Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

By Lanre Babalola

Recap from part one

In part one of this article, we traced how an incomplete transition from a centralised to a market-based electricity sector — and the open-ended sovereign commitments made at the moment of privatisation in 2013 — created the structural conditions for chronic debt accumulation. The payment arrears owed to generation companies and gas suppliers now stand at approximately N6.8 trillion, growing at N200 billion every month. The full sovereign exposure, when all instruments, facilities, and contingent commitments are considered, is substantially larger. And the World Bank estimates that unreliable electricity costs the Nigerian economy approximately $29 billion every year. Part Two asks: what must a credible response look like, and why is the current intervention — necessary as it is — not yet sufficient?

Necessary but not sufficient: The limits of debt settlement

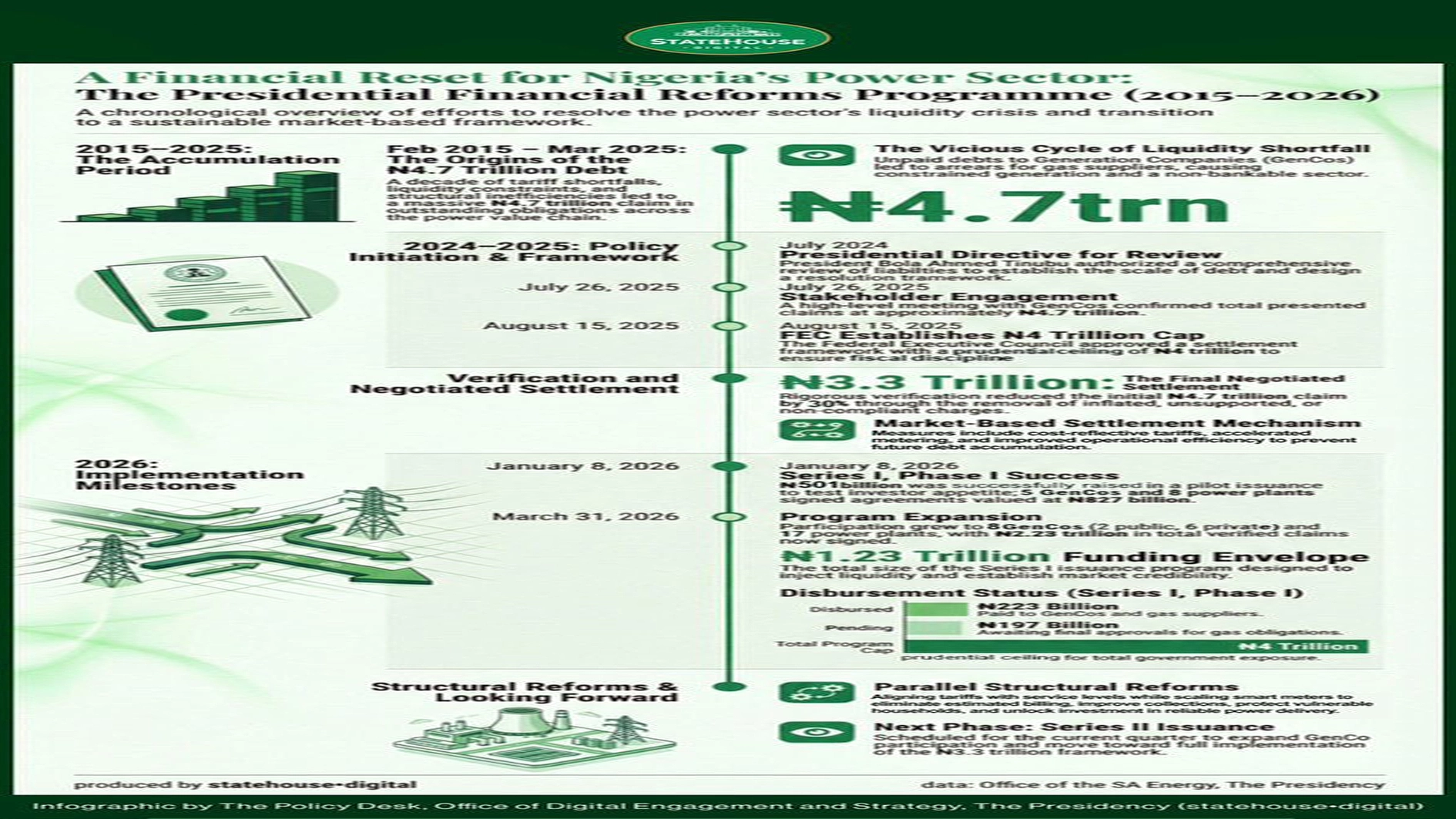

The Presidential Power Sector Financial Reforms Programme (PPSFRP) is a necessary intervention and should be recognised as such. Clearing the accumulated arrears owed to generation companies and gas suppliers is the essential first step toward restoring the sector’s operational credibility.

Gas suppliers will not expand supply to a sector that cannot service its existing obligations. Generation companies cannot maintain their plants, source spare parts, or service their own financing obligations if their invoices are honoured at less than 30 per cent. The bond programme creates the conditions under which upstream market participants can begin to function with something closer to normal commercial logic. That matters and it should be said plainly.

But the bond programme addresses a stock of accumulated debt. It does not address the flow that generates new debt at N200 billion every month. That flow is structural. It arises from the gap between what generation companies invoice, what distribution companies collect from consumers, and what the government disburses in subsidy to bridge the difference — a three-way mismatch that the bond programme does not touch. The moment the bond programme settles legacy arrears, the clock starts again. Unless the conditions that generate the gap are simultaneously addressed, the N4 trillion intervention risks becoming the first instalment of a recurring exercise rather than the structural reset it has been described as.

Addressing the structural flow requires reforms that are harder, slower, and more demanding than bond issuance. It requires an operational escrow for all distribution company revenue collections, with mandatory payment cascade rules — sometimes called a waterfall — that assure payment to gas suppliers and generation companies before any other claim on collected revenue is honoured.

It requires enforceable loss reduction targets for distribution companies, because a sector that loses 45 to 50 per cent of what it generates between the power station and the paying consumer cannot be made commercially viable by any tariff adjustment alone. It requires a tariff governance framework that is insulated from the political cycle and oriented toward rewarding operational improvement rather than guaranteeing revenues irrespective of performance.

And it requires the progressive development of the direct contracting framework that the 2005 reform envisaged — one in which the market matures to the point where generators and large consumers can transact on terms that reflect real supply and demand, and the intermediary role of the central purchasing function narrows as the bilateral market grows to sustain it. This is the completion of a reform journey that began two decades ago and has not yet reached its intended destination.

There is a further dimension that receives almost no attention in the current policy conversation: the relationship between new infrastructure investment and the accumulation of sovereign fiscal exposure. Every new power plant commissioned under a power purchase agreement, every new loan borrowed from a multilateral lender to build or rehabilitate grid infrastructure, every new megawatt of capacity added to a sector whose commercial architecture remains unreformed — each of these creates new sovereign obligations that the sector, in its current state, cannot fully service from its own revenues. The debt service falls on the government.

The fiscal footprint grows. This is not an argument against infrastructure investment — the country clearly needs more and better infrastructure. It is an argument for sequencing and for ensuring that commercial reform proceeds alongside physical investment, so that the assets built can generate returns sufficient to contribute to their own financing costs. Capacity added to an unreformed commercial system does not solve the fiscal problem. It adds to it.

The shape of a credible response

A credible response to the electricity sector’s fiscal problem has three essential characteristics. It must be comprehensive — calibrated to the full range of sovereign exposure, not merely the portion that has so far been publicly quantified. It must be structural — designed to arrest the accumulation of new liabilities, not merely to settle existing ones. And it must be sequenced — because the order in which interventions are made determines whether they reinforce each other or work at cross-purposes.

The first and most urgent requirement is an honest and complete accounting. Before a response adequate to the sector’s fiscal challenge can be properly designed, the challenge must be known in its totality. This means bringing together, for the first time in consolidated form, the full range of the sovereign’s electricity sector obligations: the generation and gas payment arrears, the Central Bank intervention facilities, the pre-privatisation legacy liabilities, the multilateral loan portfolio, capital programme commitments, contingent obligations embedded in power purchase and gas supply contracts, and the indirect exposure arising from the government’s equity in entities whose commercial bank debts remain under strain. No such consolidated account exists in one place. Compiling it is a prerequisite for rational liability management. A problem that has never been fully measured cannot be fully managed.

The second requirement is commercial stabilisation. An operational escrow for distribution company revenue collections, with payment cascade rules that protect gas suppliers and generation companies at the top of the priority order, is the mechanism that converts the bond programme from a one-off settlement into the foundation of a sustainable commercial regime. Without it, the bond creates fiscal space that is refilled by the structural shortfall each month. With it, collections begin to flow in the direction the market’s incentives require — toward those who produce the electricity, ensuring they remain able and willing to continue producing it.

The third requirement is a serious, sustained, and measurable commitment to loss reduction. Technical and commercial losses, which consume 45 to 50 per cent of generated electricity, are not immutable features of the landscape. They are the consequence of inadequate metering, insufficient network investment, poor billing infrastructure, and the absence of regulatory enforcement with genuine consequences. Distribution companies that reduce losses generate more revenue from the same electricity volume.

That additional revenue reduces the subsidy burden, slows the monthly accumulation of new sovereign liability, and creates the fiscal headroom within which further reform becomes financially possible. Loss reduction is not a glamorous policy. It does not attract the headlines that a new power plant generates. But in terms of fiscal return per naira of effort, it is among the most valuable interventions available to the sector.

A further requirement is discipline in new investments. The case for expanding and rehabilitating the transmission and distribution network is not in dispute — the infrastructure deficit is real and its consequences are visible. But the scale, sequencing, and financing of that investment should be grounded in a verified technical assessment of what the existing network can actually carry under operational conditions, not in design specifications alone.

And the financing of new infrastructure through sovereign borrowing should be accompanied by a clear commercial plan for how the assets built will generate returns that contribute to their financing costs. Infrastructure borrowed into a structurally unreformed sector is not a solution to the sector’s problems. It is a new layer of the same problem in a different form.

The wider stakes

Nigeria has undertaken a bold and ambitious macroeconomic reform programme. Exchange rate unification, the removal of fuel subsidies, monetary tightening — these are serious structural adjustments with real costs, undertaken in pursuit of a more sustainable and productive economy. Their sustained success depends, among other things, on the availability of fiscal space in which to manage transitional burdens and fund the investment priorities that growth requires. The electricity sector’s fiscal footprint is a direct, growing, and insufficiently acknowledged claim on that space.

The N6.8 trillion in payment arrears, the N200 billion monthly shortfall, and the broader range of obligations that sit alongside the headline figure are not a sector problem that happens to have fiscal implications. They are a fiscal problem of the first order, arising from two decades of structurally misaligned incentives, an incomplete transition from centralised to market-based electricity trading, and the gradual absorption of commercial risk into sovereign instruments that were never designed for indefinite duration.

The World Bank estimates that Nigeria’s economy loses approximately $29 billion every year to unreliable electricity. That cost — borne by manufacturers, hospitals, schools, and households across the country — is the other face of the same structural failure that has generated the debt burden on the government’s books. The two are not separate problems. They are the same problem expressed in two different registers: one fiscal, one economic.

The PPSFRP signals that the government has recognised the gravity of the most visible dimension of this problem. That recognition matters and should be the foundation for a broader response. What must follow is action calibrated not merely to the dimension that has been recognised, but to the full scale of the challenge that has been building. Paying N4 trillion into a system that generates N200 billion in new obligations every month, without repairing the mechanism that drives that accumulation, is a necessary beginning.

It should not be mistaken for a sufficient conclusion. The electricity sector’s debt is a problem of architecture, not just of accounting. Completing the architectural work — the commercial reform, the loss reduction, the market development, the consolidated liability management — is the task that will determine whether the bond programme becomes the foundation of a genuinely reformed sector, or simply the most expensive in a long series of interventions that deferred rather than resolved the underlying challenge.

Dr Babalola is a former Minister of Power and was one of the principal architects of Nigeria’s electricity sector reform. Through Exenergia Limited, he works on infrastructure development, electricity industry policy, regulatory economics, and the macroeconomic dimensions of energy infrastructure failure. He also writes The Missing Markets, a Substack newsletter examining the markets, institutions, and infrastructure gaps that constrain growth in developing and emerging economies.