Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

• Reserves shed over $2 bILLION in 8-week forex interventions

The nation’s economy still remains on a rocky path, sustaining the sluggish pace of recovery in the face of depressed oil prices, United States (U.S.)-China trade war, uncertainty of Brexit fallouts and fears over decelerating global growth.

Its growth outlook, given the projected external shocks and continued deficit budget challenges that have sustained series of borrowings and accumulated debts at N25.7 trillion, is still doubtful.

The International Monetary Fund (IMF) said the declining global growth and gloomy outlook, will leave traces of effects across economies and called for caution, particularly in deepening fiscal policies.

The Senior Research Analyst at FXTM, Lukman Otunuga, said that although the nation’s GDP expanded 1.94 per cent during the second quarter of 2019, it is unlikely to meet the government’s three per cent growth targets this year, as the IMF has projected the growth to expand only by 2.3 per cent this year and 2.5 per cent in 2020.

[ad]

“Despite the ongoing push for economic diversification, 90 per cent of foreign exchange (forex) earnings and 70 per cent of government revenues are still attained from oil sales.

“While the Central Bank of Nigeria can be commended on its effort to promote Naira stability, this has come at the expense of falling reserves, which decreased to $42.1 billion in September (now at $40.69 billion).

“Much attention will be directed towards the pending foreign exchange reserves data for October scheduled for release on Wednesday (today). Further signs of reserves declining amid weak oil prices and intervention by the CBN is likely to weigh on the Naira,” he said.

Specifically, the apex bank made good its pledge to defend the country’s currency exchange rate, as the falling reserves stockpile showed that about $2.25 billion has been used in several forex interventions from August 30, 2019, to date.

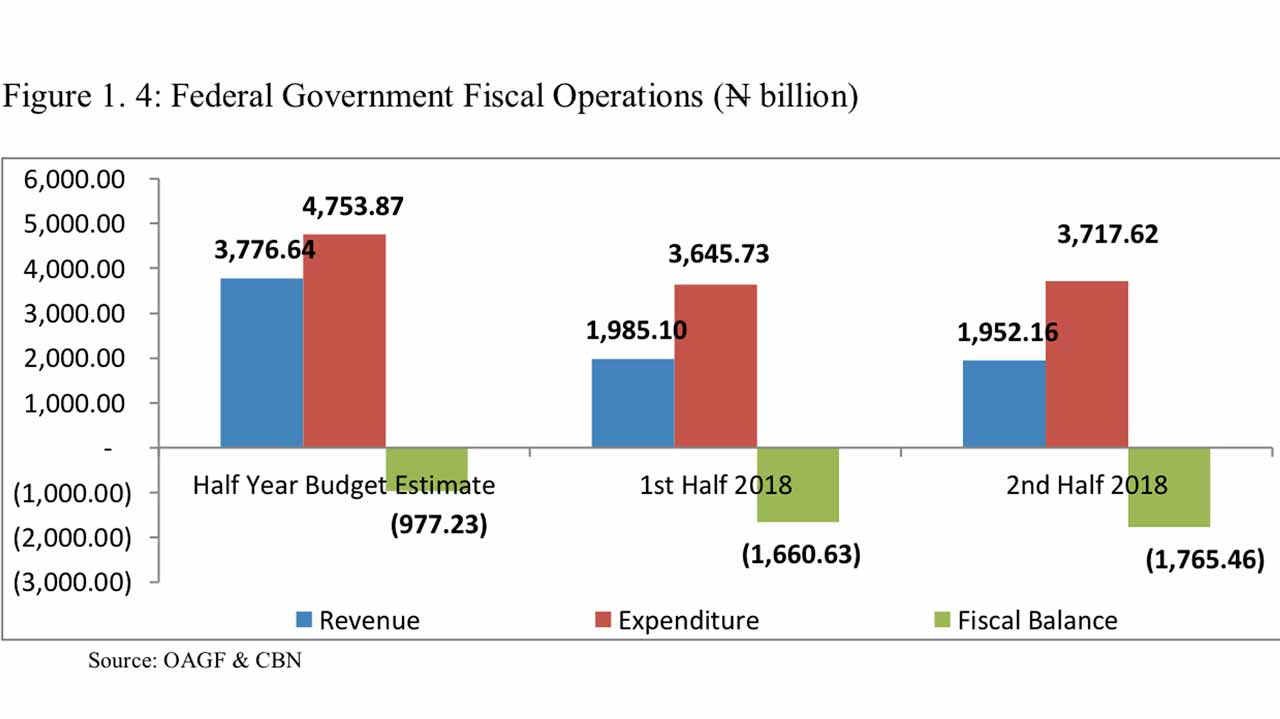

Already, Nigeria will raise its domestic debt profile by N802.82 billion to support the 2019 budget implementation, which would elapse by December 31.

In the 2020 budget proposal, the debt servicing is accounting for 27 per cent of total expenditure and 22 per cent higher than N2.3 trillion approved in 2019 budget. It would be worth knowing that 74 per cent of the N2.7 trillion will be used to service domestic debts. As the country contracts more debts, this provision will continue to rise. Unfortunately, the provision is bigger than capital expenditure that is needed to help in servicing debts.

Conversely, consumptions, also known as Non-Debt Recurrent Expenditure, accounted for 47 per cent of total spending at approximately N4.9 trillion, with personnel and pension costs accounting for N3.6 trillion, representing 74 per cent of non-debt recurrent expenditure, due to the agreed minimum wage.

Generally, there is a significant increase in recurrent expenditure from N6.8 trillion in 2019 to N8.2 trillion in 2020, FSDH Research pointed out, while analysts are already apprehensive that the revenue target will likely not be met, with attendant effects on capital expenditure implementation, worsened by the challenges in the procurement system.

“The revenue projections underperformed actual collection by 47.8 per cent in 2017 and was little changed at 44.7 per cent in 2018 and 41.6 per cent as at first half (H1) of 2019. Although the recent trend in core non-oil revenue has been positive, the projected increase is steep and unlikely to be achieved.

“The projections for non-core, non-oil revenues such as independent revenue, asset sales, recovery and fines, which have historically underperformed, are ambitious. Looking at 2017, 2018 and H1:2019 budget performance, total collection from the non-core, non-oil revenue lines was zero if we exclude independent revenue. We believe these unrealistic assumptions set up the budget for poor implementation,” analysts at Afrinvest Securities Limited said.

Nigeria proposed to earn revenue from the proceeds of oil assets ownership restructuring. But in the two years, not a kobo was earned as no steps were taken to kick-start the process of restructuring. Surprisingly, in the MTEF 2020-2022, this revenue head was omitted.

“Has FGN abandoned the idea? There should be clarity and consistency in policy implementation considering that Nigerian extant Petroleum Policy canvasses this divestment.

“Again, is it reasonable to expect the divestment process to be concluded before the end of 2019 when it is yet to start by October 2019, considering that the process of restructuring and divestment will take a fairly long period of time?” Programme Officer at Centre for Social Justice, Martins Eke, queries.

Nigeria, which emerged from recession in 2017, has borrowed abroad and at home over the past three years to help finance its budgets and fund infrastructure, but debt servicing costs are also rising.

President Muhammadu Buhari, earlier this month, presented a record N10.33 trillion ($33.8 billion) budget for 2020 to the National Assembly, which he expects to be partly financed by foreign and domestic borrowings, as well as proceeds of privatisation.

The proposal represents an 11 per cent increase when compared to the 2019 appropriation of N9.12 trillion, with retained earnings estimated at N8.155 trillion, leaving a deficit of N2.18 trillion, which represents 1.52 per cent of the nation’s Gross Domestic Product (GDP).

[ad]