Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

The coronavirus a.k.a. COVID-19 is a brand-new disease. Much like SARS (Severe Acute Respiratory Syndrome) and MERS (Middle East Respiratory Syndrome), COVID-19 is highly contagious when in close contact with infected animals or humans. The disease ostensibly began in the city of Wuhan, China in late 2019, at a seafood and poultry market. The virus is so named by dint of the crown-like formations on the surface of the particle. Viruses, like intracellular parasites cannot self-reproduce, and are not deemed living organisms. Nonetheless, COVID-19 infects host cells, multiplying exponentially, and ultimately wreaking havoc on their subjects.

[ad]

In February and March 2020, global markets reacted with shock and awe to the spread of the coronavirus. US markets like the Dow Jones, the NASDAQ, the S&P 500 and, the Russell 2000 – long-term bastions of financial strength following the global financial crisis of 2008 – reeled and writhed in agony as fears mounted. US markets relinquished all of their gains, back-pedalled from their historic highs, and retreated in the most unspectacular fashion imaginable. The US financial market, once a beacon for leading the global recovery left investors in tatters. With little warning, other than fear-mongering and bearish speculative sentiment, massive selloffs took place over consecutive days in March 2020. Investors have long been cautioning about the ‘correction’ in the financial markets, but nobody quite expected it to take the form of a virus that began in China.

How did a virus in China infect the global markets?

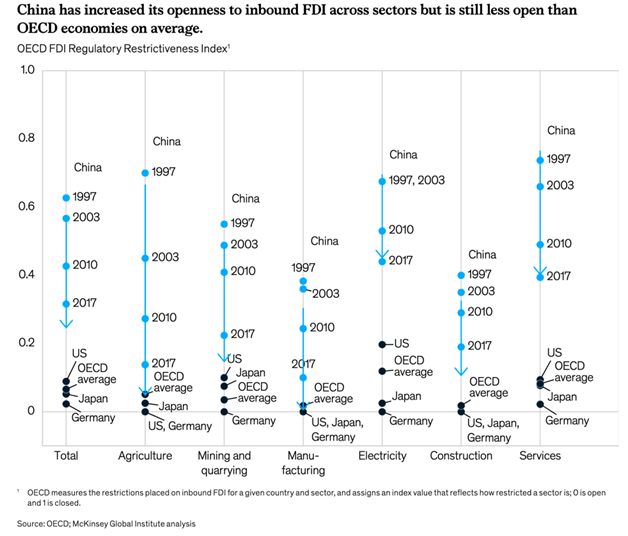

In a report commissioned by McKinsey Global Institute – China and the World – from July 2019, the role of China in the global economy was extensively studied. China is the world’s biggest economy in terms of PPP (purchasing power parity) and it is also the world’s largest trading nation of goods. An estimated 80% of all revenue generated by China’s 110 Global Fortune 500 companies is domestic in nature, with a limited international presence. With rising incomes across this populous nation, China has a thriving consumer market with an insatiable appetite for raw materials sourced globally. China is also a major exporter of goods and services, with many countries having high exposure to Chinese products. While China is opening up to increased foreign direct investments across the spectrum, it remains way behind other countries like the US, Japan, Germany, and OECD countries.

[ad]

Nonetheless, the size and scope of China’s economy is such that when China sneezes the world literally catches a cold.And that’s precisely what happened when the coronavirus outbreak in Wuhan, China generated ripples across Asia, Europe Africa, and the Americas. While estimates are sketchy, given the lack of transparency in reporting, identification, and collation of data, the statistics point to upwards of 100,000 cases, with 3353 deaths and more than 50% recovery. The mortality rate of the coronavirus (closed cases) indicates that 6% of people that didn’t recover died (3,353/57,477). That figure is certainly high enough and statistically significant enough to warrant global concern. The deaths spiked in February 2020, and are continuing their upward trajectory through March and beyond. The following confirmed cases by country/territory/conveyance have been reported:

- China 80,430+

- South Korea 6,088+

- Italy 3,858+

- Iran 3,513+

- Germany 543+

- France 377+

- Japan 361+

- Spain 259+

- USA 164+

*These figures were correct at the time of reporting on Thursday, March 5, 2020.

Given the rapid infection rate of the virus, the aforementioned figures provided for illustrative purposes only and updated figures can be found by clicking on this >>Coronavirus Spread<<, it is sensible to be concerned. Since China is ground zero for the coronavirus, any disruption to Chinese productivity has a knock-on effect for countries all over the world. When Chinese demand tapers off, or production is decreased, the global economy feels it in a big way. Despite efforts at containment, multiple cases of COVID-19 have surfaced all over the world.

[ad]

The most respected authorities including the Centers for Disease Control (CDC) sought to instill a sense of calm in the US and globally by promoting a commonsense approach to dealing with the virus – hand washing, covering your mouth and nose when sneezing, not touching your eyes, ears, mouth with your hands, staying home if you’re sick so that you don’t infect others.

What is Being Done to Bring Stability Back to the Markets?

It certainly comes as no surprise that when fear is driving speculative sentiment, markets will sell off in a big way. This type of trading news is a self-fulfilling prophecy of sorts, as even those who don’t wish to sell their equities are forced to face a grim reality: if you don’t sell now, the price of your equities will be less because everybody else is selling. And so, the sell-off begins in earnest. The market correction rebalances everybody’s financial portfolio because traders and investors seek alternatives to hedge against the volatility inherent in the financial markets.

[ad]

They do this by switching from highly volatile tech stocks, pharmaceutical stocks, industrials, and emerging market investments and purchase bonds, lower-risk funds, and gold among others. It should be stated in no uncertain terms that bear markets do not provide complete protection from pervasive negative sentiment, but there are many investment options that are relatively safer to hold during times of a financial crisis. These include fixed-interest-bearing investments such as Treasury notes, CDs, stable currencies like the Swiss franc and the Japanese yen (compared to emerging market currencies like the Indian rupee, South African Rand, Brazilian real, Chinese yuan, or Russian ruble) and so forth.

For markets to feel bullish again, traders need to start buying stocks. This begins when government steps in to allay the fears of market participants. This can be done in any number of ways such as press conferences from the White House, the CDC, European leaders, and other internationally respected government agencies globally. Naturally, news of a decline in the spread of the virus will be perceived positively and help to restore a semblance of normality back to the financial markets. Each of these measures can help to calm the financial markets, or at least to decelerate the velocity of selloffs. From a monetary policy perspective, there is much that can be done to shore up confidence in stock markets and the broader economy.

[ad]

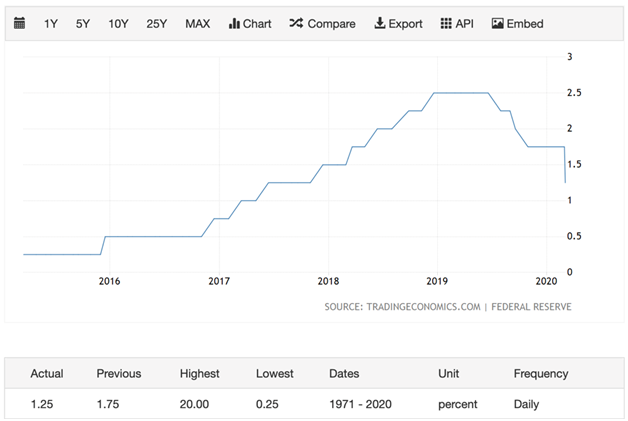

Can Interest Rate Cuts Boost Stock Market Performance?

Central bank governors and their Monetary Policy Committee (in the UK), or the Fed can convene to discuss ways of injecting liquidity back into the markets. This typically takes the form of a reduction in interest rates. There is talk of the Federal Reserve Bank moving to cut interest rates from the current level to inject increased liquidity back into the financial markets. The impact of reduced interest rates on economic activity is clear: it increases the demand for low-interest loans, spurring investment in real estate, increases in business activity, and an uptick in bank lending. This can have a positive effect on the economy in the sense that the cost of borrowing capital is less. This means that companies pay less on their loans as they are expanding business operations. This naturally translates into higher profits for the company if the economy warrants as much.

What happens next is up in the air. Nobody quite knows what to expect, but the hope is that containment will allow everyone to breathe a collective sigh of relief.

[ad]