Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

• Economists disagree as NBS figures beat IMF forecast

The National Bureau of Statistics’ (NBS) release of heart-warming growth numbers for the last quarter of 2019 yesterday has given further impetus to the discourse on gap between statistics and poverty alleviation.

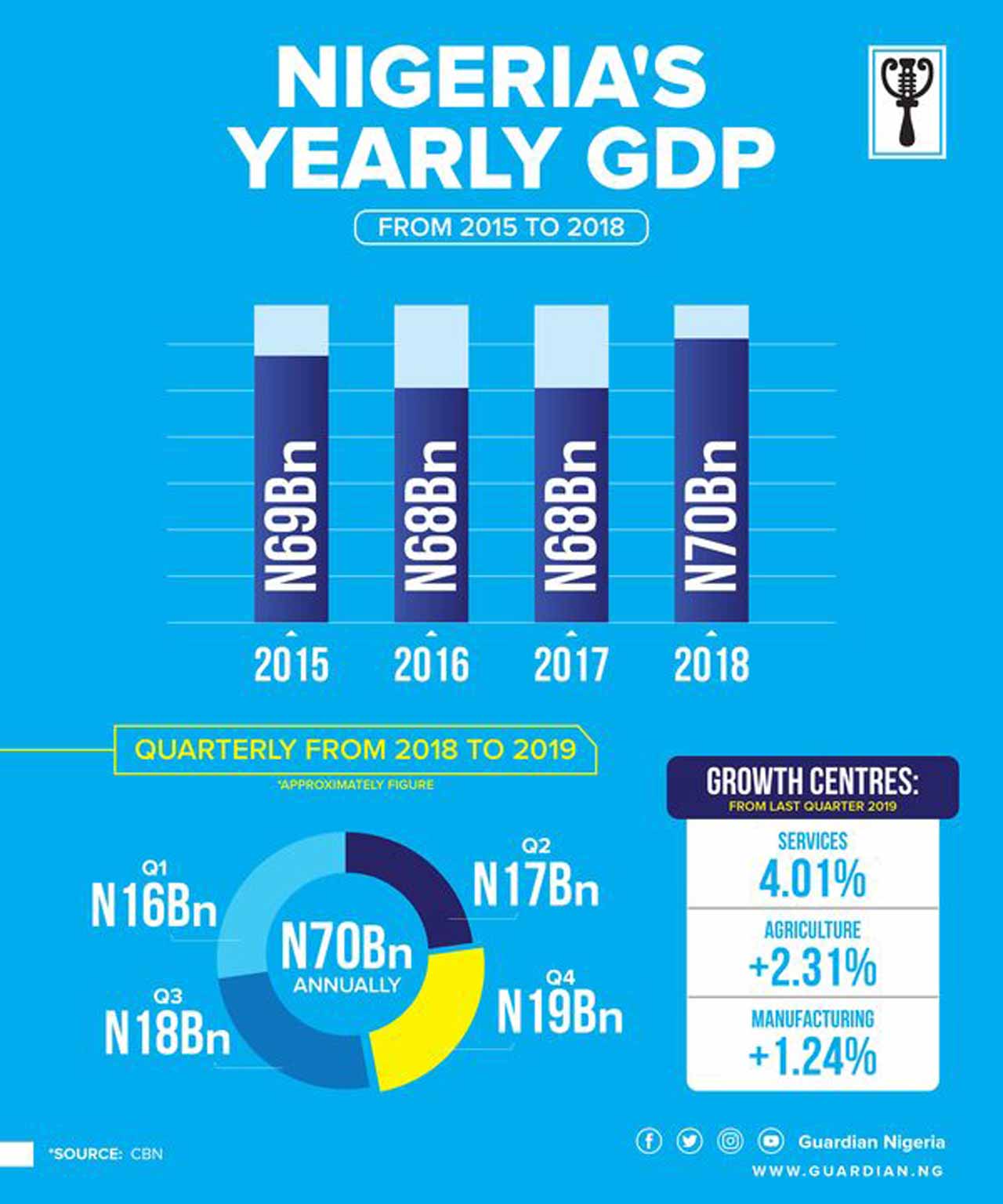

Official figures showed that Nigeria’s Gross Domestic Product (GDP) grew by as much as 2.55 percent (year-on-year) in the face of struggling real sector, receding trade outcomes, unabated poverty index and spiralling inflation. The economic growth, according to the NBS, represents the highest quarterly growth in four years (since third quarter of 2015). It was driven by sharper- than-expected growth in non-oil GDP. It beats the consensus forecasts of 2 percent, 2.36 percent and 2.20 percent by the International Monetary Fund (IMF), Cordros and Bloomberg respectively.

The IMF had, during its Article 4 Consultation on Nigeria, two weeks ago, cut its initial growth projection for Nigeria from 2.3 to 2 per cent, citing economic headwinds.

[ad]

For 2019 full year (FY), the economy, according to the NBS, expanded by 2.27 percent (year-on-year) as against 1.19% percent (year-on-year) in 2018 full year. The non-oil sector continued to show resilience, expanding by 2.26 percent year-on-year, as against 1.85 percent year-on-year in the third quarter of Q3-19), with faster growth recorded across all sub-components, except for Trade which remained in recession.

For clarity, the Services GDP (+4.01percent y/y) led the pack, followed by Agriculture (+2.31 percent) and Manufacturing +1.24 percent) sectors.

The oil sector also expanded, albeit at a slower pace of 6.36 percent y/y against the 6.49 percent y/y in Q3-19) on lower crude production (+4.71% y/y vs Q3-19: 5.15% y/y), with the NBS estimating production during the three-month period to be 2.00mb/d (vs. 2.03 mb/d in Q3-19).

The new growth figures however elicited mixed feelings from economists who expressed divergent views in their discussion of the matter with The Guardian. The debate mainly bordered on the usual disparity between statistics and actual improvement in living standards, especially as previous independent global agencies had harped on Nigeria’s deplorable poverty rate. The Multidimensional Poverty Peer Network (MPPN), in its 2018 National Multidimensional Poverty Index for Nigeria posited that the share of the country’s multidimensionally poor people at the national level was more than 54 percent with the average intensity of deprivation of standing at 42 percent. The indicators with the largest weighted contribution to poverty in the country were employment, years of schooling and school attendance.

[ad]

In the same vein, World Poverty Clock’s report in 2018 pointed at Nigeria as having the highest rate of extreme poverty globally. The report claimed that Nigeria had overtaken India as the country with the most extreme poverty in the world. India has a population seven times larger than Nigeria’s.

“Anyone who has been following my projections since last year would have observed that I have been consistent on the theme that the economy is adjusting to a new growth level beyond what many forecasts claim,” Economic Analyst with the Lagos Business School, Dr Bongo Adi told The Guardian.

He said his strong optimism was built on the most important leading indicator for real GDP growth, which is the Purchasing Managers’ Index. “Most analysts tend to ignore this in Nigeria. Without claiming any causation, if you regress GDP growth on PMI, you would obtain a strongly positive relationship.” The PMI, Adi said has been consistently above 50 for the past two years post-recession and reaching the highs of the 60s some months. What the long haul of positive PMI translates to is the gradual build-up of economic momentum which has just started to manifest.

“Of course, this obtains in the backdrop of low performance in some sectors. But on aggregate the momentum exerts a stronger boost. We begin to see this manifest in the real estate sector which has continued to garner strength. Recall that the real estate is the first to go into recession and the last to come out. This happened in the 1st quarter of 2019 and that growth spurt has persisted. The growth of the real estate and strong PMI are indicative of an economy on the rebound.”

[ad]

Dr Adi also made reference to what he described as the unconventional CBN policy regime, which he said was a “madness” that had a “method. We have seen some unorthodox policy dictatorship from the apex bank in recent past. As a result, incentive has shifted from investing in paper assets to capital market investing. Credit to the private sector has also turned a corner. With lending rates crashing, we see heightened activity in the real sectors even though infrastructure bottlenecks undermine it. The minimum wage and new tax policies have a net bouyant effect on the economy in the medium to long term.”

He argued that the recent trade policy enactments might be salutary for economic growth because the bulk of Nigeria’s trade is just a depletion of our current account. Most trade is import trade which is positive net capital outflow whose restriction reduces the negativity in the current account. The country currently has a liquidity issue in its economy with the CBN-initiated controls. With an artificially imposed low interest rate, Treasury Bills are low; Open Market Operations (OMO) is out of bounds for private citizens . Excess money in the hands of people is seeking for outlet, according to Adi. The resultant food inflationary trend pushes up headline inflation rather than core inflation. He argued that high food inflation is driven by the border controls plus increasing cost of production occasioned by infrastructural rigidities. The analyst, therefore, recommended retention of the current monetary policy regime.

Executive Director of the African Centre for Shared Development Capacity Building, Ibadan , who is former Director-General of the Nigerian Institute of Social and Economic Research ( NISER), Prof. Olu Ajakaiye said the new growth figure “is “impressive” but has an outcome that is “very depressing.”

“ The growth is still driven by oil and agric sectors. The lower growth rate of manufacturing is worrisome despite the efforts of CBN and government to support the sector. A study of the conditions and expectations of the manufacturing sector will be useful to provide a basis for additional policies to support the sector,” Ajakaiye said.

[ad]

“The negative growth rate of electricity sector also deserve attention of government. Clearly the reforms in the sector need to be re-examined and necessary changes quickly considered. The performance crop agric could have been much better but for the security and rural transport challenges. Efforts should be intensified in resolving these challenges,” he said.

He advised that a study should be commissioned jointly by the NISER and the CBN to find out the reason the sector was under- performing in spite of the many initiatives by both the fiscal and the monetary authorities. Also disturbing, according to the economist, are activities in the livestock sector which he described as very infinitesimal in the agricultural sector but were constituting a very big drawback in the overall agricultural sector through the farmers/ herders confrontations.

Prof. Godwin Owon the Executive Chairman of Society for Analytical Economics and former Special Adviser to Prof. Chukwuma Soludo at the CBN described the GDP figures as a formality done by the NBS but lacking in facts and principles. He insisted that the result did not reflect the reality and lacked basis. He asked: “How can you arrive at GDP of a nation without first establishing the GDPs of the states from where you can then disaggregate ? How can you have these outcomes when it is known that 2/3 of the country is at war and no serious productive activities are going on? The remaining 1/3 of them are having a feel of the dislocation in the 2/3 States. You cannot be talking of GDP in the air. They should stop this falsehood.”Prof. Owoh declared that the NBS has refused to subject its exercises to fiscal and macroeconomic audits which will involve macro economists subjecting its scenarios to further test to confirm the outcomes.

[ad]

Reacting to the GDP figures, Chief Executive Officer of the Nigerian Stock Exchange (NSE), Oscar Onyema said that, for Nigeria to enjoy real per capita income growth, the economy must grow at between eight and 10 per cent; with single-digit inflation rates going forward.

“I must balance the IMF’s comments with Nigeria’s GDP numbers that were released by the National Bureau of Statistics reporting a Q4 2019 GDP growth performance of 2.55 per cent, which is the highest quarterly growth since the recession in 2016 and culminating in a full year 2019 growth rate of 2.27 performance.

“Putting this side by side our annual population growth rate of about 3 per cent, the message still remains that we have our work cut out for us as a nation and the economy must grow at over eight per cent – 10 per cent; and control inflation to single digit rates, if we must enjoy robust real per capita income growth.”

He, however admitted that government’s fiscal and monetary reforms over the past two months have shown some intent at tackling the nation’s challenges.

He said: “This is not a short-term task but a long-term one, and we look forward to the sequel to the Economic Recovery and Growth Plan (ERGP) to address this existential economic threat of a sustained slow growth.

“Government’s fiscal and monetary reforms over the past two months have shown some intent at tackling the nation’s challenges. In particular, we note the clauses in the Finance Act 2019 and how they better recognise the income generating status of micro, small and medium scale enterprises thereby taxing them appropriately.”

[ad]