Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

The multi-prong approach to achieving the set target of including 80 per cent of the country’s adult population in the financial system come 2020, is gaining traction, as the initiatives, led by the Central Bank of Nigeria (CBN) recorded improved numbers and affirmation, shortly before the end of last year.

The multi-prong approach to achieving the set target of including 80 per cent of the country’s adult population in the financial system come 2020, is gaining traction, as the initiatives, led by the Central Bank of Nigeria (CBN) recorded improved numbers and affirmation, shortly before the end of last year.

The confidence-building information, contained in the result of the 2018 survey figures by Enhancing Financial Innovation and Access (EFInA), showed that 63.6 per cent of Nigeria’s adult population now has access to financial services, with 2.6 million more being capture in the system, leaving only 36.6 per cent now financially excluded.

Earlier last year, the Shared Agent Network Expansion Framework, which received CBN and the Bankers Committee’s commitments, was fired off, with the goal of reaching the financial inclusion target by 2020.

[ad]

With arrangements under SANEF, no less than 500,000 agent networks will be created across the country, in a move that will invariably, create jobs for the agents, but more importantly, become effective approach to reaching millions of the unbanked in the rural areas.

A member of the Technical Committee of the Bankers Committee on SANEF initiative, Bolaji Lawal, explained that the agents would be deployed at all the 774 local councils, experience centres of telecommunications companies and markets.

But as at then, there more than 70,000 access points in the country, three mobile money operators, six super agents and a target of between 100,000 and 150,000 agents network in the third and fourth quarter of 2018 respectively.

Since the launch of the National Financial Inclusion Strategy in 2012, stakeholders had innovated various interventions in its implementation process.

The Financial Inclusion Steering and Technical Committees were established across the states in January 2015, along with the Channels, Products, Financial Literacy and Special Intervention Working Groups.

The tiered Know-Your-Customer (KYC) framework was also introduced by the Central Bank of Nigeria (CBN) in 2013 to simplify the requirements for opening and operating bank and mobile money accounts for the low income people.

Again, the Agent Banking Guidelines were released to bring the services near the people by allowing third parties such as pharmacies, fuel stations, supermarkets, cooperative societies, among others, to offer banking and mobile money services on behalf of banks and mobile money operators.

Similarly, the National Identity Management Commission (NIMC) had vigorously pursued a comprehensive identity management system for Nigeria, while the National Pension Commission (PENCOM) pursued a micro pension framework for small businesses, informal sectors and those whose income do not come in regular streams. All, inherently linked with financial inclusion.

[ad]

Still, in collaboration with its stakeholders, the Securities and Exchange Commission (SEC) kick-started the process of increasing distribution channels to enhance access to capital market products by promoting collective investment schemes, Capital Market Financial Literacy and Capital Market Financial Inclusion Strategy.

The National Insurance Commission (NAICOM) had been implementing non-interest based products to reach out to more people, even as it released the micro insurance guidelines to provide explicit licensing of micro insurance companies and penetration of micro insurance to micro clients.

The Bancassurance Framework was another effort towards boosting inclusion, jointly released by CBN and NAICOM, to be used as a platform for extending insurance coverage to existing customers of banks.

In the same vein, the CBN recently released the guidelines for the regulation of Payment Service Banks (PSB) in Nigeria. When this comes in effect early next year, it will provide a level playing field for the provision of payment services to the bottom of the pyramid.

While these interventions contributed in large part, to some of the positive results in the EFInA report, the revised National Financial Inclusion Strategy was released in November 2018.

Nevertheless, stakeholders have been mapping out interventions to address access to finance by women, youth, rural dwellers, MSMEs as well as those vulnerable and excluded groups in the Northern parts of the country, in a move to create level playing field for service delivery.

EFInA, a non-governmental organisation and a financial sector development organization funded by the Department for International Development (DFID) and Bill & Melinda Gates Foundation towards promoting financial inclusion in Nigeria.

[ad]

The firm conducts surveys every two years in order to determine the situation of things regarding financial inclusion in the courtly.

The 2018 report came after a painstaking research carried out across the country, with 750 respondents in each of the 36 states and the Federal Capital Territory (FCT), and 27,470 interviews, which represents 97 per cent of the target samples of 28,380.

The survey was anchored on several indicators, including Banked Population; Remittances; Savings with a Bank; Payments; Received Income; Loan with a Bank; and Banking Agents, among others.

Remarkably, an increase of 1.4 per cent in the Banked Population from the 2016 to 2018 was found, a decrease of 2.2 per cent in Remittances and another decrease of 6.7 per cent in Saving with a Bank within the period.

The indicators of Payments, Received Income and Banking Agents all recorded increases of 3.4 per cent, 1.3 per cent and 0.6 per cent respectively, while Loan with a Bank remained static at 1.3 per cent.

The report however found a decrease of 1.6 per cent (from 30.1 per cent in 2016 to 28.5 per cent to 2018) in the non-bank indicators of Pension; Savings through other Formal Institutions; Mobile Money; Mobile Money Agents; Insurance; Remittances; and Loans with other Formal Institutions.

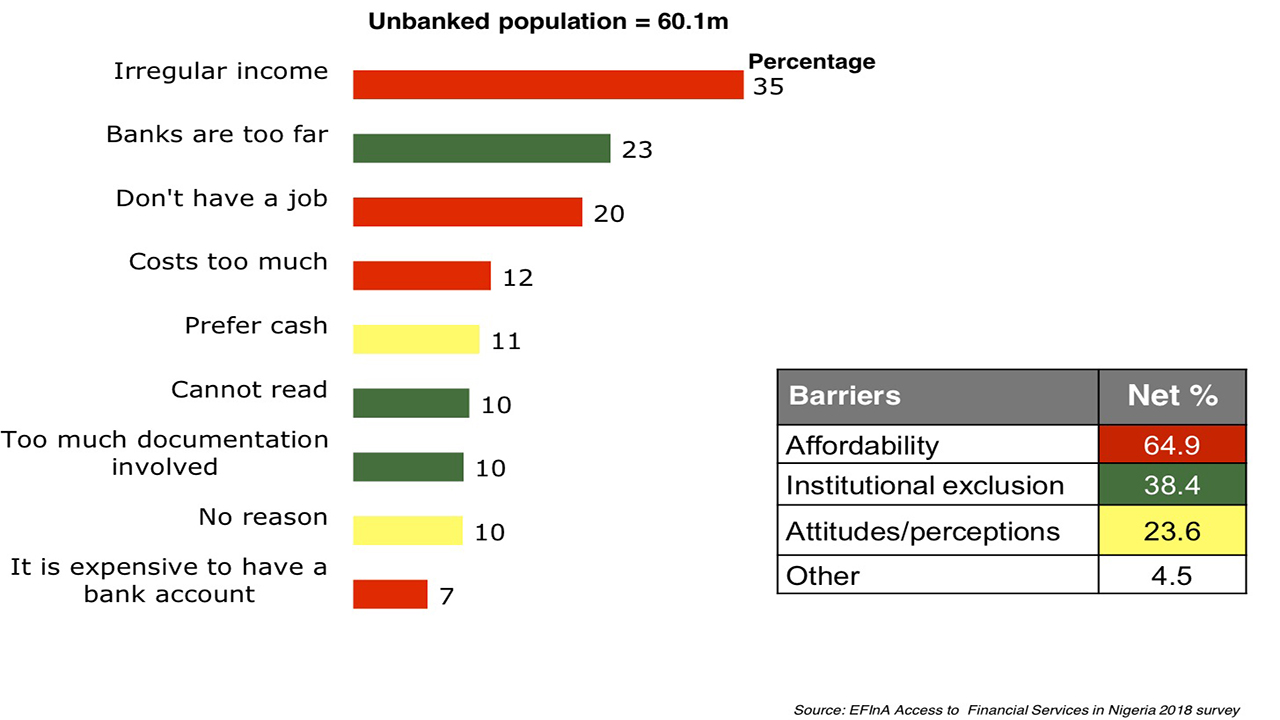

The EFInA survey report concluded that three factors of affordability, institutional exclusion and lack of awareness were the biggest obstacles to financial inclusion. According to EFInA, 60.1 million Nigerians do not have/use a bank account, 96.3 million do not have/use mobile money and 97.9 million do not have insurance.

[ad]

Chairman of EFINA Nigeria, Segun Akerele, during the presentation of the survey, said there is a clear indication of the resilience of ordinary Nigerians, despite being in a challenged economy, adding that the message of financial inclusion is really deepening on gradual basis.

For the Chief Executive Officer, Esaie Diei, EFInA’s work will retain its topnotch status, adding that the advocacy on financial inclusion in Nigeria and the development of the financial sector would always be pursued.

Former Deputy Governor and Acting Governor of the Central Bank of Nigeria, Dr. Sarah Alade, in her keynote address, pointed out that the survey will help stakeholders to come up with pragmatic solutions that will address the issues in financial inclusion.

According to her, the survey has clearly identified some institutional and capacity constraints that holding back the speed of the project and these would be given additional attention.

The report revealed that mobile money, which was thought to be useful in the financial inclusion drive, could only deepen rather than expand in adoption, as 35.5 million Nigerians use bank accounts, while only three million adults have both mobile money and bank accounts, with 59.4 million not having mobile money nor bank account.

[ad]

Similarly, 82 per cent of Nigerian adults, comprising subsistence farmers and small business owners, receive their income in cash, while another eight per cent did not receive any income at all.

Savings in the country dropped by 13.3 per cent according to the report, while savings in assets, property, and livestock rose from 47.4 million to 54.7 million since 2016.

Other decrease in respect of this indicator was that of borrowing, which went down by two per cent and remittances to one per cent.

On financial access by gender, out of 99.6 million adults in the country, 33.5 million male adult Nigerians were financially included compared with 29.4 million female adults.

This represents a decrease in the exclusion rate of 4.3 per cent and 5.7 per cent in the male and female gender respectively, and a decrease of 4.8 per cent for both gender compared with the 2016 figures.

The exclusion rate between the urban and rural areas showed that only 21.6 per cent Nigerians in the urban areas were excluded compared with 45.6 per cent Nigerians in the rural areas.

[ad unit=2]

The gains recorded on this indicator revealed a decrease of 2.8 per cent and 6.6 per cent exclusion rate in the urban and rural areas respectively, as well as 4.8 per cent exclusion rate recorded in total since the year 2016.

Regionally, the South West and South-East, two zones with the least financial exclusion rate in the past, had underperformed in the last two years.

The zones recorded exclusion rate of 18 per cent and 28 per cent respectively in 2016, compared with 19 per cent and 29 per cent exclusion rate, respectively in 2018.

All the other zones however recorded significant decrease in exclusion rate in the last two years with the South-South zone improving from 31 per cent in 2016 to 23 per cent in 2018, and the North-Central achieving 31 per cent in 2018 from 39 per cent in 2016. North-East and North-West scored 55 per cent in 2018 from 62 per cent in 2016 and 62 per cent in 2018 from 70 per cent in 216, respectively.