A downward trending inflation and positive growth of nominal money stock have only complicated the dilemma of the rate-fixing arm of the Central Bank of Nigeria (CBN), Monetary Policy Committee (MPC), in determining if the decade-old fragile and aneamic output growth or a possible spike in general price level is riskier for the domestic economy, with the outcome of the 301st meeting hanging on how the members internalise and interpret the many conflicting economic indicators (exposing the underbelly of economics as a dismal science), GEOFF IYATSE writes.

If the Monetary Policy Committee (MPC) lowers the benchmark interest rate at its crucial 301st meeting, which ends tomorrow afternoon, it would not, in any way, mean that a lower interest rate is a superior policy option. It may only suggest that a lower interest rate is timelier in its assessment.

It could also imply that the majority of its members, the grundnorm of its resolutions, consider a cheaper cost of borrowing more relevant than more stable prices. Perhaps it could also be seen as a self-proclaimed satisfaction with the technical committee’s interventions over the past 18 months under the current leadership.

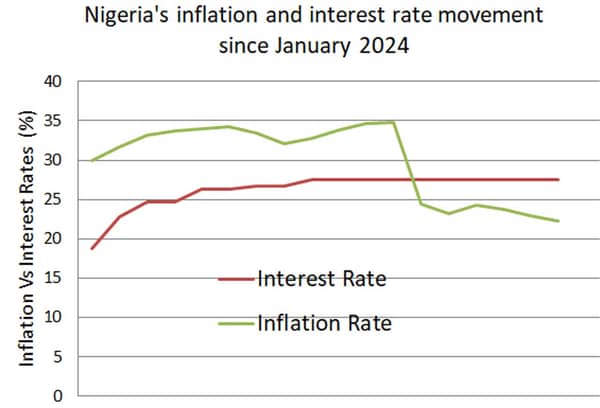

But most importantly, a rate cut or hold may also depend on where the members set their views. A backward-looking view could suggest the inflation battle is over in the medium term. About eight months ago (in December), the headline inflation stood at 34.8 per cent – about 1300 basis points (bps) above the most recent consumer price index (CPI) reading. Of course, there is an argument that the CPI rebasing was all that was required to magically bring down the stubbornly high inflation rate to the current band. Could things have been different from the consistent uptick in 2023/2024 without the CPI rebasing? Perhaps not as sharp as the drop seen in the past six months.

Granted, however, the speed of price hike has been slowed by consumer resistance and the foreign exchange (FX) (a major inflation rate driver) market stability recorded in the past year. Month-on-month (M/M) change, which reveals the current tenacity of inflation, remains positive but is slowing. Independent market surveys indicate that prices of some essentials, ranging from building materials to consumables, have remained unchanged since January. For the food segment, a few staple items have witnessed a moderate drop in prices. For instance, there has been a noticeable drop in the prices of rice, beans and garri (with some reports claiming there is a glut). A model of this perspective could point to a deflationary trend and support a moderate rate cut, which some experts are already betting on.

But backward-looking data does not stop at a six-month or one-year analysis. About a decade ago, the inflation rate was a single digit and remained consistently so. If the MPC members have a long-term horizon, they could also consider pre-2015 when the inflation rate was a single digit. That would leave a wide hole in the current inflation victory.

Understandingly, a single inflation rate is an unrealistic target in the short- to medium-term. But if that is even a long-term, an elevated interest rate regime, assuming the transmission mechanisms are effective and strong enough, should remain a policy choice as advised by the International Monetary Fund (IMF) in its recent Article IV report.

And the committee could also choose a forward-looking approach for its modelling. That would require its members to consider the near-, medium and long-term outlook and consider the ability of the economy to stave off re-inflationary risks, taking into consideration all endogenous and exogenous variables.

This would also require a thorough analysis of the inflation expectation and scenario mapping of the causes and effects of its volatility. The pull-and-push relationship among the variables that trigger relevant inflation would also be considered with the view of establishing the risk of falling back into the 2023 and 2024 runaway inflation.

Perhaps, a forward-looking view may also launch the monetary authority into a deeper and endless spiral of questions on the structural dimension of Nigeria’s inflation, ranging from the low complexity index of the economy to the uncompetitive manufacturing index, poor local capacity utilisation, the paradox of power inefficiency, inadequate support for local industries and the taxation disincentive. These are areas where it can only advise rather than intervene. Many analysts have described structural challenges as the strongest driver of Nigeria’s inflation – sadly, they get little or no attention in the battle for a less destructive inflation growth. Perhaps, the distortion of the structural defect is getting worse with what appears to be a coordination failure in the current fiscal setup.

In the next two days, as it has been historically, the MPC will subject the entire gamut of inflation, both that it can measure and those outside its control, to monetary base analysis. It is more like using a model where the residual accounts for over 70 per cent of the independent variables for important decisions. Sadly, this has become the norm. Little wonder that there is a strong positive correlation between interest rate and money supply, which has increased by 145 per cent since May 2022 when the CBN started the post-COVID-19 tightening. Broad money supply was N48.5 trillion in May 2022 when the interest rate was 11.5 per cent. As of last May, when the interest had more than doubled to 27.5 per cent, the money supply rose to N119 trillion.

But money balance growth is only one of the conflicting variables in the face of tight monetary policy. In April 2022, the most recent CPI reading before the then Godwin Emefiele-led CBN raised the monetary policy rate (MPR), headline inflation was 16.8 per cent. Over the years, the inflation rate had assumed a rising function of interest rate, exceeding almost touching 35 per cent before the recent easing – an antithesis of the Phillips Curve, a theoretical framework that explains the trade-off between inflation and interest rates.

The counter-intuition of the upward trend of both interest and inflation rates is one of Nigeria’s many economic anomalies. In the United States, the headline inflation was heading to 10 per cent when the last interest rate hike campaign kicked off. A few months into the rate hike run, the inflation rate was brought down to a manageable level. In the United Kingdom and many other advanced countries, high interest rates have acted as antidotes to rising liquidity and high consumption demand that are responsible for the price crisis. Since 2021, the a priori expectation has been retested, with the well-behaved market validating the ancient theories.

But in the case of Nigeria, weak transmission mechanisms and market failure have rendered MPR less effective in anchoring inflation and taming the price crisis. Perhaps, the gains of the interest rate hike are the increase in capital inflow, which has translated to high FX liquidity and a more stable naira. Through the FX pass-through effect, a weaker naira has served as a major price driver. For instance, from 2023 to the height of the FX crisis last year, the naira had lost nearly ¾ of its value. Most imported goods, such as cars and medical consumables, equally witnessed a similar reverse spike in prices.

If an interest rate hike was responsible for capital inflow, a major objective of the aggressive interest ‘pumping’ of Yemi Cardoso, the CBN governor, it also suggests that a lower interest rate could trigger capital outflow, which is another caution for the MPC.

Of course, liquidity has improved in recent months, supporting the naira’s moderate four per cent year-to-date (YTD) gain. But the naira is still not considered stable enough to suggest that a rate cut is not premature. Already, falling yields on debt instruments are sending an untoward signal. The MPC may not want to heighten the apprehension with a sudden and sharp rate cut – perhaps not this year.

Interestingly, the continued global trade tension is fueling fresh inflation while sending warning signs to central banks. Federal Reserve Chair, Jerome Powells, disclosed that President Donald Trump’s tariff plan is a valid reason for delaying quantitative easing. Within the context of the fresh concerns, Nigeria and other developing countries may adopt a wait-and-see posture in the coming months, which is necessary for preventing capital flight.

A liquidity pressure could come with an enormous burden. In the first half of the year, the CBN spent $4.1 billion defending the naira, over 200 per cent of the amount spent in last year’s comparative period, according to CSL Stockbrokers report. That level of spending may not be sustainable given the poor FX inflow and the health of the country’s reserves, a reason the monetary authority would want to maintain a competitive interest rate to keep the dollar inflowing. Industry stakeholders have baulked at the sustainability of the naira defence bill, citing weak oil earnings, subdued foreign portfolio investment inflows and uncertainties around external financing.

“Our objectives have been and will continue to be to achieve stability in the FX and financial markets. CBN will continue to embrace orthodoxy and stay the course. We remain vigilant and will not take anything for granted. Inflation has been too high for too long, and our goal is to bring it down from double digits to single digits in the medium to long-term,” Cardoso said, suggesting the long-run goal of the tightening is yet to be achieved.

This was the position of the CBN boss two months ago. Two months, indeed, could be a long time in uncertain economic times. But nothing much has changed in the price assessment framework – inflation remains above 20 per cent; naira still trades above N1500/$ while output growth projection remains above three per cent. Cardoso controls only a vote. But if he remains consistent with his position in May, he wants to see the benchmark interest rate kept at 27.5 per cent in the meantime.