A report has revealed a five per cent drop in network investments by telecommunications operators across the globe in 2023 and said there could be further cuts in capital expenditure in 2024.

Research house, Dell’Oro Group, noted that spending by operators on network technology products dipped by five per cent year-on-year in 2023 after five consecutive years of increasing investments.

While the Dell’Oro team didn’t share a value for the market, its previous insights pegged the global spending in six telecoms networking technology categories – broadband access, microwave transport, optical transport, mobile core network (MCN), radio access network (RAN), and service provider router and switch – at about $100 billion in 2022, which puts the 2023 total at about $95 billion.

According to it, multiple factors, including the buildup of network technology inventories by network operators and supply chain issues, contributed to the reduced spending, particularly in the RAN and mobile core system sectors, but it wasn’t just mobile network investments that suffered a decline, noted Dell’Oro Vice President and Analyst, Stefan Pongratz, in his latest blog about the telecoms network equipment market.

“Following a couple of years of robust passive optical network (PON) investments, operators were able to curtail their home broadband capex as well. This reduction was more than enough to offset positive developments with optical transport and SP routers,” he stated.

Dell’Oro observed that major capex cuts by the top U.S. telcos had a significant impact, explained Pongratz, saying: “North America subsided faster than expected. Initial readings show that the aggregate telecoms equipment market dropped by roughly a fifth in the North American region, underpinned by weak activity in both RAN and broadband access. On the bright side, regional dynamics were more favourable outside of the U.S. Our assessment is that worldwide revenues excluding North America advanced in 2023, as positive developments in the Asia Pacific region were mostly sufficient to offset weaker growth across Europe,” he noted.

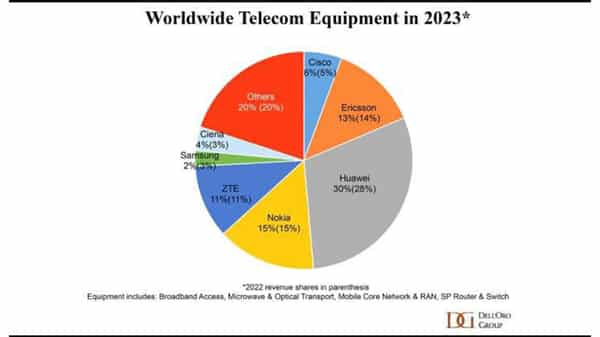

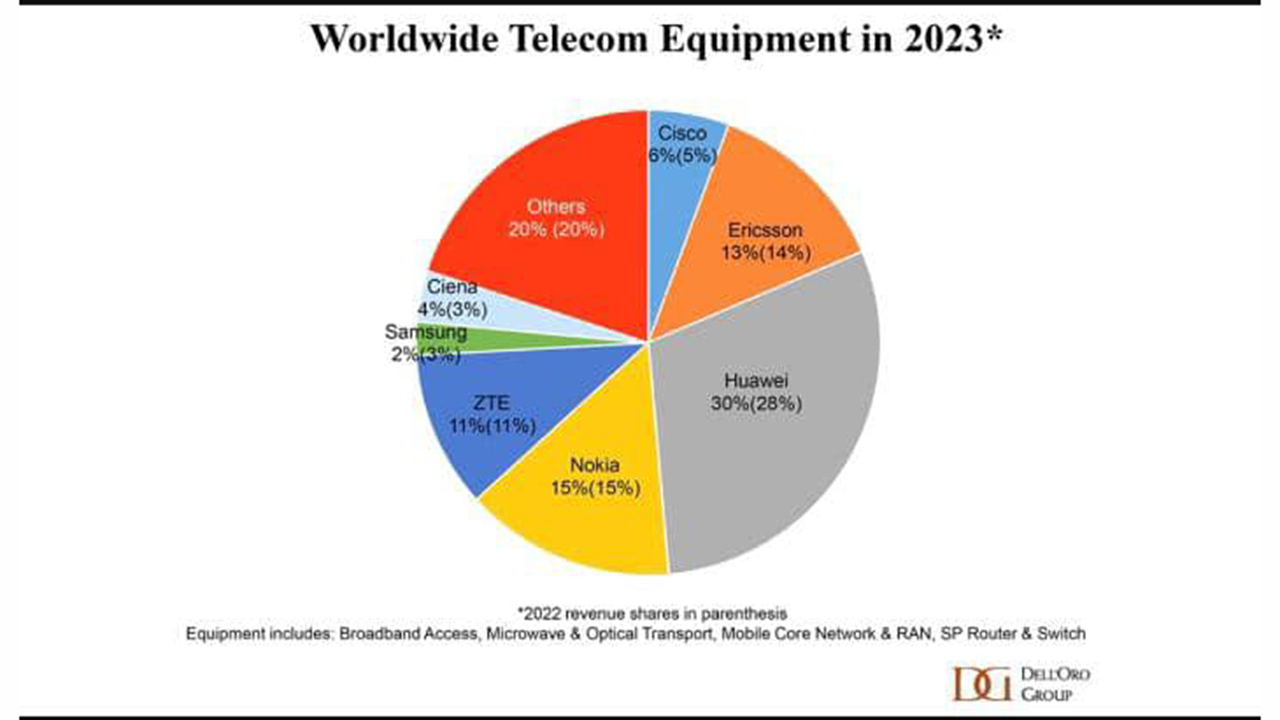

It stressed that while the numbers change, the vendor ranking remains pretty much the same. Helped by the significant investments of the three main operators in its domestic market, as well as its ongoing supplier relationships with network operators in many markets around the world (despite being barred in some countries for security reasons), Chinese firm Huawei Technologies is by far the biggest single vendor, with a 30 per cent global market share, followed by Nokia with 15 per cent and Ericsson with 13 per cent.

The top seven vendors accounted for 80 per cent of the global market, according to Dell’Oro’s calculations. According to Dell’Oro, that network operators tightened their purse strings was apparent in the financial reports of most vendors throughout 2023 and this was hammered home by the full-year reports issued by the major vendors during the first three months of this year.

According to it, not only did the likes of Ericsson and Nokia report significant year-on-year sales declines, but they also warned of a challenging economic environment in 2024.