Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

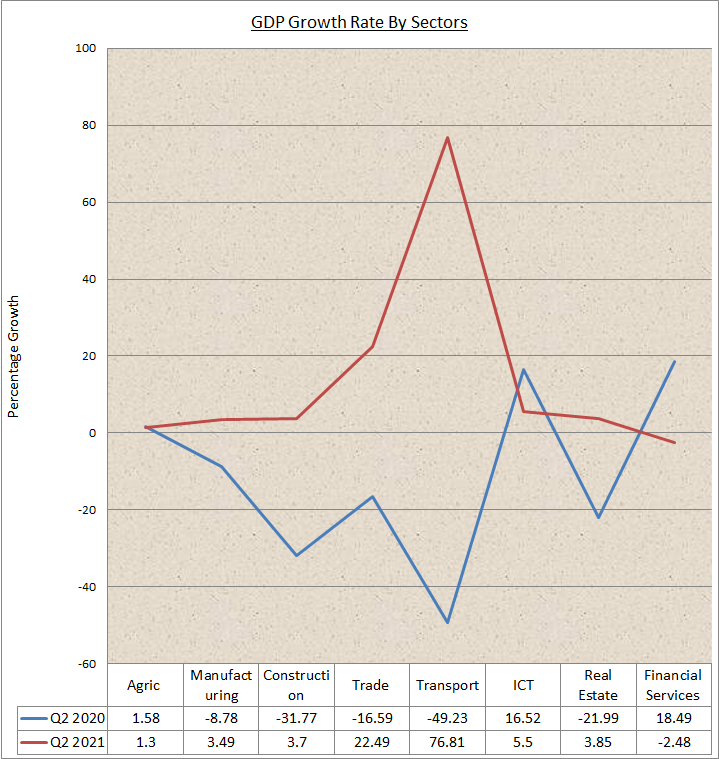

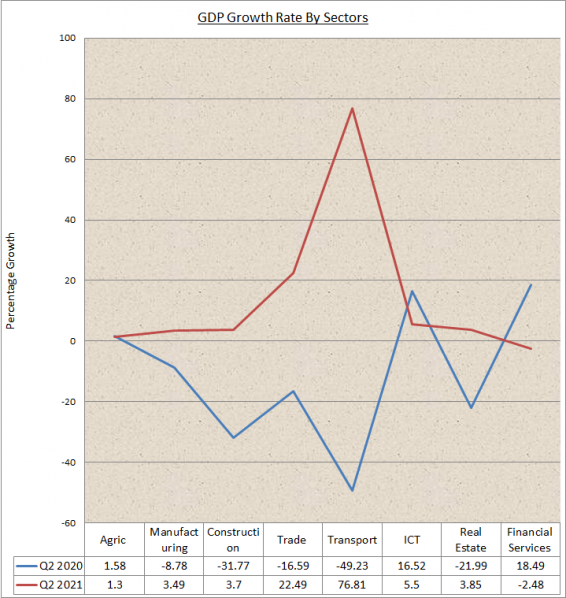

Nigeria, like any other economy, maybe climbing out of the deep hole. Nothing understates this better than the recent recovery in the transport sector, which saw a year-on-year (YoY) leap of 76.8 per cent in the last quarter (Q2 2021) as against -49 per cent growth it posted last year Q2.

The economy, across sectors, faltered last year for obvious reasons. There was a global shutdown to contain the spread of the COVID-19 pandemic, and as expected, the logistics sector, including transportation, took the first blow.

[ad]

And in the words of Prof. Samuel Odewumi, a member of the transport faculty of the Lagos State University (LASu), “a vibrant transport is the first sign of a recovering economy”. Like transport, like trade. From a deep dive in Q2 2020, activities in the sector saw double-digit growth last quarter.

Indeed, the gross domestic product (GDP) growth data for Q2 2021 released last week did break a six-year record. The 5.01 per cent YoY growth was roughly twice as high as any other quarterly performance since 2015 when President Muhammadu Buhari’s administration took over the national economy.

The leg-up performance came two quarters after the country exited one of the deepest but shortest recessions in its history. The economy caved in by as much -6.1 per cent in Q2 2020, which was followed by another -3.62 per cent in Q3 2020, leading ultimately to a recession, the second in the life of the current administration.

[ad]

But as predicted, the hollowing experience was short-lived as the country exited the recession narrowly in the last quarter (Q4 2020). There were debates as to whether the economy could bounce back immediately or go through a painful U-recovery, which could expose the country to the most dreaded depression.

It is in this context that the recent GDP data mean more than mere statistics to the market and policymakers. Except weighed against the base effect of the lull of Q2 2020 performance, which they are compared with, the flashy data could fool Nigerians and potentially downplay the fact that the country is only halfway out of the deep hole it was in throughout last year.

Of course, relevant ministries, departments and agencies (MDAs) have taken to different media platforms to celebrate the “impressive performance”. But it is relevant to interrogate the figures. Can the country replicate a similar performance in the near term? Do the figures represent real growth or the ongoing celebration is a classic case of broken window fallacy?

[ad]

A major reason the five per cent growth does not mean the economy is out of the woods comes from how percentage changes work when they oscillate between positive and negative regions. When an asset is priced at N100 million and it falls by 20 per cent, its new value is N80 million. If it regains 20 per cent, its new value is not N100 million but N96 million; the gain is N16 million. It thus means that the asset would need to grow by a higher percentage to erase the previous losses.

A worker whose salary was reduced by, say 10 per cent, during last year’s lockdown would also need more than a 10 per cent top-up on the new pay cheque to regain the original income value, supposing she has no other sources of livelihood.

In the same vein, when GDP falls by a certain percentage, it requires a higher percentage growth to return the economy to its previous size. By implication, Nigerian’s GDP merely reclaimed what it lost to COVID-19 last year’s Q2.

[ad]

In terms of absolute figures, the difference between the monetary value of the country’s total production during Q2 2020 when the economy was completely locked down and Q2 2021 when it had supposedly regained momentum was N0.86 billion or 5.4 per cent. The growth recorded in trade (which is not a high-capacity utilisation sector) alone added N0.51 billion (an equivalent of 60 per cent) to the expansion in the size of the GDP.

The sectoral performances, as contained in the Q2 data and other recent ones, underscore an economy that is not only bleeding but also deeply flawed by many contradictions. In continuation of the historical hollowing out, the manufacturing sector, though recorded positive growth in the last two quarters, is still tottering on the brink of collapse.

The sector moved from N1.4 trillion in Q2 2020 to N1.45 trillion in Q2 2021. Does the increase reflect the efforts put into growing the sector, including interventions and fiscal incentives, in the recent years? Perhaps, it does not appear to reflect the efforts the government put into reviving the sector, much less the latitude that naturally followed the re-opening.

[ad]

In the first two quarters of the year, the manufacturing sector got away with 3.4 and 3.49 per cent respectively. As good as the figures are, the sector’s performance is still in the negative region and below pre-COVID era. During Q2 2020, the sector lost 8.78 per cent with the following two quarters also recording negative growth, leading to annual growth of -2.75 per cent.

Agriculture, the fulcrum of the country’s attempt at reviving the productive sector, is among the few sectors that experienced positive growth during the pandemic. Of course, nothing short of that is expected of a sector that has received so much attention in terms of fiscal interventions and incentives at a huge cost to taxpayers. But the concern about the speed of growth of the sector persists. So much is expected of the sector not only because of the urgent need to flatten the food inflation curve, which stood at 21 per cent at the last survey, but also its weighted impact on the economy.

According to the last quarter’s growth statistics, the sector alone accounted for 23.8 per cent of the entire GDP. And that was not a flash in the pan, it reflected historical trends. If anything has changed, the Q2 performance even fell short of that of last year and the recent few years. Last year, the ratio of the sector to the entire economy was 26.2 per cent. That was about half of the entire service sector and five per cent higher than the contributions of industries.

[ad]

According to data by the World Bank, about 34.7 per cent of Nigeria’s workforce is engaged in agriculture, which accords it the highest degree of inclusiveness.

This also suggests that the growth of the sector matters more for the country’s desire to reduce its worrisome unemployment rate, which stood at 33.3 per cent at the close of last year.

There is no real-time employment data in Nigeria, hence it is difficult to know how the labour market has responded to the growth figures but most economists believe last year’s data might not have changed remarkably. And the GDP data are rough validation. Real estate and construction have a large multiplier effect on job creation. Sadly, the figures of these critical sectors are not as bright as expected of a fast-recovering economy.

[ad]

The growth of the construction sector has been in a wide swing. The real growth rate of the construction sector in Q2 2021 was 3.7 per cent YoY, a rise of 35.46 percentage points from the rate recorded the previous year. Relative to the preceding quarter, there was an increase of 2.27 percentage points. For the first half of the year, its growth was 2.4 per cent compared to -16 per cent in 2020. Regarding quarter-on-quarter (QoQ), the sector grew by -23.08 per cent in real terms, higher than the -24.77 per cent it recorded in the second quarter of 2020.

The incoherent growth does not bode well for a sector that is expected to support massive job creation, especially for the youths. And for a sector that is notorious for casualisation, this pattern of growth can hardly support staff retention and transfer of technical know-how, a challenge that could create a skill gap in the medium- to long term.

Real estate, a sector with huge employment potential as well, appears more progressive than construction. Yet, its growth does not match the huge housing deficit. Q2 2021 real GDP growth of the sector stood at 3.85 per cent, higher than the growth recorded in the second quarter of 2020 by 25.84 percentage points, and 2.08 percentage points higher relative to Q1 2021 In the first half of 2021, real estate services grew 2.79 per cent YoY in real terms, compared to -14.11 per cent recorded in 2020. In terms of QoQ, the sector grew by -0.72 per cent in Q2 2021.

[ad]

This sticky growth is challenging for the economy given the huge hole in the labour market. If job growth continues to slow, it will take the country several years to bring the economy back to its level of employment that can restore sanity in the society. Besides, faster employment growth means higher aggregate demand and, subsequently, more jobs.

Considering the current level of restiveness, poverty and security breakdown in different parts of the country, anything less than “V” job growth will escalate the already terrible situation. Youth unemployment is in the region of 45 per cent, which is worrisome.

But economists are even more scared that the rising hostility will be worse if they are not taken off the streets immediately. That does not suggest the sluggish job growth, which the phenomenal Q2 GDP figures will, at best, offer.

The recent GDP data mean more than mere statistics to the market and policymakers. However, when weighed against the base effect of the lull of Q2 2020 performance, which they are compared with, the flashy data could fool Nigerians and potentially downplay the fact that the country is only halfway out of the deep hole it was in throughout last year.

[ad]