Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover • Market size valued at $378.4 billion in 2019

• Market size valued at $378.4 billion in 2019

The global automotive aftermarket size was valued at $378.4 billion in 2019 and is expected to register a Compound annual growth rate (CAGR) of 4.0 per cent from 2020 to 2027, the latest report by grandviewresearch.com has revealed.

The report titled, ‘Automotive Aftermarket Industry Size, Share, Trends Report, 2020-2027’, noted that the market is majorly driven by the pursuit of automobile drivers to enhance their vehicle performance in terms of exhaust sound, speed, appearance, along with other aspects.

[ad]

Regional regulatory authorities, such as the Japanese Automobile Sports Muffler Association (JASMA), and the U.S. Environmental Protection Agency, monitor built-up standards and environmental impacts associated with automotive component functioning, for instance, noise emission levels associated with the modern-day resonators and mufflers in automotive exhaust systems.

However, it disclosed that digitisation of component delivery sales and services, along with online portals distributing aftermarket components in synchrony with global automotive suppliers, is expected to draw significant investments from the key participants.

[ad]

Owing to the above-mentioned trade gateways, the online aftermarket business is expected to witness high growth in developing countries. Additionally, increasing online sales of automotive components are estimated to further boost market growth.

Value chain of the aftermarket consists of two primary segments, automotive replacement part suppliers and service enablers. These prime industry segments exchange value through automotive sectors at several intermittent stages. Access to a considerable number of components along with simple transactions through digitalization, is expected to solve the obtainability issues, thereby driving the aftermarket growth.

[ad]

Ensuing digitalization and rising trend of Internet-of-Things (IoT) are anticipated to have a significant impact on industry growth.

Though technological improvements have created several market opportunities, high R&D expenditures are expected to hinder market growth over the forecast period. Automobile manufacturers face various constraints, such as increased production costs during manufacturing processes. However, some automotive replacement parts, such as aftermarket filters, offer the chance of choosing a part that suits the condition in which the vehicle operates.

[ad]

Replacement part insights

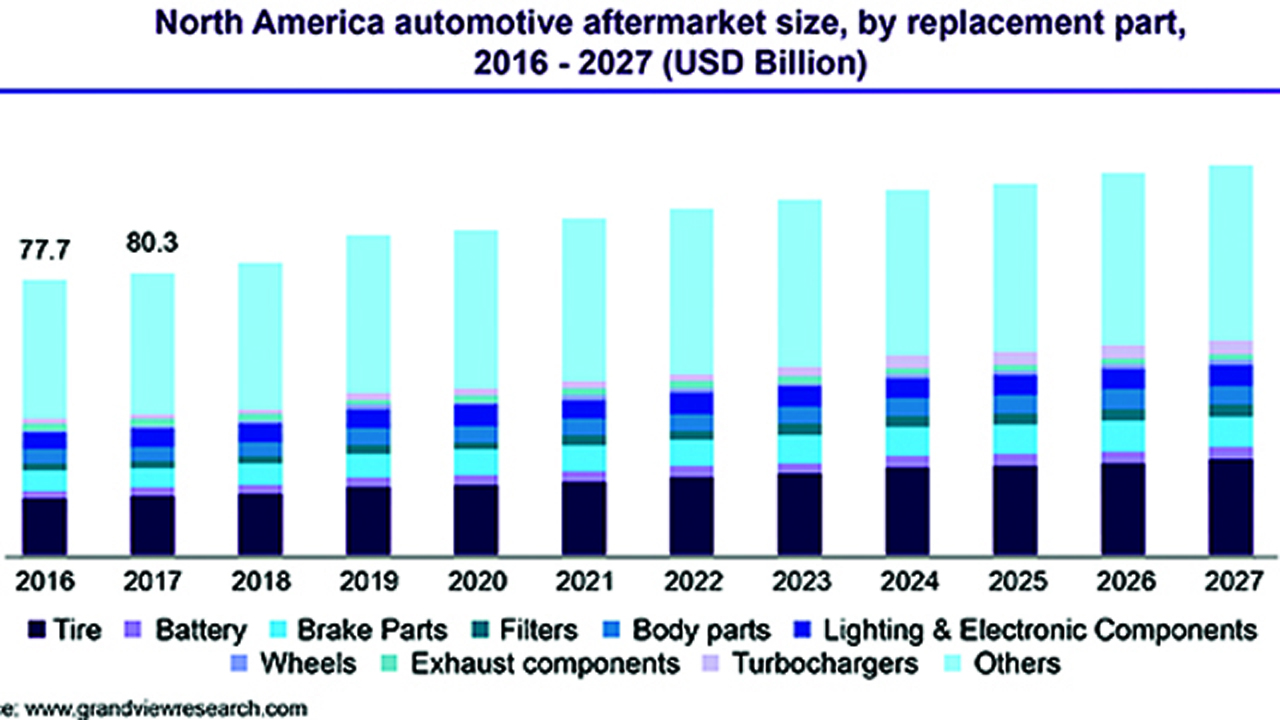

On the basis of the replacement part, the market is segmented into the tire, battery, brake parts, filters, body parts, lighting and electronic components, wheels, and exhaust components. The tire is anticipated to be the largest segment in terms of the replacement part and is expected to dominate the market in terms of size owing to the low replacement cycle of tires as compared to its counterparts.

The aftermarket replacement part suppliers include various accessories, lubricants and tires, and other component replacement suppliers. The industry value chain consists of service enablers, such as repairing services providers and entertainment service providers. The automobile industry is observing growth in demand for hybrid electric cars due to increased prices of petrol and petrol engine-based automobiles. This would eventually throttle the demand for exhaust parts and specific tools for these vehicles in the coming years.

[ad]

Increasing disposable income in developing countries, such as China and Brazil, is expected to have a positive impact on the aftermarket. Increasing demand for automotive is projected to trigger the demand for automobile component sales in the forecast period. Stringent regulatory rules and standards for car safety across the globe are anticipated to drive the market growth. Modern age production technologies, such as 3D printing of automotive parts that enable efficient fabrication and reduces emission, are being used extensively by major players in the aftermarket to optimize their production costs.

Distribution channel insights

On the basis of the distribution channels, the aftermarket is categorized into retailers and wholesale and distribution (W&D) segments. In terms of size, the retailer’s segment is anticipated to dominate the market, whereas the wholesale and distribution segment will witness the fastest growth from 2020 to 2027.

[ad]

The automotive aftermarket plays a significant role in the automotive manufacturing and maintenance scheme as automotive components need to be replaced on time to maintain the overall performance of the vehicle.

Technological advancements are transforming the market toward digitalization, leading to automotive components, parts, and services being sold online. Every player in the value chain, including Original Equipment Manufacturers (OEMs), Original Equipment Suppliers (OESs), wholesalers, insurers, and workshops are reacting to the growing online trend. Advanced technology used in automotive fabrication, rise in automobile manufacturing, and digitalization of automotive repair and maintenance services is some of the factors boosting the market growth.

[ad]

Service channel insights

On the basis of service channel, the aftermarket is segmented into Do It Yourself (DIY), Do It For Me (DIFM), and Original Equipment (delegating to OEMs). In terms of revenue, the OE segment is anticipated to dominate the aftermarket by 2027 while the DIY segment is expected to witness the fastest growth over the forecast period. DIY customers have technical knowledge and interest to maintain, repair, and upgrade their cars on their own whereas, DIFM customers buy parts online but get them installed by professionals.

The aftermarket service channel includes raw material suppliers, tier 1 distributors, and automobile exhaust hubs/manufacturing units and aftermarket units, comprising jobbers and repair shops. Repair centers are important stakeholders in the aftermarket service channel. The industry is witnessing a trend of strategic alliances and collaborations between collision repair centers and insurance companies to gain a competitive edge and capture a significant share in the market. For instance, Utica Mutual Insurance Company, State Farm Mutual Automobile Insurance Company, and Progressive Casualty Insurance Company have tie-ups with certified automotive repair shops across all the states in the U.S.

[ad]

Certification insights

On the basis of certification, the aftermarket is segmented into genuine, certified, and uncertified. The genuine segment is anticipated to dominate the aftermarket in terms of size by 2027 while the uncertified segment is expected to witness the fastest growth from 2020 to 2027. Genuine parts are manufactured by the car manufacturers or by the OEMs, also known as subcontractors.

Genuine replacement parts have greater quality assurance, are diverse, easy to find, and come with manufacturing warranty. The downside, however, is that they are expensive and need to be purchased from authorized dealers.

[ad]

Certified automotive parts are tested and inspected by certified organizations. The Certified Automotive Parts Association (CAPA) is a non-profit organization that was incorporated in 1987, to ensure the quality of replacement parts used by collision repair shops. CAPA offers test programs to verify and guarantee the quality and suitability of automotive replacement parts. Certified parts are cost-effective alternatives to costly genuine parts whereas, uncertified parts can be used instead of original automotive parts. Uncertified parts are not approved by the carmaker. However, the low cost of uncertified parts is anticipated to create significant growth opportunities for the segment in the coming years.

Regional Insights

Based on region, the aftermarket is segmented into North America, South America, Europe, Asia Pacific, and MEA. Asia Pacific led the aftermarket in terms of revenue in 2019 and is also expected to witness significant growth from 2020 to 2027. Advanced technology usage in the fabrication of auto parts, surge in consumer and passenger automobile production and sales, and digitalization of automotive component delivery services are anticipated to spur the automotive sales in the region.

Universities and other R&D organizations are working toward increasing the cost and operational efficiencies of critical automotive components, thus reducing the price of the end product.

[ad]

A new design, developed by a team of researchers from the Department of Chemical Engineering at Imperial College, London, uses up to 80% less rare metal, reducing costs of the vehicle and component fabrication considerably. The prototype is anticipated to exhibit better results than the existing automobiles.

Strict vehicle emission rules by governments across the globe have also pressurized component suppliers to manufacture environment-friendly and high-efficient automotive components for the native and global markets. Over the past few years, emerging economies, such as China, India, and Brazil have witnessed considerable developments in the automotive sector, which is expected to boost market growth in the Asia Pacific.

Automotive aftermarket share insights

Some of the key industry participants in the aftermarket are Continental AG, 3M Company, Delphi Automotive PLC, Federal-Mogul Corporation, Denso Corporation, Magneti Marelli S.p.A., and Robert Bosch GmbH. Technological advancements and increasing investments in R&D by manufacturers are expected to drive the aftermarket. Several domestic and regional competitors prevailing in the market are challenged to offer innovative products to help buyers understand the changing technologies, security needs, and business practices.

[ad]