforming from death traps to the real highways they should be. The Presidential Infrastructure Development Fund (PIDF), an initiative of the administration, is said to have invested over $1 billion in three flagship projects – Lagos-Ibadan Expressway, Second Niger Bridge, Abuja-Kaduna-Zaria-Kano Expressway – which are either completed or near completion.

Among other infrastructure initiatives, it signed Executive Order 7, mobilising private investment into the development of key roads and bridges, including Bodo-Bonny in Rivers and Apapa-Oshodi-Oworonshoki-Ojota in Lagos. The latter is a case study of how unconventional thinking could help developing countries unlock infrastructure funding and bridge the wide gaps.

But the gains, in terms of increase in the stock of infrastructure, may have been deflated by the head-shaking macroeconomic readings contained in the handover notes the incoming President, Ahmed Bola Tinubu, will receive today. From debt scare to alarming poverty and the huge unemployment rate to volatile local currency, Buhari has shattered all known documented records in the history of the country.

Poverty-unemployment spiral

The National Bureau of Statistics (NBS) had promised to release updated and improved labour data this month, supposedly, the first labour statistics in over two years. Whereas the promise has not been fulfilled to help economic researchers know the current status of the job market, the Nigerian Economic Summit Group (NESG) and KPMG have pegged this year’s unemployment rate at 41 and 37 per cent respectively.

At the end of 2020, when the last labour data were released by the statistics office, the unemployment rate was 33.3 per cent – over three times what it was when Buhari was campaigning in 2015. If the rate of jobless Nigerians remains unchanged or above the 2020 level, Nigeria will be ahead of South Africa, which currently has the highest proportion of jobless citizens at 32.9 per cent. Nigeria is not ranked for lack of current data.

[ad]

The average projection of NESG and KPMG forecast on the proportion of Nigeria’s working class who are unable to get jobs is 39 per cent, which will be over 600 basis points ahead of the country’s biggest regional rival (South Africa). The number of jobless Nigerians would be as large as the population of Ghana.

At the turn of 2015 when Buhari toured the country with his change agenda, the national rate of unemployment was 7.5 per cent. It tipped to 8.2 per cent the following quarter when the President took the reins of office. In the third quarter, the figure went up to 9.9 per cent, and ballooned to 23.1 per cent in 2018 when the administration’s policies began to take root with dwindling capacity utilisation, factory closure, fleeing investment and insecurity headlines taking over the media space.

Poverty, a constant in the country’s socio-economic equation, is an increasing function of unemployment. The two variables feed on each other and reinforce their growth momentum, especially in an autopilot economy. The rate of poverty and the number of Nigerians living from hand to mouth has increased to a frightening level in the last few years.

For one, there has been a pushback on the poverty label hanging on Nigeria. The description of Nigeria as the poverty capital of the world, for instance, has been described by many as being hasty. On the international scene, questions on the redefinition and reclassification of subjects have gained prominence. But beyond the international profiling and the recent pushback, the government admits that poverty is a major socio-economic challenge confronting the country. For instance, in 2019, the President pledged to commit to measures to lift 100 million people out of extreme poverty by 2030, indirectly confirming that the number of Nigerians in extreme poverty net is not less than 100 million.

[ad]

NBS, last November, released Nigerian Multidimensional Poverty Index (MPI), revealing that 63 per cent of the citizens or 133 million were multidimensionally poor. NBS had also estimated the number of monetarily poor Nigerians at 82.9 million or 40.1 per cent.

According to the 2018/19 Nigerian Living Standard Survey (NLSS) of NBS, official monetary poverty implies Nigerians with real per capita expenditure below the poverty line of N137,430 per year (or N376.5 per day). If the figure is taken as given, the benchmarked N376.5 daily expenditure as a measure of monetary poverty is unrealistically low. The minimum cost of a square meal at mama puts (unbranded local restaurants) anywhere in the country is about N500. That alone mocks the NBS standard definition of poverty.

The threshold is also a far cry from the $1.9 (N874) global daily expenditure cutoff line for people living in extreme poverty. Using the global benchmark, Statista pegs the people currently living in extreme poverty in Nigeria at 90.16 million, which is 20.16 million or 29 per cent higher than what the figure was a year into Buhari’s administration.

The threshold is also a far cry from the $1.9 (N874) global daily expenditure cutoff line for people living in extreme poverty. Using the global benchmark, Statista pegs the people currently living in extreme poverty in Nigeria at 90.16 million, which is 20.16 million or 29 per cent higher than what the figure was a year into Buhari’s administration.

But the concern is more about the lack of commitment to poverty reduction than the absolute number of poor people. The World Bank, after analysing the consequences of poor policy articulation and implementation, in its last year’s Nigeria Development Update, projected that 23 million more Nigerians would be added to the number of people living in extreme poverty by 2030, except the growth rate falls.

The economic cost of runaway inflation

Nigeria has seen the most disturbing inflation figures in the past eight years in terms of momentum and prevalence. For the first time, high inflation became an entrenched issue, making it difficult for economic agents, particularly investors, to plan.

Before Buhari assumed office, the economy had sustained an unbroken 29-month single-digit inflation run, which was a target at some point. Seven months into his administration, the inflation rate left the realm of a single digit but many experts dismissed the then-new trend as transitory.

[ad]

At the administration’s second anniversary, the speed of the headline inflation rate had almost doubled, climbing from 8.7 per cent to 15.6 per cent. Thereafter, efforts to curtail the challenge made little or no difference as the price crisis assumed the character of runaway inflation.

The speed of inflation hit the highway, following the famous border closure of 2019 that left millions of households struggling to feed. The government said the border closure was necessary to check smuggling and rising insecurity while stimulating local production. The government did boast that the country had achieved self-sufficiency in targeted food items like rice. But the market reality was something entirely different, with 50 kilogramme of rice rising by nearly 500 per cent in about four years to hit N40,000 – N10,000 higher than the public sector monthly minimum wage – before the government succumbed to pressure and ordered a partial reopening. Nigerians have been regaled by pyramids after pyramids of rice paddies, which have not stopped the price of the essential food from climbing even high to its current N45,000.

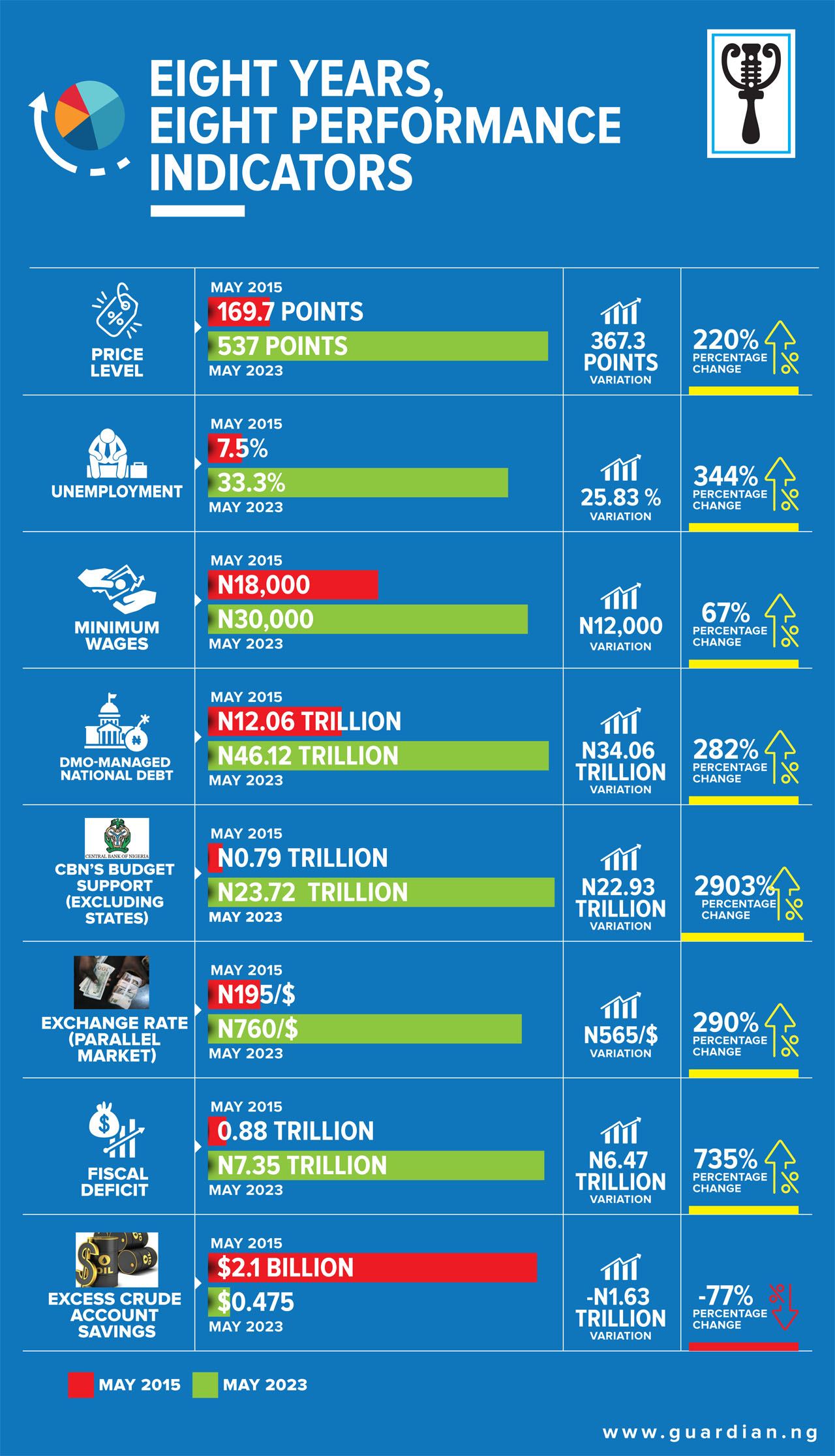

Last month, the headline inflation rate set a new 17-year high of 22.2 per cent while food inflation neared 25 per cent. From May 2015 till April 2023, the composite consumer price index (CPI) has tripled, rising from 169.7 to 537 points. By implication, an average household would need to increase its money income three times to retain its May 2015 consumption bundle.

But sadly, incomes have rather buckled self-employed individuals. Those in paid jobs have also lost their wage negotiating power to rising employment. Since wage is a decreasing function of the unemployment rate, most employees are consigned to reservation wages, an economic term that define a situation where an employee is indifferent as to whether to accept to offer himself for work or not.

[ad]

The growth of the minimum wage reflects how sticky employment conditions have been in the past eight years. During the Buhari administration, the minimum wage grew by 67 per cent whereas the general price level has increased by 220 per cent or over threefold what it was in April 2015, implying that an individual whose money income has tripled is still slightly below his purchasing power as at eight years ago.

Indeed, inflation concern, in recent years, is a global concern. But Nigeria’s elevated inflation predated the trigger of global inflation – COVID-19. Global inflation was caused by the expanded public expenditure that followed COVID-19 and turbocharged by the Russia-Ukraine war. And while inflation is easing elsewhere, such as the United States where it has dropped to a two-year low, Nigeria’s month-on-month inflation change, which measures the current strength of price increase, is still trending upward at about two per cent. The decoupling of Nigeria’s inflation rate with the global trend speaks to the true character of the country’s price crisis. It has little to do with the global shock but more to do with local structural challenges, including inefficient power, poor infrastructure, policy inconsistency and unaffordable cost of funds.

Nigerian businesses have never had it rosy, in terms of cost and access to funds. The rise of fintech, in the past decade, may have eliminated the second half of the twin challenge of funding (access), except that borrowers pay through their noses to secure funds from them. This suggests that unaffordable pricing is more prevalent today than at any other time. In June 2015, the maximum lending rate was 26.4 per cent, which was close to 10 per cent above the rate a decade earlier.

Before the end of Buhari’s first term, the maximum lending rate had spiraled to 31.6 per cent, which was restrictive enough to send many small businesses out of business. The Central Bank of Nigeria (CBN) pegs the current maximum price of commercial funds at 28.6 per cent. With management and sundry charges, high-risk borrowers, including micro, small and medium-scale enterprises (MSMEs), which generate about 84 per cent of Nigerian jobs, according to the International Labour Organisation (ILO), pay as much as 33 per cent as cost of credit.

[ad]

To suck out liquidity from the economy and achieve a stable inflation rate, the monetary authority embarked on an aggressive restrictive monetary policy last May, raising the benchmark interest rate from 11.5 per cent to 18.5 per cent in the 12-month tightening. But the fiscal recklessness and untamed development financing seem to have continued to pour water on the floor, which the Monetary Policy Committee (MPC) inadvertently wasted its time mopping.

Naira as an article of trade

One immutable and most distinguishing function of money is a store of value, where flow John Keynes’ popular quote: “The best way to destroy the capitalist system is to debauch the currency”. Naira has, indeed, faced much debauchery in the past eight years that it became more of an article of speculation and trade than it was a store of value.

The currency had lost its long-standing N150/$ peg against the dollar before the election that ushered Buhari to power. The official rate was about N196/$ with the black market rates converging around the same rate or even trading slightly lower some days. Shortly after the first anniversary of the administration, the official exchange rate of the local currency had lost almost 50 per cent of its value, trading around N280/$.

But the problem was much deeper – the currency became increasingly unstable while the market arbitrage, which was about zero a year earlier, widened to about N80 per dollar. That marked the beginning of the recently-renewed round-tripping and other barefaced official malpractices witnessed in the market. Two years ago, a desperate CBN stopped the weekly funding of the Bureau de Change (BDC) as it grappled with the stern reality of a steadily dipping local currency. What did that achieve? More sliding, increasing volatility.

Since 2016, naira has literally been on the highway with a self-fulfilling prophecy and shorting taking hold of the market. The CBN attempted every strategy in the books only for debauchery to continue. At the height of the crisis last year, a premium on the black market hit 100 per cent – the first time such would happen since the country’s return to civil rule.

[ad]

The parallel market rates have tightened around N750 to a dollar in the past six months with some air of sanity in the market but the damage seems to have been done. At the official market, the currency has lost about 290 per cent of its value against the dollar in the past eight years while it dipped by close to 150 per cent at the official market.

CBN’s budget supports balloon by 2,900% and rising

Less than 20 years after the country exited the debt crisis after it secured a relief from the Paris Club, it is sliding back into the trap, no thanks to the additional N34 trillion accumulated by the federal and state governments in the past eight years. Additional debt, which excludes the controversial and opaque budget supports from the apex bank, has increased the national sovereign by 282 per cent.

But the unrestrained recourse to the ways and means (W&M) window of the CBN and the manner it is managed raises even more worry. The President inherited N789 billion CBN overdraft from his predecessor in 2015; the amount has risen to N23.72 trillion with an unconfirmed report claiming that an additional N4 trillion was accessed in the past three months. Last year, the amount stood at N22.72 trillion while an additional N1 trillion request was approved by the National Assembly before they proceeded to election recess.

Buhari had written to the National Assembly seeking its approval to restructure the debt into a 40-year bond priced at a nine per cent interest rate. The government hitherto paid the equivalent of the monetary policy rate (MPR) plus three per cent as interest on the fund. The National Assembly had earlier requested a detailed explanation of how the proceeds were spent but recently U-turned and approved the request, an action that was followed by bribe allegations.

[ad]

At an emergency meeting yesterday, the Senate also increased the borrowing allowance as contained in the CBN Act, which has been repeatedly violated, from five per cent of the previous year’s revenue to 15 per cent. That will increase the borrowing limit by 200 per cent. The previous clause said that the government could only borrow five per cent of the previous year’s revenue to bridge the budget funding gap and that the loan be deflated within the financial cycle or the CBN seizes to exercise the power.

The International Monetary Fund (IMF), World Bank and other stakeholders have repeatedly called for an end to the abuse of the short-term funding window. But the outgoing administration continued to access the window under the guise that the “economy would have collapsed” if the window was blocked. Besides N4 trillion a media said has been accessed in the last three months, Buhari has borrowed N 22.93 trillion, which translates to an increase of 2,903 per cent.

Depleting savings, growing deficits

The administration would also be remembered for the depletion of the Excess Crude Account (ECA) savings. As at the end of April, the outstanding on the account, according to the Federation Account Allocation Committee (FAAC), was $0.475 million, which is 98 per cent of $2.1 billion ex-President Goodluck Jonathan left behind.

Poor capital project funding, expanded fiscal deficits and bloated recurrent expenditure are some of the bookmarks of the administration. From 2015 till last year, the Federal Government’s actual budgets summed to N69.6 trillion with the fiscal deficits totaling N29.4 trillion, according to figures obtained from the budget performance reports released by the Budget Office.

Of the total budgetary spending outlay in the eight years, only 20 per cent (N13.89 trillion) went to capital expenditure (CAPEX), even though some ministries classify consumables like computers as CAPEX. The balance of N55.7 trillion was spent on overhead and other recurrent items.

FG’s budgetary allocation to CAPEX in eight years is only 22% of the government debt – that is the component of FG’s debt managed by the Debt Management Office (DMO) plus the outstanding N23.72 trillion CBN’s overdrafts. FG owes 84 per cent of Nigeria’s public debt while states jointly sit on 16 per cent. On average, Buhari and the state chief executives added 19.6 per cent to the DMO-managed sovereign debt yearly.

Nigeria could tolerate rising debts but not when it means every naira earned would go into its serving. Last year, FG’s debt servicing to revenue ratio exceeded 80 per cent. It would take bold reforms, the World Bank, projected to prevent it from exceeding 100 per cent in the next few years. That would mean taking fresh loans to pick up other bills and interest on existing debts. This is the state of the economy Buhari will transfer today.

[ad]