Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

The signing into law of the bill for using movable assets as collateral, popularly known as Collateral Registry Act, precisely on May 30, 2017, was greeted with not only resounding applauds from the financial system stakeholders, but also described as a move in the right direction.

The law, which came on the realisation that small business, estimated to have employed over 60 million Nigerians and accounted for 48 per cent of the nation’s Gross Domestic Product (GDP) are stifled by funding, would from then, allow them borrow from banks with their movable items rather than fixed assets.

The objectives of the Secured Transactions and National Collateral Registry (ST/NCR) is to enhance financial inclusion in Nigeria, stimulate responsible lending to MSMEs, facilitate access to credit secured with movable assets, perfect security interests in movable assets, facilitate realisation of security interests in movable assets, and to establish a collateral registry and provide for its operations.

[ad]

The key deliverable of the Registry is to promote the acceptance of movable asset as collaterals for loans and contribute to economic growth and development of the country.

Former President and Chairman of Council of the Chartered Institute of Bankers of Nigeria (CIBN), Prof. Segun Ajibola, told The Guardian that the development reduced uncertainty, especially for banks that are wary of the level of risks associated with small businesses in less-than-encouraging business environment in the country.

The don, at a knowledge event organised by the institute’s subsidiary- CIBN Centre for Financial Studies with the theme: “Collateral Registry Act: Pros and Cons for the Banking Industry and Other Stakeholders,” reiterated that the Act was timely against the backdrop of different propositions on the potential it holds for Micro, Small and Medium Enterprises (MSMEs) and the economy.

The Financial Institutions Training Centre (FITC) also lauded the move to entrench the use of movable assets in financing, as opposed to fixed and huge collaterals that are not owned by the majority of those in need of capital.

But emphasising the need to get the initiative right, the Managing Director/Chief Executive Officer of FITC, Lucy Newman, said that as a next level of credit management, it would be nice if people can aspire to acquire properties and basic living items, as well as present a credit report individually, to have access to credit.

Less than two years after the enactment, about than 154,827 operators Micro Small and Medium Enterprises (MSMEs) have used their movable assets to obtain loans from financial institutions, under the National Collateral Registry (NCR), estimated at about N1.56 trillion.

Out of the number, 22,251 were female-owned MSMEs, with a total loan portfolio of about N43.62 billion. The rising number has been attributed to the high participation of smallholder farmers under the CBN Anchor Borrower’s Programme, using cross-guarantee as collateral.

The Central Bank of Nigeria (CBN), in pursuant of its mandate on sustainable economic and inclusive growth and financial inclusion, had collaborated with the International Finance Corporation (IFC) to establish NCR.

The NCR is a financial infrastructure that seeks to deepen credit delivery to MSMEs through enhanced acceptability of movable assets (equipment, machinery, vehicles, Keke-NAPEP, crops, livestock, account receivables, inventories, jewelries, among others, as collateral for loans by financial institutions.

It is a noticed based Registry where security interests in moveable assets are registered after being used as collateral to obtain facilities from financial institutions. It allows lenders to assess their priority interest in potential claims against particular collateral.

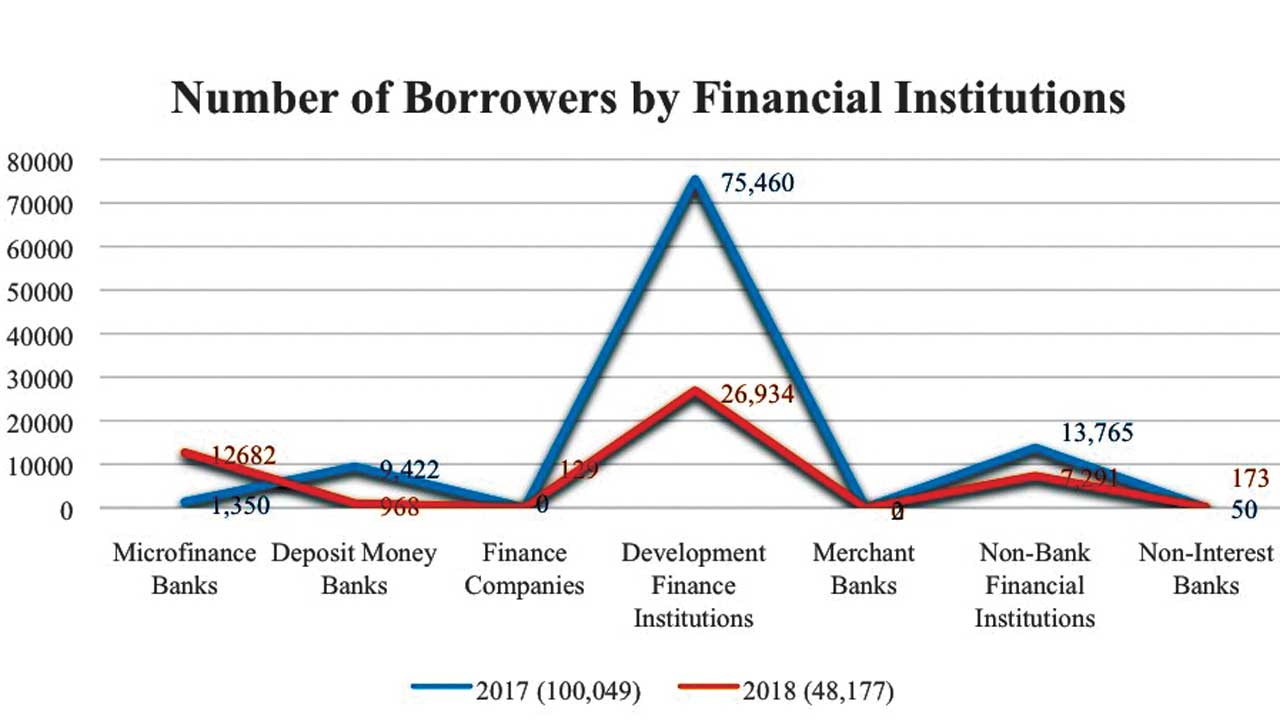

Already, the apex bank has affirmed the upsurge in lending, using movable assets as collateral, during the year under review, boosted by increase in the number of microfinance banks on the NCR portal, as well as increased participation of deposit money banks and non-bank financial institutions.

Already, the apex bank has affirmed the upsurge in lending, using movable assets as collateral, during the year under review, boosted by increase in the number of microfinance banks on the NCR portal, as well as increased participation of deposit money banks and non-bank financial institutions.

A cumulative of 16,349 searches was conducted by both financial institutions and the public on the NCR portal in 2018, due to increased participation in the movable asset lending regime and continuous sensitisation to the users to ensure they conduct searches to determine the level of encumbrances before undertaking any financial transaction.

In 2019, according to the apex bank, there would be conduct of specialised two to three days Workshop for Judicial Officers on the new secured transactions in movable assets regime in Nigeria, in partnership with the World Bank and National Judicial Institute.

There would also be increased sensitisation seminars for the legal community and the police; training of financial institutions on Asset Based Lending; formal launch of the registry; continuous sensitisation and capacity building of financial institutions.

It would also drive utilisation of collateral registry by at least 50 per cent of registered banks and other financial institutions; and integration of all other registries with NCR, like the Corporate Affairs Commission, and vehicle licensing, among others.

During the period under review, NCR Solution was able to move to the cloud, which enabled the website to be more stable, making productive performance by enhancing its accessibility by financial institutions and general public with ease. There was no downtime/network interruption recorded the whole of the year.

In the same period, 411 microfinance banks registered on NCR portal as a result of intensive sensitisation campaign on its operations carried out across the six geo-political zones of the country, as well as other collaborative strategic enlightenment programmes.

Also, the number of financial institutions that registered on the portal increased by 343 per cent when compared with the 2017 figure, which was 103 financial institutions. This was the result of the various aggressive education and awareness campaign on secured transactions in moveable assets conducted under the National Action Plan.

Still, the number of registered financial institutions that registered financing statements on the NCR portal increased by 89 per cent when compared with the 2017 figure, which was 36 financial institutions. This was the result of the various aggressive education and awareness campaign on secured transactions in moveable assets conducted under the National Action Plan.

[ad]

Last year, the office executed strategic engagements that were targeted at sensitising the participants on the legal implications of the Secured Transactions in Moveable Assets (STMA) Act, 2017; dynamics of secured transactions in movable assets; operations of the NCR portal, as well as to improvement of usage of the NCR portal by financial service providers.

So far, the challenge has been inadequate funding for sensitising the judiciary and Nigeria Police on the legal implications of the STMA Act, 2017. Of course, there is need for a driver to move NCR staff to strategic meetings and provide answer to financial institutions complaints where necessary, considering the present location of the office.

There is also need for additional staff, like a Senior Manager- training/public education and Assistant Manager- legal officer, to compliment the staff requirement for the registry.

Another observed challenge is the low usage of the Collateral Registry System, especially by banks and reluctance of financial service providers to appreciate the benefits of Asset-Based Lending.

[ad unit=2]