Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

It will take the Federal Government, at least, seven and half years to pay its existing N36.78 trillion debt – which is about 88 per cent of the N41.6 trillion national public debt stock – if it saves 100 per cent of its retained earnings at the current value.

[ad]

And if the outstanding N19.1 trillion overdrafts and advances it owes the Central Bank of Nigeria (CBN) are included, it will take the government 11 years and five months to pay up supposing the debt and revenue are held constant and it saves every kobo it earns.

But these are extremely simplistic scenarios. For a start, no government can save 100 per cent of its revenue. Secondly, in modern economics, national sovereign debt is a flow, which means it is meant to be measured over a period of time. Yet, in discussing debt sustainability, the carrying capacity of an economy is a key consideration.

The foreign exchange dynamics also pushes the oversimplified supposition too far from reality to deserve a serious thought but that a country can suspend its responsibilities, including salary payment, for over a decade just to clear its debt shows the severity of the country’s indebtedness.

Indeed, the challenge has ballooned beyond the government’s capacity as shown in recent data and that has raised concern about the possibility of default in the near term. Some economists, including the Director-General of the World Trade Organisation (WTO) and ex-Nigeria’s finance minister, Dr. Ngozi Okonjo-Iweala, had warned that the country’s level of borrowing was becoming unsustainable. But as expected, the caution was met with pushback from government officials who were expected to advise the government appropriately.

From N12.06 trillion the current administration inherited seven years ago, the country’s public debt has jumped by 245 per cent to N41.6 trillion as at March 31, 2022. Plus, the CBN’s ways and means (W&M) facilities, which were estimated at N19.1 trillion at the last count, the Federal Government and sub-national entities currently sit on N60.7 trillion debt, albeit minus the undocumented amount. The figure is 83.9 per cent of the country’s real gross domestic product (GDP), estimated at N72.39 trillion last year.

[ad]

Plotted against the global debt-to-GDP ratio, which rose to 263 per cent according to economists at Brookings, Nigeria’s debt to GDP is not much of a problem. But the revenue potential of the drivers of the GDP, such as agriculture, are poor, with the government rather spending to keep the sectors afloat. Also, debts are serviced with revenues rather than GDPs.

Nigeria’s debt to GDP is still at a moderate level, the debt servicing to government revenue has soared to a frightening level, in recent years. It hit 81.1 per cent in 2020 but the government dismissed the enormity of the challenge, hiding under the COVID-19 alibi while it went for more loans.

Last year, the ratio of debt servicing to revenue rose by 1500 basis points to 96 per cent. Yet, the government said there was no option for debt financing, with the Senate President, Ahmed Lawan, saying Nigeria is still too undeveloped to shun the debt market. From the Minister of Finance, Budget and National Planning, Zainab Ahmed, to the Director General of the Budget Office, Dr. Ben Akabueze, and his colleague at the Debt Management Office, Patience Oniha, national economic managers are used to echoing the same refrain – low revenue profile and not the expenditure is the problem – in defence of the borrowing spree. They did little about the falling revenues but give endless reasons to justify more debt requests.

Today, the hole created by the imbalance between falling revenue profile and fast-growing expenditure has expanded into an abyss that is threatening to swallow the country. Media headlines had never been scarier than what the citizens have read in the past five days.

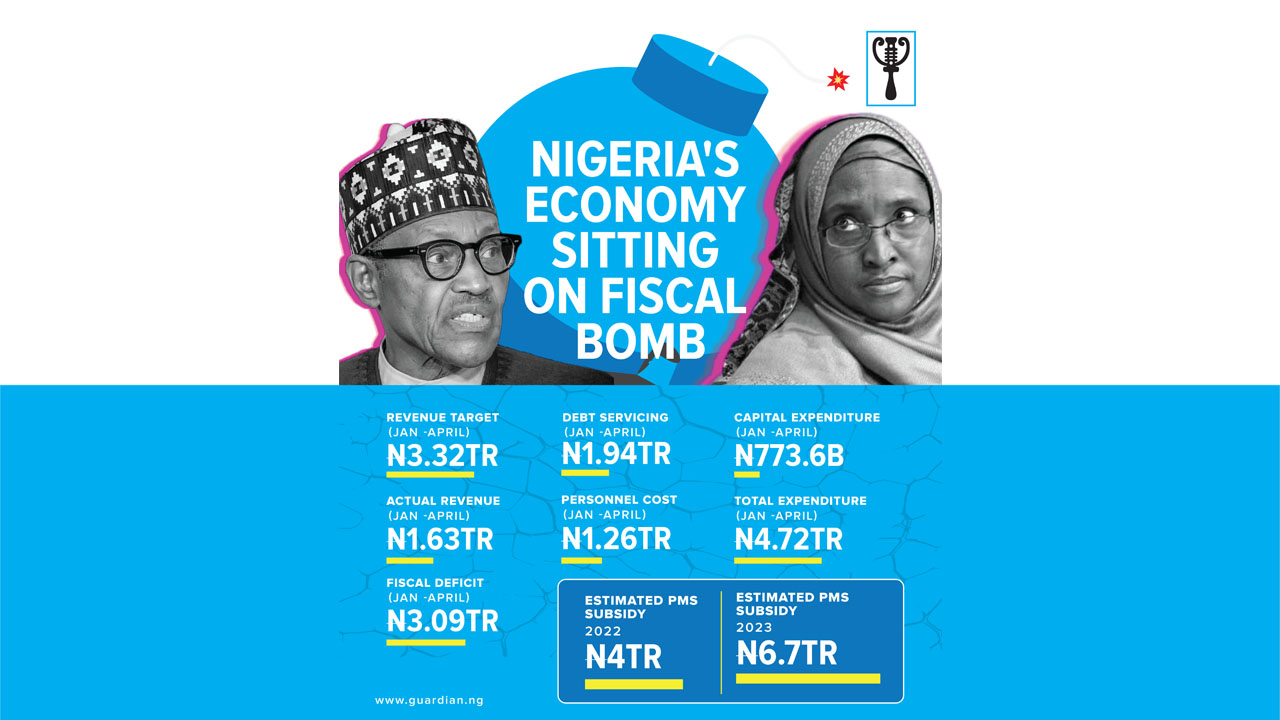

In the first four months of the year, the FG spent N1.93 trillion on debt servicing amid plummeting revenue mobilisation, which put the retained earnings at N1.63 trillion in the same period. That pushed the debt to revenue ratio to 118 per cent, the first time the figure would hit or exceed 100 per cent. By implication, the government would need to borrow to meet its obligation supposing its financial need was fulfilling its obligation to existing creditors.

Of course, there were other pressing obligations. Personnel cost gulped N1.26 trillion, leaving only N773.6 billion for all-important capital expenditure (CAPEX) out of the total spending outlay of N4.72 trillion, implying that only 16 per cent of the spending went into infrastructure stock, a key driver of growth. Debt servicing and personnel took as much as 84 per cent of the total expenditure and amounted to almost 200 per cent of the earned revenue.

[ad]

The fiscal performance update presented alongside the 2023-2025 Medium Term Expenditure Framework and Fiscal Strategic Paper (MTEF and FSP) estimated the revenue performance at 49 per cent as the prorated target for the period was N3.32 trillion.

And that is not surprising. In the first quarter, oil output dropped to its lowest level in recent history, averaging 1.3 million barrels per day (bpd). According to the budget performance overview presented by Ahmed, production went up to 1.4 million bpd at the start of this quarter but slumped to 1.25 million bpd in May. June data are not available, but with no efforts made to reduce oil theft, the figures may be annualised.

The government hoped to gross N9.37 trillion from oil and gas revenue in the year as projected during the appropriation. But despite the spike in international oil prices, which exceeded the budget benchmark by a wide margin, only N1.23 trillion was realised as at the end of April 30. The figure translates to 39 per cent in actual performance, and the finance minister attributed the shut-ins to pipeline vandalism and crude oil theft. She promised that the situation would improve in the second half of the year following “concerted efforts” to address the challenges but there are no specifics of the efforts.

Added to the dreary fiscal position is the controversial premium motor spirit (PMS) subsidy. The annualised retained revenue of the Federal Government is only about 20 per cent higher than N4 trillion earmarked for this year’s subsidy.

In all of these, the government is bogged down with important unfulfilled commitments it makes vain efforts to trivialise. For instance, its running battle with the Academic Staff Union of Universities (ASUU) and its unwillingness or inability to pay its indebtedness to the body has shut the ivory towers since February. There are other unkept promises – to the Nigeria Union of Teachers and other trade unions, which Prof. Godwin Owoh (an economist) said it should be added to the sovereign debt stock.

Historical data on the country’s fiscal position could be dismissed as backward-looking. But even the future does not appear to inspire hope, at least not as the government has envisaged it. In its best scenario analysis, it hopes to spend N3.36 trillion on PMS subsidies next year. That assumes that provision would be made for only six months into the year, reflecting the earlier announcement extending the social scheme by 18 months.

[ad]

Under business as a usual assumption, which is most likely as subsidy removal has become a moving target, PMS subsidy will gulp N6.7 trillion. If this assumption holds, the government could incur as much as 137 per cent of its retained revenue, estimated at this year’s performance so far, on subsidy payment. The opportunity cost of spending that much on subsidy is health, education or infrastructure investment that will be sacrificed.

Should subsidy payment continue beyond the middle of next year, the finance minister confirmed that it “is not feasible to make any provision for MDAs’ capital expenditure” beyond the multilateral/bilateral loan-funded and donor-funded projects in the appropriation projected at N16.98 trillion, with a fiscal deficit estimate of N10.5 trillion. Assuming subsidy removal reform is achieved, the fiscal space could expand, allowing FG to earn N8.46 trillion and raise the spending limit to N17.99 trillion. That will put the fiscal deficit at N9.53 trillion or about 13 per cent of the country’s real GDP, which is above the three per cent threshold stipulated by the Fiscal Responsibility Act (FRA).

Meanwhile, some of the revenue targets and parameters are more of a statement or hope as they do not reflect recent data. For instance, the crude production output is estimated at 1.69 million bpd for 2023 and 1.83 million bpd for 2024 and 2025. In contrast with recent output data, some of which were presented in the same document, the estimates may be spurious – the sorts that have raised fiscal deficit above projected level in the past years. The last time Nigeria achieved the 1.69 million bpd mark was 2020 when the production was 1.7 million bpd. Since then, output has hovered between 1.12 million and 1.48 million bpd. This suggests that the fiscal hole could be wider than contemplated by the medium-term plan, meaning the government would need to borrow much more than it is currently doing.

Where would the debt come from? Beyond debt sustainability issues, the era of free market risk is gone with monetary easing. Commercial lenders are not expanding their balance sheets anymore just as premium on risky assets is rising very fast – a reason Nigeria’s 10-year Eurobond yield has risen from 8.6 per cent at the end of the first quarter to over 14 per cent.

[ad]

A recent report by The Guardian said the country has been priced out of the international market, making it difficult for the country to access the market for refinancing or fresh facilities. The report was published in June. If anything has changed since then, jerkeddeteriorated with the country’s sovereign bond yield rising further to about 15 per cent.

The government is left with the domestic debt market option but the odds are increasing with the aggressive rate hike move of the Monetary Policy Committee (MPC). Last week, the interest rate was jacked up from 13 to 14 per cent with a promise that the policy option will be sustained should inflation remain uptrend. Besides, the governmnt, if it chooses to look inward for fresh loans, also risks crowding out private sector operators, who are battling a harsh operating environment across the board.

The three pillars of supply-side economics, where analysts tie the country’s production challenges, are tax, regulatory and monetary policy. Government has hinted that there is sufficient headroom in the first stream as Nigeria’s tax to GDP is among the lowest in the world. Unfortunately, it is currently not in a mood when it cannot tell, which of its desperate actions could make things go irreversibly wrong.

[ad]