Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

• Five banks hold N11.8 trillion govt securities • Economic distress real concern, say experts

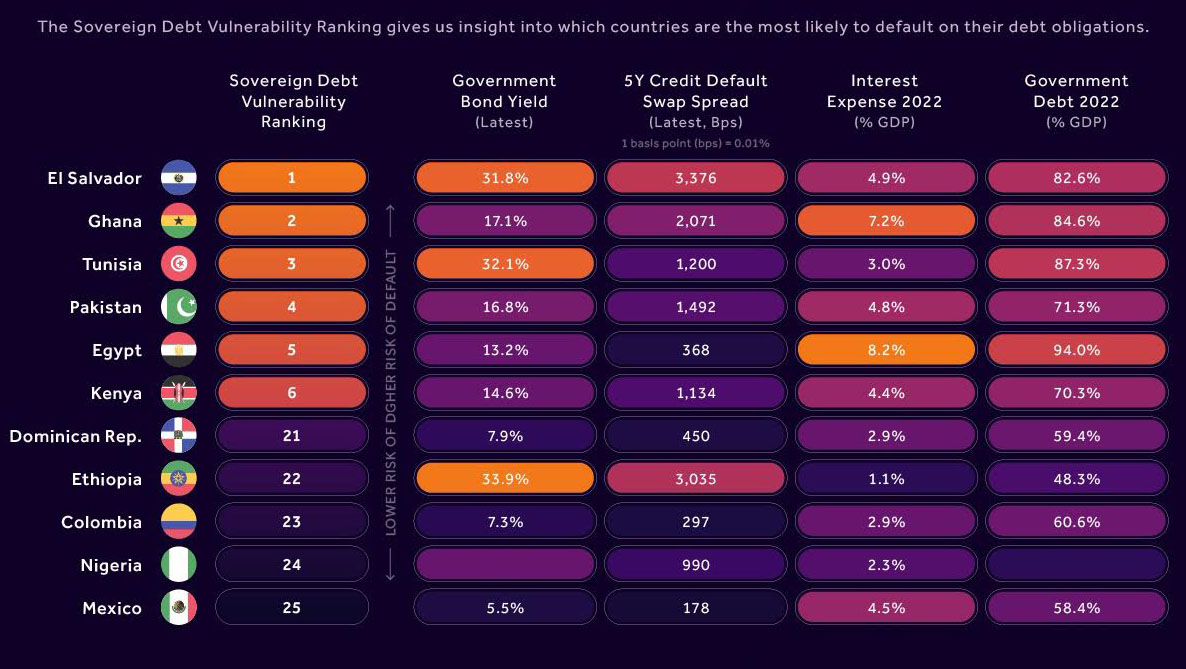

• As Nigeria, Kenya show signs of replicating Ghana’s path • Lenders urged to restrict NPL to less than 10%

• ‘Concerns about default are tenable, debt-to-revenue ratio is rising’

As African governments fight to stave off debt distress, experts have expressed fear that a likely default could create a wide hole in the books of Nigeria’s banks and erode their profitability.

[ad]

This comes as checks by The Guardian revealed that First Bank, Zenith Bank, GTCO, Access Corp and United Bank for Africa had a combined N11.84 trillion investment in government securities in 2022 up from N9.99 trillion invested in 2021.

With major banks already taking a haircut from the Ghanaian debt crisis in their 2022 financials, there is rising tension in the banks about how another default by Nigeria, Kenya or any other African country, where the financial institutions are highly exposed to sovereign securities, could affect the operators.

Reports said Kenya could default as close as next year while Nigeria, though with a more resilient economy, spent over 99 per cent of its revenue on debt servicing last years’ first three quarters with zero remittance to a sinking fund for maturing debt.

Experts said the revenue profile of the country must be shored up significantly to avoid a default and stabilise the fiscal position. The removal of fuel subsidy holds a huge prospect in stabilising public finance but a higher minimum wage could be another major drain on the public purse.

Experts said the government’s default on bond payment without a well-diversified investment portfolio of banks could trigger a crisis in the entire industry.

This is because foundational issues that drove Ghana’s economy to its current distressed state are predominant in the nation’s economy.

Although Nigeria has never defaulted on its debt payments, experts warned that similar crisis like that of Ghana could happen in Nigeria, which could be catastrophic unless appropriate risk management is put in place by the Central Bank of Nigeria (CBN) to ensure that banks’ exposure to countries’ sovereign bonds does not pose any material danger to their balance sheet.

Already, the default by Ghana government is currently eliciting relatively higher impairment charges on sovereign bonds of many sub-Saharan African countries, including Nigeria as the yields on these emerging market bonds trend upward at the international capital market.

Hence, investors in the debt instruments issued by African countries have adopted cautious trading.

“Nigeria is rapidly running out of its limited credit line. Right now, our credit space is very limited, not because we have a high debt-to-GDP ratio, but because our revenues are too small to support the size of our debt. This explains our high debt service ratio,” an analyst explained.

“When a country’s debt service ratio goes over 30 per cent, it is in trouble. But we’re aiming for 100 per cent, which shows how big a problem we are in. The next step would be to consider the government’s priorities for what projects get what,” Head of the Budget Office, Dr Ben Akabueze, had stated.

An independent investor, Amaechi Egbo said the yield environment has been significantly high, which has made it difficult for the Federal Government to save in terms of debt service.

[ad]

“Yes, the concerns about default are tenable, there is no security, whether sovereign or otherwise, that is 100 per cent secured. Nigeria’s debt-to-revenue ratio is worsening, Nigeria’s debt stock has grown significantly and still growing, unless something meaningful is done to reverse these trend, I am afraid, the worst can happen, banks must tighten their risk management framework and ensure that their loan is not bad,” He said

Head of Research, FSL Securities, Victor Chiazor, urged banks to ensure that they do not have a significant portion of their investments or credit going bad, noting that this could lead to bank’s total collapse.

“Banks should ensure that their bad loans do not exceed 10 per cent of their total loans and investments. When bad loans and investments rise to up to 40 or 50 per cent, most banks are likely to collapse.”

Vice Chairman of Highcap Securities, David Adonri, said the exposure of Nigerian banks to foreign sovereign bonds should follow due risk management process to minimise any harm while maximising income.

According to him, the CBN, being in charge of monetary policy and banking supervision, ought to regulate this aspect of banking strictly.

“They have prudential guidelines and risk management framework that banks must follow in order to remain sound. If these regulations are enforced, exposure of banks to local and foreign sovereign risks will be minimised.

“Therefore, he called for the diversification of bank’s risk assets, including foreign assets as an important risk management tool to reduce unsystematic risk”, he said, noting that this must be done in a manner that does not cause any harm.

Head Equity, Planet Capital, Dr Paul Uzum, urged banks to learn from the Ghanaian experience, and ensure they prepare adequately for the possibility of such eventuality from the federal government.

[ad]

“Whilst banks pursue Eurobond investment with high yields, they should not compromise risk or safety of such investments. Again, they need to maintain a well-diversified investment portfolio of their dollar assets to reduce the risk.

“The banks invest their dollar deposits and dollar reserves in Eurobonds issued by countries or corporations to earn interest, if they over concentrate their investment in Nigeria Eurobond and the Nigerian government defaults in payment, such banks would definitely collapse, ” he said.

Recently, the World Bank warned that Nigeria’s debt service-to-revenue ratio could reach 160 per cent within five years unless extensive reforms are implemented to free up fiscal space.

Nigerian banks held direct and indirect (through subsidiaries) Ghana Eurobond holdings of about ₦800 billion (or $1.7 billion), accounting for an estimated five percent of the industry’s total investment securities as at December 31, 2022, a report by Agusto & Co said.

A look at the impact on Nigerian banks showed that GTCO reported a N35.94 billion net impairment charge on its financial assets for the 2022 full year performance, up from N760.79 million recorded in the previous year. The provision led to a 3.33 per cent drop in GTCO’s profit before tax (PBT) to N214.15 billion.

Access HoldCo Plc, the parent company of Access Bank, the biggest Nigerian bank by asset, reported a five per cent fall in PBT from N176.6 billion in full year 2021 to N167.7 billion in 2022 following a write-down from Ghana’s sovereign debt crisis.

Analysts at Agusto & Co said the capital position and performance of the top Nigerian banks: Access Bank Plc, Zenith Bank Plc, United Bank for Africa Plc and Guaranty Trust Bank Plc), which were the most impacted, would remain strong in the near term, while the average capital adequacy ratio of the banks are expected to exceed 15 per cent regulatory minimum for international banks.

It stated that, however, the Ghanaian subsidiary of the top Nigerian banking institutions would continue to put pressure on their group’s performance, asset quality and capitalisation.

“It is noteworthy that the Ghana subsidiaries of these banks, in addition to being exposed to the government securities, are impacted by the prevailing economic turmoil that has weakened their asset quality and earning power as the Ghanaian cedi depreciates against the dollar, interest rate rises and inflation remains high,” it added.

[ad]