Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

Nigeria is using bonds to temporarily solve the liquidity crisis in the power sector. But the pathway to a sustainable solution to the liquidity crisis that bedevilled the sector may remain far distant from the intervention, KINGSLEY JEREMIAH reports.

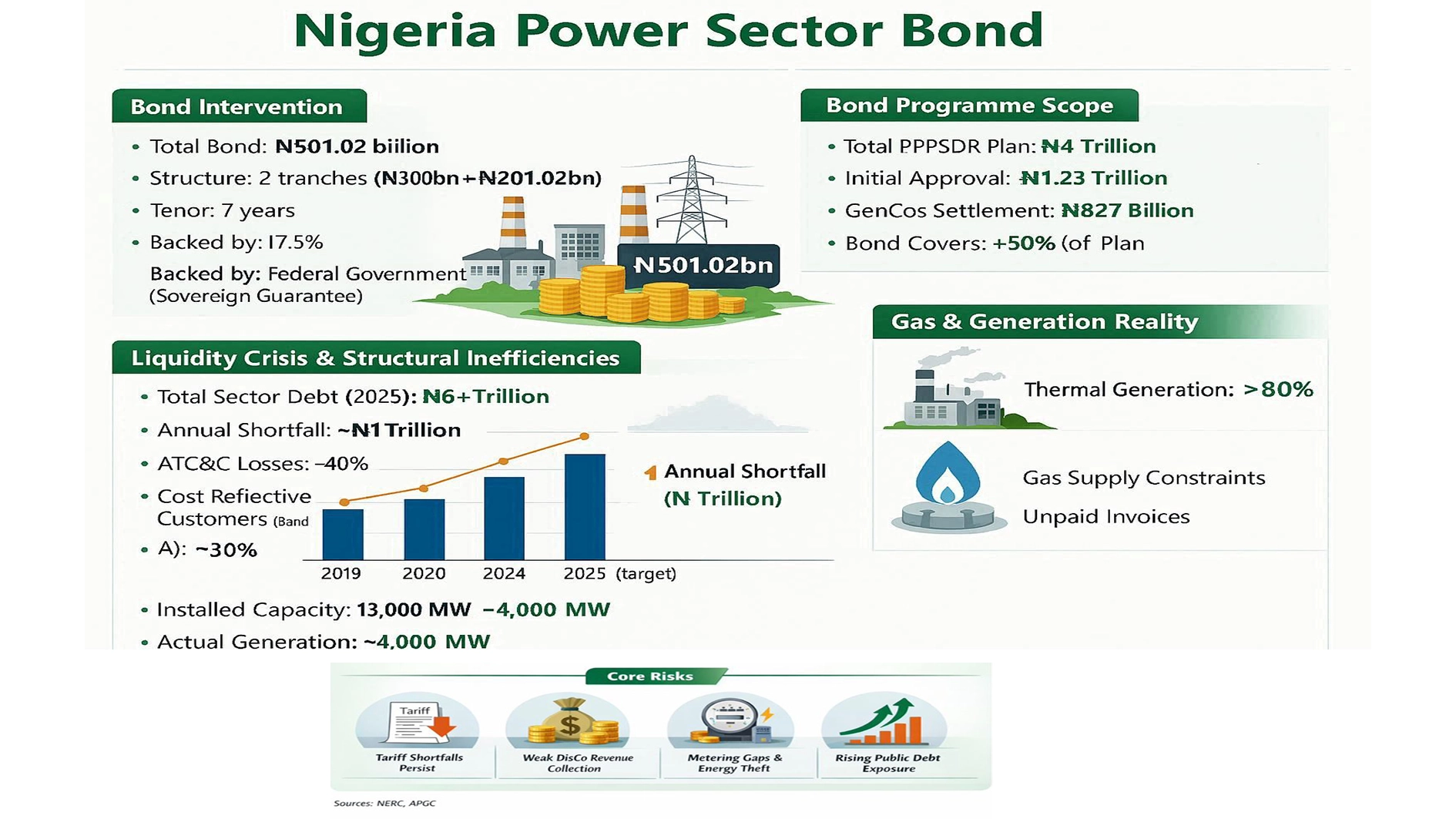

On the 27th of January this year, after a long period, Nigeria’s power sector appeared, at least briefly, to have found a financial relief. A series of high-level signing ceremonies heralded what could be called the first bond issuance targeted at addressing legacy debt in the power sector. This came after years of mounting debt, stranded capacity and eroding investor confidence. Backed by the Federal Government and described as a decisive intervention, Nigeria offered a N501.02 billion bond designed to inject liquidity into the cash-starved system.

While most policymakers saw it as the beginning of a reset, to many power generation companies (GenCos), gas companies and financial analysts, it was something more immediate, a financial lifeline. Yet beneath the optimism lies a deeper question: can a market weighed down by structural inefficiencies and chronic revenue shortfalls truly be rescued by a bond? How long will the government continue to back this bond in a sector that continues to accumulate about N1 trillion? What are the impacts of these solutions on Nigeria’s public debt, which continues to rise?

Nigeria’s electricity crisis is not one of scarcity, but of imbalance. More than a decade after the 2013 privatisation of the Nigerian Electricity Supply Industry (NESI), the sector continues to face a fundamental mismatch between what it costs to produce power and what consumers are able or required to pay. Now, only the band A customers, which the Nigerian Electricity Regulatory Commission (NERC) said accounts for about 30 per cent of the market, pay cost-reflective prices. This mismatch translates to about N1 trillion shortfall. Aggregate technical and commercial losses of about 40 per cent also meant that of every N100 of power invoiced, about 40 per cent is lost within the sector. While this political and social compromise, designed to shield consumers from price shocks, is expected to be backed by the budget, it is only theoretical. In practice, those subsidies are rarely paid in full in the face of fiscal chaos that forced 70 per cent of the 2025 budget to be rolled over, according to the Ministry of Budget and Economic Planning.

Cascading liquidity crisis and bond rescue

According to the Nigerian Bulk Electricity Trading Company, between May and October 2025 alone, 25 GenCos issued invoices totalling N1.531 trillion but received only N547.37 billion, just 35.7 per cent of their expected revenue. The outstanding N984.3 billion, largely attributed to tariff shortfalls, remains unpaid.

By December 2025, total debts across the power sector had surged beyond N6 trillion, according to the Executive Secretary of the Association of Power Generation Companies, Dr Joy Ogaji.

For operators, the implications include insufficient funds to service loans, maintain infrastructure or fund expansion. For gas suppliers, critical to Nigeria’s largely thermal generation base, which accounts for over 80 per cent, non-payment has translated into curtailed supply. For consumers, it has meant persistent outages, unstable grids and a power system that consistently underperforms its installed capacity.

It is against this backdrop that the Federal Government, through the NBET, introduced the Presidential Power Sector Debt Reduction Programme (PPSDRP), a N4 trillion initiative aimed at clearing legacy debts and restoring liquidity.

The N501.02 billion Series 1 bond, issued through NBET Finance Company Plc, a special purpose vehicle under the Nigerian Bulk Electricity Trading Plc (NBET), represents the first phase of that effort.

Structured as two seven-year instruments, N300 billion and N201.02 billion, both at 17.50 per cent, the bond carries a full sovereign guarantee. It is part of an initial N1.23 trillion approval, signalling a shift towards capital market financing rather than direct budgetary intervention. Since the budget is hardly implemented, a dedicated bond offers the sector a guarantee.

At the ceremony, the Special Adviser to the President on Energy, Olu Verheijen, described the programme as a “decisive reset” for the sector, aimed at restoring financial stability and rebuilding investor trust.

So far, 14 GenCos have signed Full and Final Settlement Agreements worth approximately N827 billion, with the bond proceeds expected to cover roughly half of these obligations in the first phase.

So far, 14 GenCos have signed Full and Final Settlement Agreements worth approximately N827 billion, with the bond proceeds expected to cover roughly half of these obligations in the first phase.

Acting Managing Director of NBET, Johnson Akinnawo, said: “This intervention will significantly improve liquidity across the value chain. It will enable operators to stabilise their operations and support renewed investment.”

If liquidity is the bloodstream of Nigeria’s power sector, gas is its oxygen. The current arrangement will provide succour to gas suppliers. Thermal plants, which account for the bulk of electricity generation, rely heavily on natural gas supplied by companies such as Seplat Energy Plc, Shell and Pan Ocean Oil Corporation. But years of unpaid invoices have strained these relationships to the breaking point. The major challenge for the sector currently is gas.

Ogaji had earlier decried the inability to pay gas companies and how that stalls supply.

If revenue from the bond reaches them, there are indications that supply will resume.

Without gas, it is difficult to generate power, no matter the installed capacity.”

Ogaji also noted that liquidity constraints have disrupted relationships with Original Equipment Manufacturers (OEMs), whose role in maintaining and servicing power plants is critical.

As a result, plant availability has dropped to an estimated 30 per cent in some cases across the industry, according to NERC’s reports. The bond, by improving cash flow, could reverse this trend.

Such improvements, while technical, have far-reaching implications for more reliable generation, stabilise the grid and improve service delivery.

For investors, the bond signals a renewed commitment by the government to address the sector’s financial dysfunction.

Minister of Finance and Coordinating Minister of the Economy, Wale Edun, represented by Patience Oniha, Director-General of the Debt Management Office, described the clearing of legacy debts as “not optional but critical.

“By settling these obligations in a structured manner, we are enabling GenCos to stabilise operations, improve maintenance and attract new investment,” he said.

Group Managing Director of Sahara Power Group, Kola Adesina, had also said the intervention could unlock new capital formation.

“Capital comes when there is confidence. Once this process is complete, construction will commence on the second phase of our Egbin Power Plant,” he said.

Cautious optimism vs temporary realism

Installed generation capacity in Nigeria stands at 13,000 megawatts, but what is dispatched daily is about 4000MW, a reflection not just of financial constraints, but of systemic inefficiencies across the value chain.

Clearing debts, while necessary, does not automatically resolve these deeper issues. For many players, the bond raises uncomfortable questions about the role of government in a privatised market.

Former Chairman of the Nigerian Electricity Regulatory Commission (NERC), Dr Sam Amadi, questioned the logic of using sovereign guarantees to settle what market debts are essentially.

“These are market obligations. Why is the government stepping in before a full review of how the debts were incurred?” he said.

Some stakeholders have also insisted that the bond market is not a magic wand, stressing that if underlying issues are not addressed, new debts will accumulate. These issues are non-cost-reflective tariffs, weak revenue collection, inadequate metering and poor financial discipline among distribution companies (Discos).

If GenCos are the immediate beneficiaries of the bond, the long-term sustainability of the sector depends largely on the performance of distribution companies. Discos sit at the frontline of revenue collection, yet many are plagued by technical losses, energy theft and inadequate infrastructure. Metering gaps persist, leaving millions of consumers on estimated billing, a system that undermines trust and revenue accuracy.

Managing Director of Azura Power, Edu Okeke, argued that debt clearance should have been accompanied by stricter conditions for Discos.

“Clearing the backlog should have come with cleaning their books and forcing recapitalisation. Otherwise, we risk being in the same position within a year.”

His concern reflects a broader consensus that views reform at the distribution level, liquidity injected upstream, may simply dissipate before it reaches the end of the value chain.

Former President of the Nigerian Economic Society, Prof. Adeola Adenikinju, said the bond represents a critical but incomplete solution.

Adenikinju said: “It is a necessary condition, not a sufficient one. Without cost-reflective tariffs, a credible subsidy framework and disciplined disbursement, it risks being remembered as another well-structured but ultimately insufficient intervention.”

Chief Executive Officer of Integrated Africa Power, Dr Chigozie Nweke-Eze, offered a similar assessment, saying, “This is a short-term stabilisation tool, not a structural reform,” he said.

According to him, it shifts private sector inefficiencies onto the public balance sheet, increasing sovereign debt and exposing taxpayers to long-term risks.”

His warning shows a central tension in the programme. While it may stabilise the sector in the short term, it also expands Nigeria’s public debt burden, raising questions about fiscal sustainability.

A stakeholder, Adetayo Adegbemle, said: “It is a major concern to believe that the Federal Government would consider a bond, which is another form of debt, to clear an ongoing debt.

He does not see the bond approach as a sound policy direction or a solution to the power sector debt, noting that the root of the power sector debts itself is not being addressed, and raising another debt in bonds is not one of the solutions.