Follow Us on Google News

Follow Us on Google News Follow Us on Google Discover

Follow Us on Google Discover

Telecom operators in Nigeria and other parts of Africa have continued to witness declining average revenue per user (ARPU) amid flat operating costs and reducing margins.

PwC, in a new report, said telcos have seen their ARPU eroded in recent years, reflecting the commoditisation of core services (voice, SMS, basic data) and competitive pricing pressures.

ARPU is a non-GAAP metric commonly used by digital media, social media, and telecommunications companies to assess their revenue-generating capabilities at the per-customer level.

The report, titled, ‘Study on the level of competition in voice and data market segment of the Nigerian telecom industry’, presented at the Nigerian Communications Commission (NCC) organised stakeholder workshop in Lagos, noted that sub-Saharan African (SSA) telcos grew their subscriber bases but ARPU has declined since 2020 due to factors like economic inflation, low consumer incomes and intense competition.

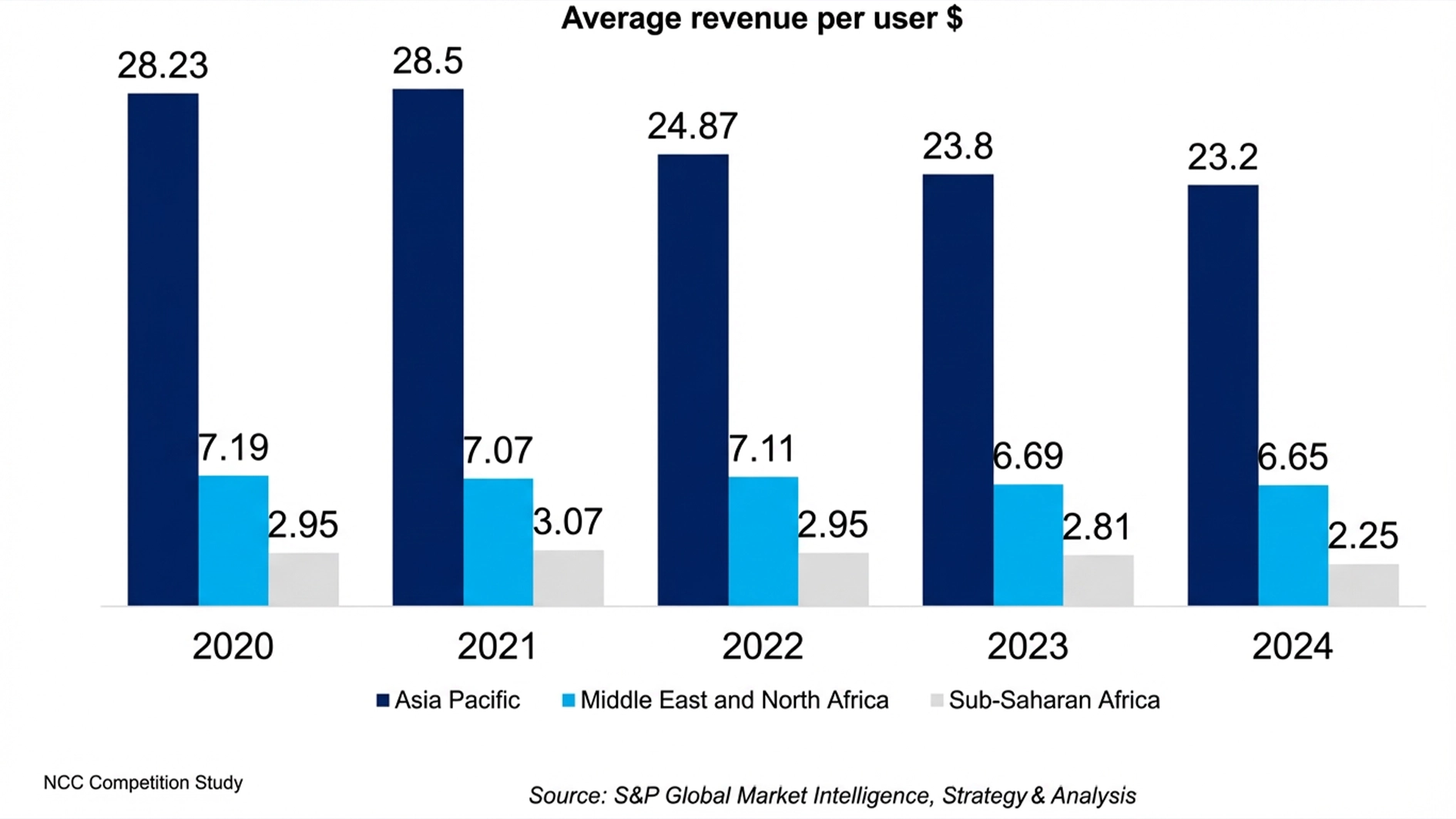

Specifically, in 2020, Asia Pacific saw 28.23 per cent growth in ARPU, the Middle East and North Africa (MENA), 7.19 per cent and SSA, 2.95 per cent. In 2021, Asia Pacific witnessed 28.5 per cent, MENA, 7.07 per cent and SSA, 3.07 per cent.

In 2022, Asia Pacific saw 24.87 per cent; MENA, 7.11 per cent, and SSA, 2.95 per cent. In 2023, Asia Pacific still saw 23.8 per cent; MENA, 6.69 per cent and SSA, 2.81 per cent, and for 2024, Asia Pacific maintained dominance with 23.2 per cent; MENA, 6.65 per cent,l and SSA, 2.25 per cent, respectively.

According to the report, global telecom revenue is projected to grow slowly by 2.9 per cent CAGR through 2028, falling behind inflation to a modest $1.31 billion in 2028

PwC noted that this growth rate falls short of global inflation expectations, which are forecast to average between 3.7 per cent and 5.8 per cent yearly over the same period.

“The industry’s core offerings (fixed and mobile connectivity) are increasingly commoditised, limiting pricing power and squeezing margins,” it stated.

According to it, consumers want digital customer journeys like self-service apps, eKYC onboarding and chatbots instead of physical service centres.

It said App-based account management and e-top up dominate, reducing reliance on paper cards & call centres.

PwC further observed that with the rise of content creation, and younger entertainment and social media generations (millennials, genZ, genX), data equates with social access e.g TikTok, WhatsApp, streaming platforms, among others.

“Telcos must design entertainment first bundles and partner with OTTs to stay relevant,” it stated.

According to the report, users now increasingly want TelCo plus lifestyle services such as utilities, fintech, health (telemedicine platforms), and content.

It noted that success for telcos depends on who can integrate lifestyle services seamlessly into their offerings.

As a result, PwC observed that telcos are rolling out third-party subscriptions to bundle services and improve customer retention in a saturated market. It said telcos are keen to upsell to their subscribers, not only to boost ARPU, but to protect their core data service subscription.

According to it, telcos account for 77 per cent share of streaming partnerships worldwide, highlighting the strategy to drive subscriptions through integrated data and content packages.

It disclosed that as of 2024, 20 per cent of the global streaming market is distributed by telcos through bundling.

The report said 5G adoption is accelerating, albeit slower than expected, and is forecasted to account for 64 per cent of mobile subscriptions by 2028. It said 5G is set to become the dominant mobile standard globally by 2026, with subscriptions rising to 7.51 billion in 2028.

According to PwC, by 2028, 5G will account for 64.1 per cent of all mobile subscriptions, saying Fixed Wireless Access (FWA) is a key 5G use case, especially in underserved urban-to-rural areas.