Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

Last year, non-prime borrowers, including small and medium enterprises (SMEs), paid an average of 145 per cent as cost of funds higher than the multinationals, big corporations and others considered as prime borrowers, an analysis of money market indicators have shown.

Prime borrowers are individuals and organisations whose perceived credit risks are below average. The categories of borrowers are likely to make full payments on time. Facilities to such individuals are often priced lower than the market rate.

[ad]

While the prime-lending rate is lower than the maximum loan price globally, the difference between prime and non-prime credits is often far wider than the global average.

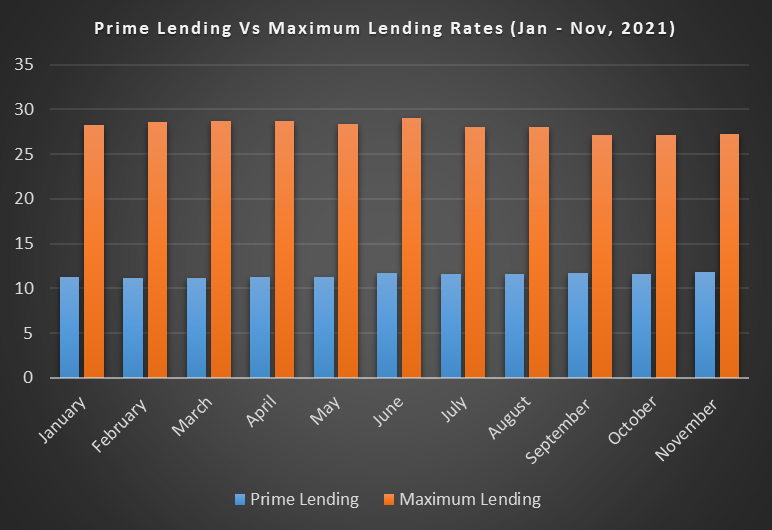

According to the document sourced from the Central Bank of Nigeria (CBN) yesterday, prime borrowers paid an average of 11.47 per cent as interest rate from January to November last year. The rate is 16.64 percentage points less than the average maximum interest rate of 28.1 per cent paid by other borrowers.

June was the toughest month for most borrowers. Then, the maximum interest rate, the statistics said, was 29.05 per cent as against prime borrowing cost of 11.67 per cent.

[ad]

Whereas, struggling small businesses paid through their nose to access funds in the year, the rates banks offered to their prime customers were less than the monetary policy rate (MPR), the floor of all commercial rates set by the Monetary Policy Committee (MPC).

The country’s MPR remained at 11.5 per cent throughout last year while the average prime-lending rate was 11.47 per cent.

The MPR was reduced by 100 basis points from 12.5 per cent in September 2020 as part of the MPC’s concessions for businesses, which were hard hit by COVID-19.

[ad]

Overall, the prime lending rate was less than MPR, which means it was less than the stimulated minimum interest rate. It opened the year at 11.25 per cent, 0.25 percentage points less than MPR, and stayed around the rate until June when it rose to 11.67 per cent.

At its current rate, also, the real prime lending rate – nominal rate less inflation – is negative. The country’s headline inflation rose to 18.17 per cent in March before the National Bureau of Statistics (NBS) claimed it started moderation.

According to the November Consumer Price Index (CPI), the most recent available data, the country’s inflation rate is currently 15.4 per cent, which was still higher than the year’s average prime rate.

[ad]

Juxtaposing the average prime rate for the year (11.46 per cent) with the current inflation rate, the real prime lending rate last year was -3.9 per cent, suggesting that the banks might have paid big-ticket customers to hold their funds for them.

Access to cheap funds is considered as one of the most critical challenges facing small businesses in Nigeria, which are estimated at over 41 million.

[ad]

An economist and former Director-General of the Lagos Chamber of Commerce and Industry, Dr. Muda Yusuf, had described the wide differential between prime and non-prime lending rates as a signal of the funding crisis faced by small businesses. Yusuf said urgent policy actions must be taken to make credit affordable to businesses for productive purposes.

Speaking with The Guardian, a professor of applied economics, Godwin Owoh, said the breakdown of monitoring of key monetary system pricing – interest, exchange and inflation rate – is a major concern as the economy struggles into another year.

[ad]