Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

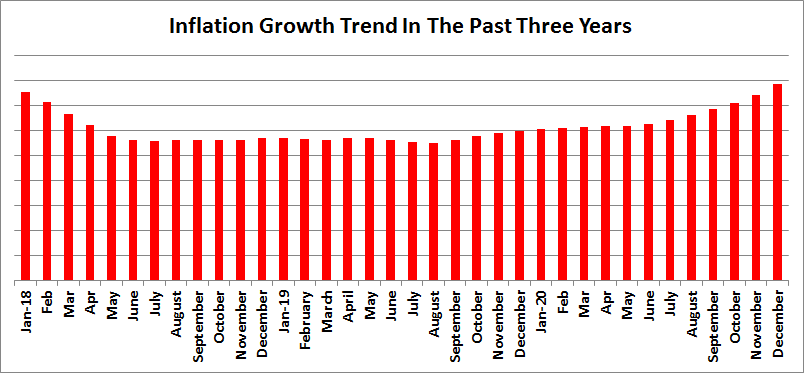

The headline inflation has grown consistently in the past 15 months to hit 15.75 per cent in December. The last time the index reached and exceeded its current figure was December 2018.

Unmanageable inflation growth is a challenge but just one among the red data the economy is grappling with. Unemployment (plus underemployment) also reached an all-time high of above 55.7 per cent last year just as the weak naira is crushing the purchasing power of an average citizen daily.

[ad]

At the same time, production continues to face a cost efficiency challenge with the government’s ability to intervene being weakened by falling revenue. The country officially announced a recession last year when the gross domestic product (GDP) plunged over six per cent.

These indicators point to one worrisome socio-economic trend – a growing misery index, which a professor of economics, Akpan Ekpo, said “was above 90 per cent the last time” he calculated it.

The misery rate index determines how the average citizen is doing. It has a strong correlation with social upheavals and crime rate, which has already held the northern part of the country hostage manifesting in banditry, kidnapping and terrorism.

[ad]

The index also, in theory, measures the social costs of unemployment, inflation and growth rates, which are all currently at a crisis level.

Ekpo, a former director-general of West African Institute for Financial and Economic Management, said the rising misery index would push more Nigerians below the poverty line and escalate social tensions, except urgent measures are taken to check it. He was, however, quick to identify the only macroeconomic tool that can work in the Nigeria current situation – fiscal policy.

Existing data suggest that Nigeria’s poverty level is already in dire straits. For instance, the latest round of the Nigerian Living Standards Survey of the National Bureau of Statistics (NBS) said 40 per cent of the total population of about 83 million people lived below the poverty line estimated at $381.75 per year as of 2019.

[ad]

The 2020 data are not available but with the devastating impacts of the coronavirus 2019 (COVID-19) pandemic, which has thrown more people into the labour market and killed sources of livelihoods of thousands of households, the level of poverty is expected to have increased.

For millions of Nigerians who were already walking on a tightrope before the outbreak, COVID-19 was like a falling knife. The fall of oil prices has worsened the currency crisis with the naira losing about a quarter of its value to the dollar in the past 12 months as the Central Bank of Nigeria (CBN) is struggling to protect the local currency.

The contracting production, Ekpo said, has made the crisis extremely precarious. “The unemployment is rising; real interest rates are negative while the cost of borrowing is high for small businesses. This means we are heading towards a crisis,” he said.

[ad]

While the big organisations may have been taking advantage of the all-time low bond yields to raise fund through debt instruments, the small and medium enterprises (SMEs), which, according to the International Finance Corporation (IFC), accounts for over 96 per cent of Nigeria’s businesses and generate about 84 per cent of the jobs, are still cash-starved. Some borrow at above 20 per cent where available.

The director-general of the Lagos Chamber of Commerce and Industry (LCCI), Muda Yusuf, said the unbearable cost of funds is a major challenge affecting the performance of the private sector, including the SMEs. At a forum on the 2021 outlook recently, he also noted that the illiquidity of foreign exchange was a major problem affecting the much-needed local production.

There is a strong relationship between production and inflation, economists have noted. A fast inflation rate affects businesses’ planning negatively, leading to poor performance while a robust local production, as suggested by Johnson Chukwu, the chief executive of Cowry Asset Management Limited, “is the antidote” to the current inflation dilemma.

[ad]

“The only way we can fight inflation is to increase local production. The major cause of inflation is unrestrained importation. As long as we continue to rely on imported goods and services, inflation will continue to rise,” he added.

Indeed, Nigeria’s trade balance has remained negative in the past few quarters. Total imports rose by 33.77 per cent in Q3, 2020 compared to Q2, 2020 and 38.02 per cent compared to Q3, 2019. On the other hand, total exports in Q3, 2020 was 34.85 per cent higher than Q2, 2020 but 43.41 per cent lower than that of Q3, 2019.

In Q3 2020, the country’s total trade value stood at N8.37 trillion, with imports accounting for only 36 per cent or 2.99 trillion of the figures. Chukwu said the government has a responsibility to reverse the trade figures as a necessary action to keep the inflation rate low and stabilise the foreign exchange market.

The FX crisis, which is partly responsible for the growing inflationary pressure, is not over. The non-oil share of the exports is still very low while the crude market still faces headwinds as panic over COVID-19 lingers.

Meanwhile, economists said how the currency crisis is managed will ultimately determine the direction and magnitude of the inflation rate in the next 12 months.

[ad]

But FX is just a component of the inflation concern mix. Senior Economist/Head, Research & Strategy, Greenwich Merchant Bank, Ayodeji Ebo, told The Guardian that the energy cost and the price of petrol motor spirit (PMS) if they increase going forward, would heighten the pressure on the naira and reduce the purchasing power of especially the poor.

Investors in the electricity value chain have pushed for cost-reflective tariffs, saying that is the economic incentive needed to make the critical infrastructure bankable and attract fresh investments. Negotiation with the labour and other political exigencies have held up the implementation of the Multi-Year Tariff Order (MYTO), a model for incentive-based regulation that seeks to reward performance above certain benchmarks, reduces technical and commercial losses and lead to cost recovery while improving performance standards.

Also, the Ministry of Finance has disclosed that there is no provision for subsidy for petrol products, meaning that as the international oil prices continue to recover from the ruin of COVID-19, the price of the deregulated PMS is expected to adjust upward. Already, there are reports that the landing cost of PMS has increased.

Ebo asked Nigerians, who are already burdened by the deteriorating standard of living, to look forward to an upward adjustment in PMS price and consequently higher transport cost. This, he said, would trigger an even faster rise in the inflation rate, at least, in the next few months.

[ad]