Last week, the presidency announced that some Indian investors have made significant investment pledges during the just concluded Nigeria-India Presidential Roundtable and Conference held on the sidelines of the G-20 Summit that took place in New Delhi, India. While stakeholders have applauded this move, they have also called on the government to improve the operating environment for local and existing manufacturers before going after foreign investors, TOBI AWODIPE reports.

The Presidency, through the Special Adviser on Media and Publicity, Ajuri Ngelale, said $14 billion was pledged by Indian investors to the local economy. Indorama Petrochemical Limited pledged $8 billion to the expansion of its fertiliser production and petrochemical facility in Rivers State, Jindal Steel and Power Limited pledged $3 billion while SkipperSeil Limited also pledged $1.6 billion to establish 20,100MW power generation plants across several states in Northern Nigeria.

President Bola Tinubu, he said, also approved the finalisation of a new $1 billion agreement to bring the Defense Industries Corporation of Nigeria to 40 per cent self-sufficiency in local manufacturing and production of defence equipment in-country by 2027, through a comprehensive new partnership with the Managing Arm of the Military-Industrial Complex of the Indian Government.

Another pledge from Bharti Enterprises to the tune of $700 million took the total amount to almost $14 billion with the President saying they must all translate to industries and jobs.

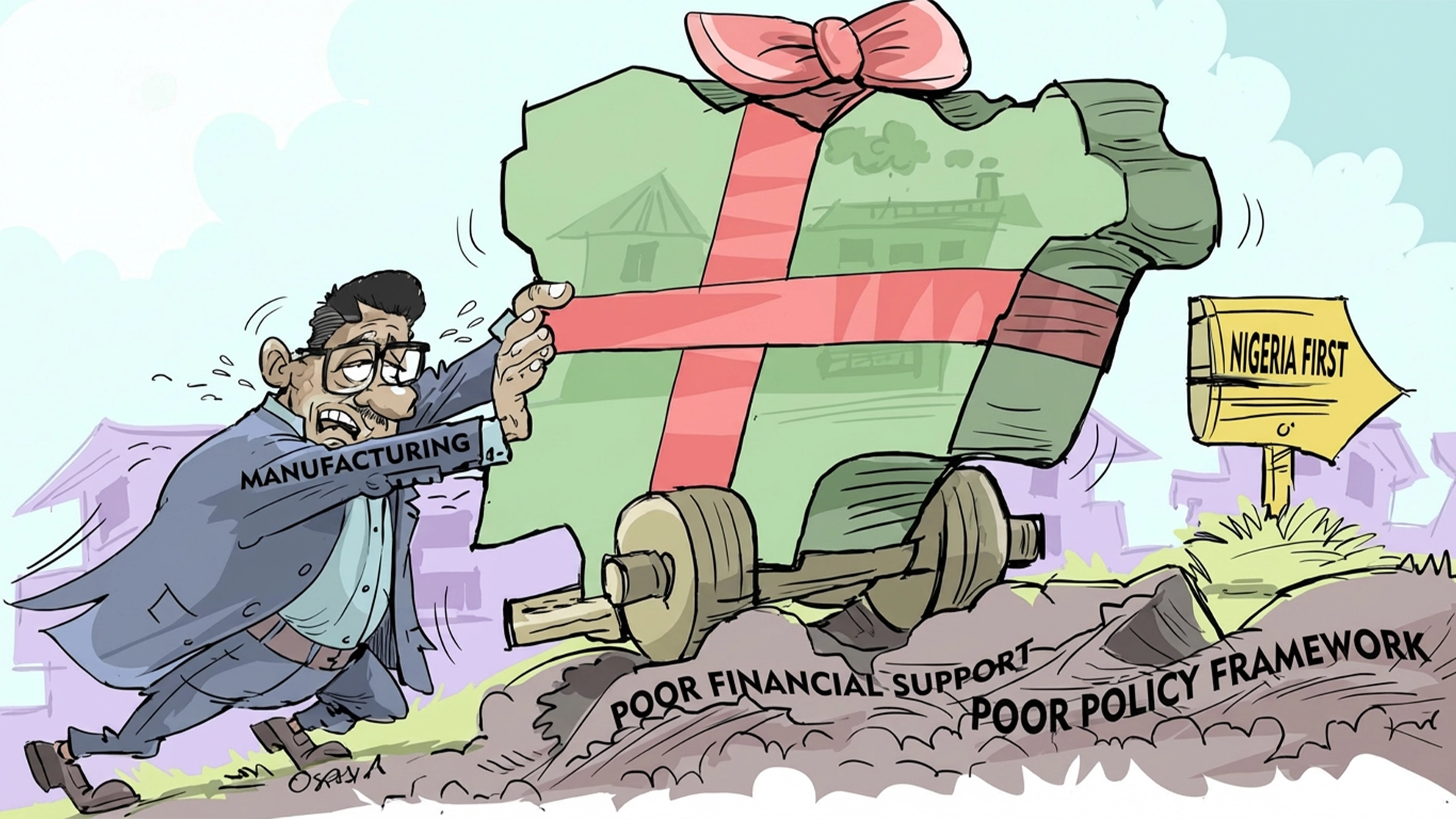

No definite timeline has been given on when the pledges would be redeemed or when the industries would take off, a situation the Director, Centre for the Promotion of Private Enterprise (CPPE), Muda Yusuf, said is a reason the pledges should not be celebrated yet.

“It is one thing to pledge, it is another thing entirely to commit resources and get things running but we must remain optimistic. This is a good thing as what our economy needs the most right now is investments, be it domestic or foreign.

“Foreign investment is great because it brings in foreign exchange which helps our FX liquidity but how soon this will materialise remains to be seen. But it is a step in the right direction.”

He noted that the investors would do due diligence and country risk assessment so the Federal Government must ensure there are no impediments and maintain high levels of investors’ confidence so that other investors would come in as well. He urged local industry players and stakeholders not to celebrate until the investors come in and start operations.

“The investments will benefit Nigeria if there is an additional inflow of capital because it is about the movement of capital between both countries. We need to minimise risks for them as well because if they do their findings and they see that the risks are too high, investors would pull out. India is a big name in manufacturing, pharmaceuticals, trade, industry and many other areas and having them come in would be of huge benefit if structured well,” he stated.

Yusuf noted that while foreign investment is good, it is also as important as domestic investment and urged the Federal Government to pay urgent attention to both so that the latter does not suffer.

Yusuf urged the Federal Government not to over-concentrate on foreign investors and forget the local ones, who he said have been keeping the economy going, facing the heat, dealing with a worsening operating environment and other factors.

“Our domestic investors are creating 90 per cent of jobs we have in Nigeria currently and paying 90 per cent of the taxes the government is using; be it the multi-nationals, big manufacturers, medium to small scale entrepreneurs or even the informal sector, which is often overlooked but over-taxed.

“We often tend to focus on foreign investments, forgetting about domestic investors, who are very critical to the survival of our economy. They also deserve attention and care they deserve to be engaged with and given reassurances just as the Indian investors were reassured. If our local industries and manufacturing sector are allowed to die, what will foreign investors come to meet?” he asked.

Immediate past chairperson, the Manufacturers Association of Nigeria (MAN), Apapa branch, Frank Ike Onyebu, expressed excitement at the prospect of attracting foreign investment coming into the country, adding that it is good for the economy whenever FDIs are secured.

He, however, went on to add that it is not enough to simply make such announcements, but that the government must follow with measures and a good operating environment to ensure they become a reality.

“Any investor coming in will make findings and do an in-depth analysis of how they are going to make money and get returns on investments as well as risks to said investment. Anyone can sign a MoU or make pledges and it wouldn’t translate to anything. We must improve our operating environment for manufacturers because I don’t know if the government is aware but many companies currently operating in Nigeria are trying to get out.

“Insecurity, high cost of doing business, skyrocketing inflation and many other factors are killing businesses here and many operators are looking for a way out. We must get it right at home first before inviting foreigners to come in,” he stated.

Onyebu lamented that power has been a major challenge for businesses and industries in the Amuwo-Odofin Industrial Estate Scheme, worrying that any investor who experiences the situation would take to his heels.

“I have been running totally on the generator for the last few days as the power supply company says there is a fault it has not been able to locate yet. We have to ‘tip’ them to come to fix it because that is still cheaper compared to burning diesel. If I can find another country to do business with less problems, I will go there immediately.”

He lamented that if foreign investors do their homework well, they will be shocked at the level of hardship manufacturers face daily in the country.

“Instead of getting steady power, we get nothing and have to constantly tip the officials to give us the little we used to get. What did they do instead? They ran to the government to approve tariff increases to shore up their revenue. Which foreign investor will see all these and want to stay?” he queried.

He regretted that despite several complaints made to the government, the industrial area remained in a state of neglect with a non-existent road network.

“I have lost a lot of money and customers because of the bad roads in this axis. Go around the whole of this industrial estate and show me a good road network. We pay through our noses before some containers agree to come here; what investor would see this and want to put money here? We have been struggling with FX for years and it has affected many operators with some being forced to close.”

He added that he was hopeful the agreements materialise as it would be a boost for everyone but urged the government to look into local manufacturers’ and industrialists’ complaints to prevent them from pulling out as others had done recently. “It is our hope and desire that more investors come into the country because, truthfully, Nigeria suffers from under-investment and under-utilization. We need more factories to come on board, we need to create massive employment quickly for our people but more importantly, we need a safe, stable environment that will facilitate the production of cheap, affordable goods for local consumption and export.”