Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

As long as financial exclusion remains high, everyone loses.

To comprehend the magnitude of the challenge we face in our quest to reduce poverty in Nigeria, we need to first acknowledge government’s efforts so far.

You will recall the establishment of social investment programs (SIP) initiatives which were aimed at reducing poverty and improving livelihoods of vulnerable groups such as the unemployed youths, women, and children.

[ad]

The components of the SIP include:

- N-Power: a job creation scheme supporting graduates and non-graduates. The scheme seeks to enhance the employability of participants by providing stipends while non-graduates acquire vocational skills. Graduates, on the other hand, are trained to work in communities as school teachers, health support, and agriculture extension workers.

- Home Grown School Feeding (HGSF): a school feeding programme to enhance nutrition and learning of primary school children, markets for agriculture providers and jobs for food vendors in the community. Payments for agricultural produce and cooking services are made by the government.

iii. Conditional Cash Transfer (CCT): a poverty-reduction scheme providing cash transfers of N5,000 to one million very poor and vulnerable Nigerians on the national social registry (NSR).

- Government Enterprise and Empowerment Programme (GEEP): an interest-free credit scheme for micro and small enterprises that lack access to formal credit.

These SIP schemes involve the disbursement of cash to a broad base of Nigerians and aim to increase the throughput of payments as well as promote financial inclusion. Large transaction throughput/volumes are essential in the enhancement of the DFS ecosystem and government’s SIP initiatives offer such an avenue to increase DFS transactions volumes.

[ad]

Another fortunate development is that the Nigerian government was able to secure a $500 million loan from the World Bank towards the execution of this project. This throughput will facilitate monetary transaction flows between government and persons (G2P/P2G), government and business (G2B/B2G) and government and government (G2G).

Unfortunately, the SIP implementation has been hampered by extant financial system infrastructure constraints. In particular, these attempts by the government have exposed constraints in the areas of identity, reach (access) and cash-out (liquidity).

Let’s take the Conditional Cash Transfer (CCT) scheme, for example.

During its initial phase, the scheme covered 9 States with existing social registries. Potential beneficiaries in the national social registry were validated using the bank verification number (BVN) scheme. After validation, funds were paid through the Nigerian Interbank Settlement System (NIBBS) into bank accounts in participating banks. Since the scheme launched in 2016, three challenges – identity, reach and cash-out – have limited CCT scalability and the intended social and economic benefits.

Identity

Firstly, due to technical and operational constraints with the BVN system, only about 20 percent of the NSR beneficiaries have been validated.

The requisite process of validating the identities of intended CCT beneficiaries and account creation has not produced sufficient recipients of the CCT funds. The technical and operational constraints of the BVN scheme such as the use of proprietary technology and their ancillary costs, data quality and accuracy have all limited the establishment of enrolment centres to an already limited number of bank branches.

Reach

Secondly, the lack of proximity to, and availability of, financial service points (FSPs) — bank branches and/or agents which are meant to provide account opening and other customer service activities at the last mile – renders CCT funds which are domiciled in bank accounts inaccessible. In the case of account opening, only about 57 percent of beneficiaries with validated BVNs have successfully opened bank accounts.

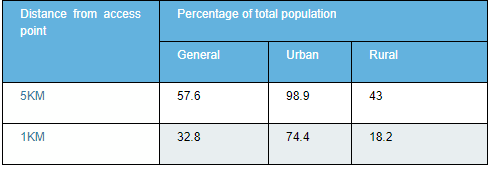

A 2015 study of financial service points (FSPs) in Nigeria revealed that there were less than 30,000 access points serving an adult population more than 90 million. The table below showing access point by distance further emphasises the plight of rural dwellers.

The proximity of access points presents a conundrum that impacts consumer utility, commercial sustainability of agents and ultimately financial inclusion. Resolving this challenge mandates the creation of additional access points and systematic mechanisms that facilitate commercial sustainability through even demand for agent services and increased transaction volumes.

Cash-Out

Thirdly, FSP liquidity for on-demand cash payouts (cash-out) cannot be met as and when due.

The conversion of digital payments to physical cash at agent locations is often limited by the proximity/access problem and manifests in user behaviours that warrant the immediate and complete withdrawal of funds received, leaving no residual funds in the account. This behaviour is not only detrimental to cashless tenets but also creates a surge in liquidity demand at peak periods that may be difficult to fulfill (thereby leading to service fee hikes and exploitation).

Unattended management of such service failures could potentially jeopardise trust and confidence in the financial services system.

In sum, addressing these pain points, which are mostly operational and exploratory, will ultimately improve financial inclusion and also address the scalability of the CCT and other SIP schemes. Without definitive knowledge of the implementation outcomes of the proposed initiatives, a regulatory approach that supports experimentation and testing is essential. Hence why we suggested the introduction of regulatory sandboxes for financial services in an earlier article.

Olayinka David-West and Ibukun Taiwo are members of the Sustainable and Inclusive Digital Financial Services Initiative at Lagos Business School

[ad unit=2]