Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

A text analysis of 227 public discussions on merchant acquiring highlights where businesses get stuck most often: gateway configuration and plugins, jurisdiction rules, chargebacks, reserves, and payout timing. Here is what the data shows and what Nigerian exporters can do.

What the data shows

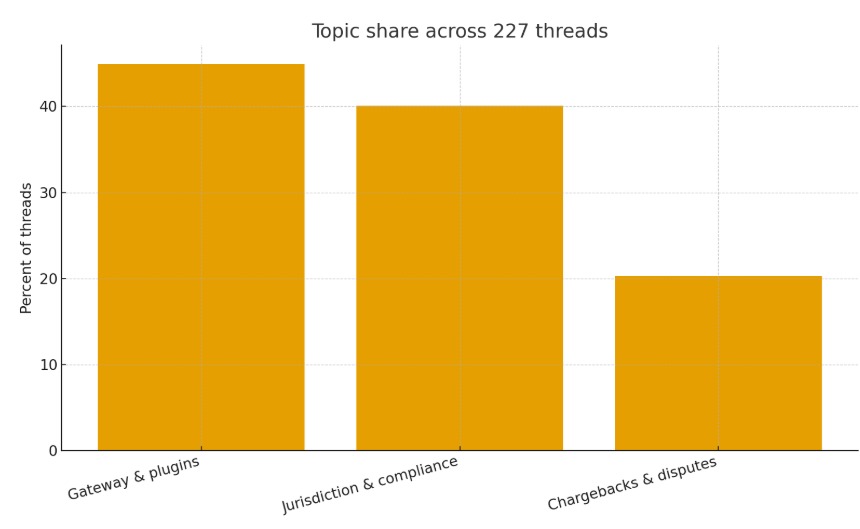

We reviewed 227 public threads from OffshoreCorpTalk’s payment and banking sections and classified first posts by topic and by operational signals. Gateway and plugin issues are the most common theme. 44.9% of threads include questions about gateway setup, plugin maturity, tokenization, subscription renewals, or refund handling. Jurisdiction and compliance topics appear almost as frequently at 40.1%, often when merchants test cross-border flows or encounter regional authentication requirements. Discussions that touch chargebacks and dispute handling account for 20.3% of threads.

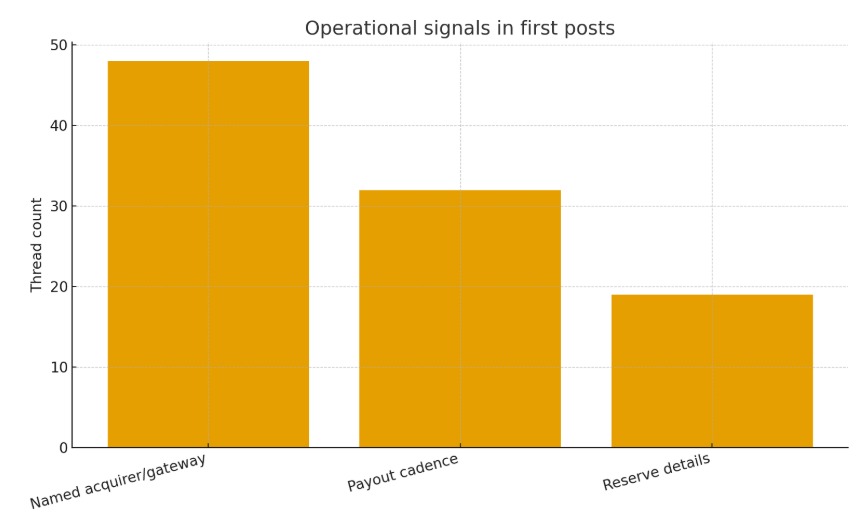

Operational signals reinforce this picture. We see specific acquirer or gateway names in 48 threads, payout calendars or cut-off rules in 32 threads, and reserve formulas or release cadence in 19 threads. The language in first posts is pragmatic. Merchants describe caps during a pilot, adjustments to authentication rules, refund targets, and what happens when funding slows after a spike in disputes.

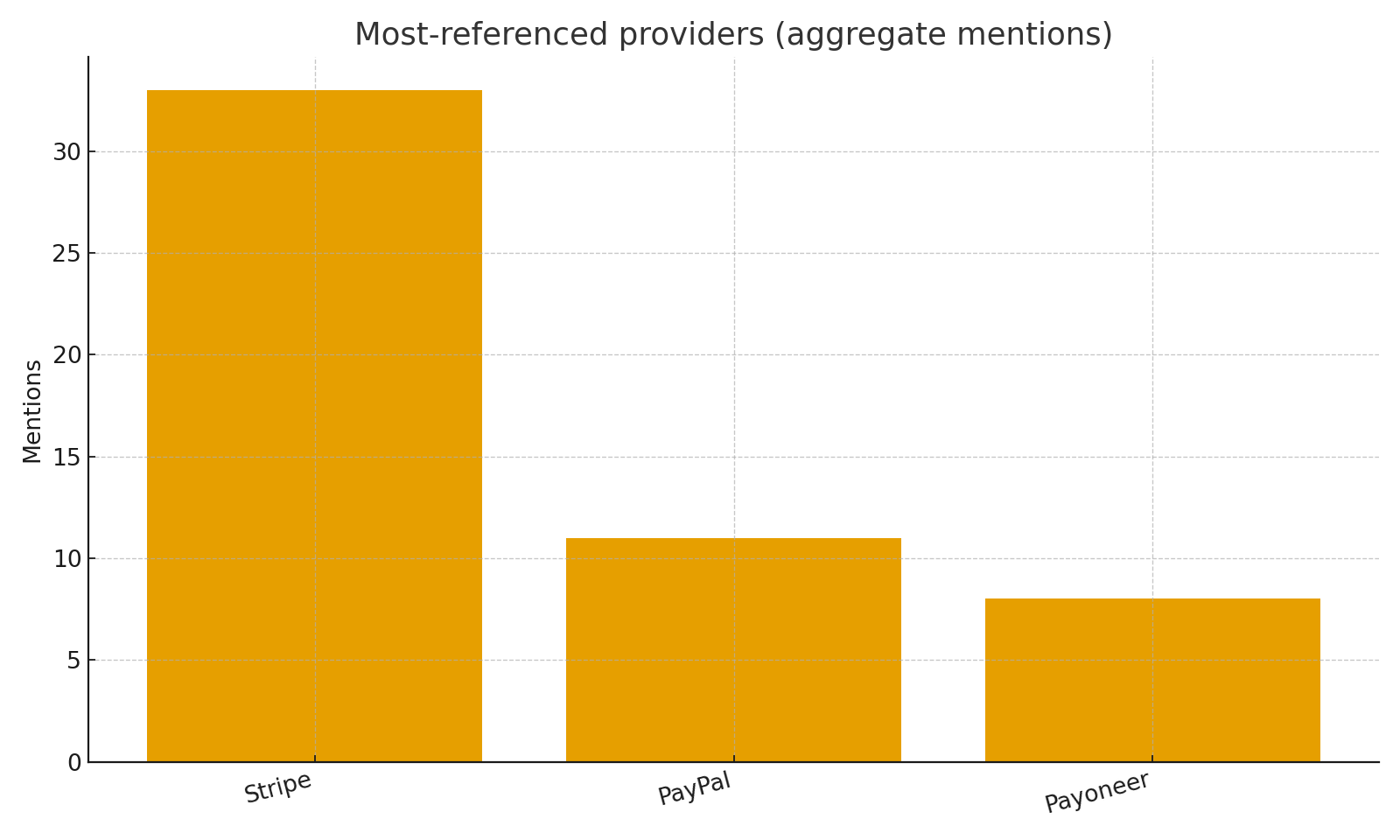

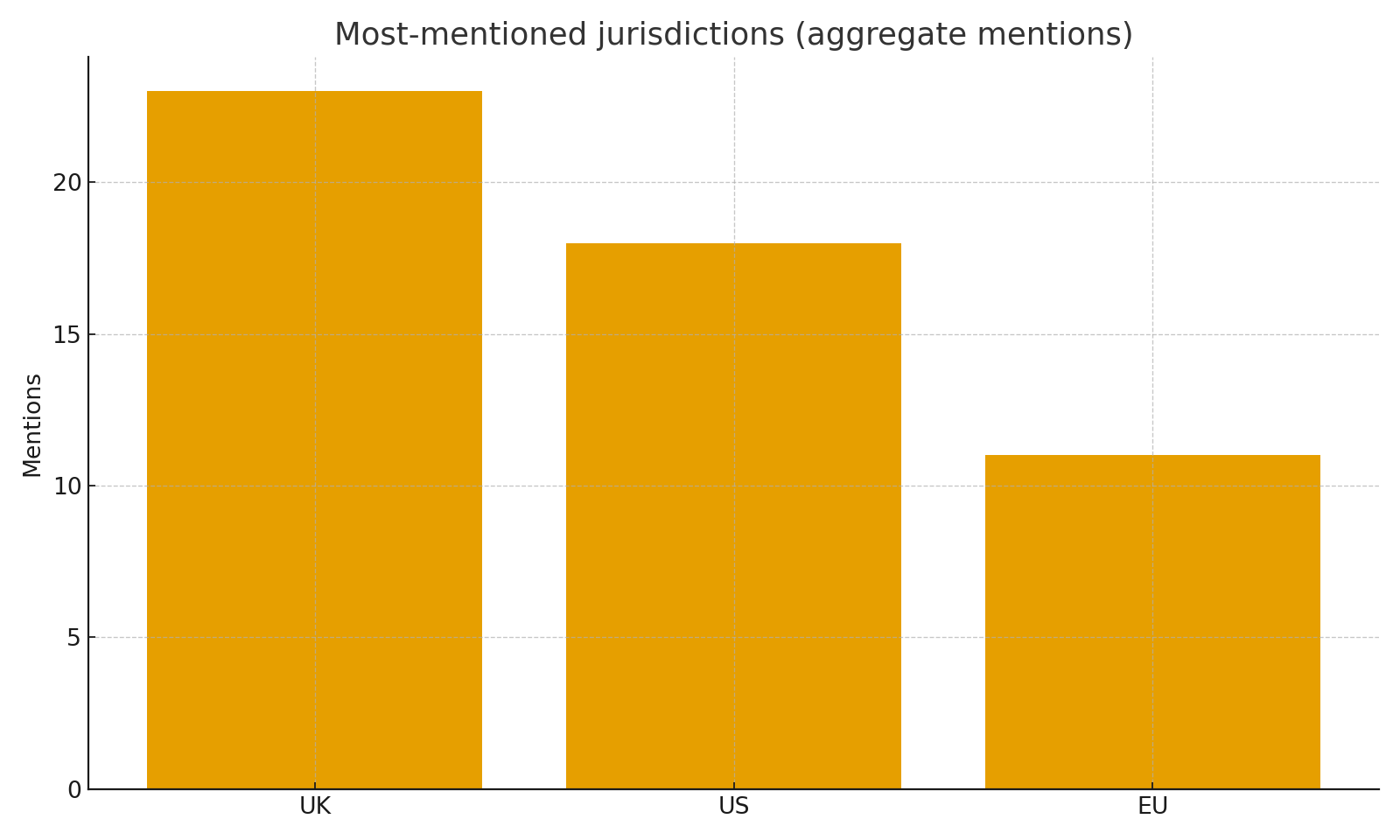

Mentions of providers are concentrated in a small set. The three most referenced families are Stripe (33), PayPal (11), and Payoneer (8). Mentions of jurisdictions cluster around UK (23), US (18), and EU (11). We list aggregate counts only and avoid endorsements.

Volume is not static. Threads peak in 2024 Q3, which aligns with periods when posters describe policy updates, gateway version changes, and tighter risk controls.

Figure 1. Topic shared across 227 threads. Gateway and plugin issues are referenced in 44.9 per cent of first posts, jurisdiction and compliance in 40.1 percent, chargebacks and dispute handling in 20.3 per cent.

Figure 1. Topic shared across 227 threads. Gateway and plugin issues are referenced in 44.9 per cent of first posts, jurisdiction and compliance in 40.1 percent, chargebacks and dispute handling in 20.3 per cent.

Figure 2. Operational signals. Named acquirer or gateway appears in 48 first posts, payout cadence in 32, reserve formulas in 19.

Figure 3. Mentions of providers. Most referenced families: Stripe, PayPal, Payoneer.

Figure 3. Mentions of providers. Most referenced families: Stripe, PayPal, Payoneer.

Figure 4. Mentions of jurisdictions. Mentions cluster around UK, US and EU.

Figure 4. Mentions of jurisdictions. Mentions cluster around UK, US and EU.

Where merchants struggle

Underwriting facts

Many first posts ask the same three questions. Who is the acquiring bank. Which MCC will be assigned? Will the merchant be on a unique MID? When these answers are vague at onboarding, funding becomes unpredictable later, especially during audit cycles or when disputes increase.

Authentication and dispute readiness

Enabling 3-D Secure 2 moves issuer fraud liability in many cases, but it does not eliminate disputes. The recurring wins in the dataset are practical. Use clear descriptors that resolve to a branded help page. Keep evidence templates by reason code. Answer alerts within the window. Refund quickly when appropriate.

Reserves and funding

The most difficult moments in the threads are not approvals. They are reserve changes, a switch from daily to weekly funding, or new volume caps. Surprise comes when there is no written formula or cap at the start.

What this means for Nigerian exporters

- Treat onboarding as a contractual specification. Get the acquirer name, the MCC, the reserve formula with a hard cap, and the funding calendar and cut-offs in writing.

- Turn on 3-D Secure 2 with risk-based rules. Challenge high-risk traffic and let low-risk flows pass to protect conversion.

- Prepare reason-code evidence packs and refund service levels. The best outcome is to resolve alerts before a dispute is filed.

- If you run subscriptions, test renewals, proration, partial refunds, and descriptor display in a sandbox before you switch real traffic.

- Keep a pilot cap for 8 to 12 weeks so any change to reserves or funding can be managed without business disruption.

Buyer’s checklist before you switch traffic

- Which bank acquires the transactions and in which country are funds settled

- What MCC will be assigned and what rules follow from that MCC

- Unique MID confirmation. If shared, what are the controls

- Pricing line items: discount, per item, cross border, assessments, gateway, tokenization, batch, monthly minimum

- Reserves: formula, release cadence, and a hard cap on total balance held

- Funding calendar, daily cut-off time, and the specific triggers for weekly funding

- Disputes: 3-D Secure 2 directory servers, alert programs and fees, representment workflow and deadlines

- Technology: who owns the gateway and SLA, official plugin links and supported versions, API docs and sandbox credentials

Explainers

What is MATCH

MATCH is a Mastercard file that acquirers check when a merchant has been terminated for cause. An entry limits access to new accounts for up to five years. It is not a public blacklist. It is an underwriting signal that prompts extra scrutiny.

What is a rolling reserve

A rolling reserve withholds a share of settlements, for example 5 to 10 percent, and releases it after a set period such as 90 or 180 days. Providers use reserves to buffer chargebacks and fraud losses during early months or in higher-risk verticals. The predictable version is one that has a written formula and a hard cap.

Methodology and limits

We analysed first posts from 227 public threads across three categories: Card, Crypto and Payment Processing, Offshore Bank and EMI Accounts, and Offshore Company. Text was classified by topic categories and by operational signals. We aggregated counts and anonymised individuals. No private areas were accessed. Forum users self-select and first posts may under-represent outcomes reached later in a thread. Findings should be read as directional patterns, not market-wide rates.

Conclusion

Approval is not the finish line. Staying funded is. The dataset shows that predictable cross-border processing depends on underwriting clarity, authentication that fits risk, and clear dispute workflows. Nigerian exporters that secure facts in writing, run a capped pilot, and invest early in dispute tooling reduce surprises and keep momentum.