This month, Nigeria’s external reserves climbed to levels not seen in years. But while reserves provide a useful buffer, they do not, on their own, cure poor governance disguised as fiscal imbalance — a risk that is not technically synonymous with bankruptcy but amounts to a slow erosion of the country’s fiscal sovereignty. As the country’s fragile financial situation forces the government to trudge on under severe fiscal constraints, GEOFF IYATSE reports that a fall in oil prices, a sudden cessation in portfolio inflows, or a spike in global rates could expose the country’s weak financial underbelly in weeks.

From the Caribbean to Asia and across Europe, as well as Sub-Saharan Africa, modern economies are replete with bankruptcy crises. At least since the turn of the century, the global community has witnessed more bankruptcies than economic milestones and breakthroughs.

For one, Argentina declared bankruptcy in 2001 with a debt of $145 billion as massive corruption ruined its stability and scuttled its debt management policy implementation.

In 2008, it was Iceland that was caught in an $85 billion debt dilemma amidst a global credit crunch. Amidst the COVID-19 crisis in 2020, the world’s development institutions put up rare rescue efforts to save vulnerable countries, especially in Africa, which were teetering on the fiscal edge. But that did not cure national economies of the bankruptcy scourge.

Lebanon, despite its panicky and desperate efforts, including a WhatsApp user ‘tax,’ could not prevent defaulting on its debt obligations estimated at $90 billion in 2020 as the global community struggled to stave off the systemic risk of the pandemic.

Most recently, Sri Lanka, a small country mired in elite bargaining, joined the long list of countries that would taste national embarrassment. And it also came knocking at the West African door a few years ago when Ghana defaulted on a $3 billion debt payment.

Like a stroke, bankruptcy does not start the day it is announced. A familiar path manifests in rising domestic yields, crowding out of the private sector, depletion of reserves, and finally, restructuring, then default.

Zambia and Kenya have both had a taste of this in recent years, to the glee of Nigerians and others. But Nigeria, which escaped the crisis by the whiskers, is copying the playbook of bankrupt countries step-by-step and layer-by-layer.

As Abuja celebrates moderate nominal growth in revenue, many leading economists are also carried away by the growth and choose to take their eyes off the details in the government’s books that could ruin its future survival.

Public financing framework is everything, but fiscal consolidation, the only remedy, leading to a funding crisis that is turbo-charged by unsustainable cost of debt service, choking fiscal deficits, sustained stop-gap borrowings, bloated contingent liabilities, escalating politically-charged expenditures and most importantly, extremely volatile revenues.

Whether it is in the global North or South, where corruption, official waste and cronyism are synonymous with political leadership, bankruptcy thrives on fiscal indiscipline and governance failure, failure to manage the trade-offs between short-term comfort and long-term gains in a manner that aligns with the normative consensus of the affected countries and the common good.

Fortunately, Nigeria, with all its failings, has been spared the bug, a vice fuelled by moral disaster more than it is about economic misfortune. But sadly, there have been concerns about the country’s fiscal sustainability, a forerunner of insolvency. The question about Nigeria’s fiscal sustainability is decades old.

In recent times, from President Goodluck Jonathan through the late Muhammadu Buhari to the current one, administration after administration has found a smarter, but not necessarily a wiser response to the probing of the civil society.

Narrowing fiscal margins

WITH the fiscal margins narrowing to a frightening level, debt rising faster than revenues, politically-charged recurrent expenditures swelling daily just as budget execution capacity dangerously weakened, the question as to whether Nigeria can survive its self-inflicted fiscal trouble is more relevant now than any other time in the country’s history.

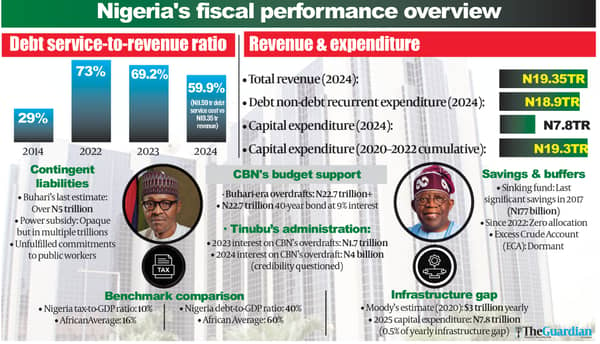

Last year alone, the Federal Government spent N11.59 trillion on debt servicing. The amount is huge for a country that is burdened by a gaping hole in infrastructure spending, estimated at $3 billion yearly.

Agreed, the government has increased its revenue profile with its retained earnings only about N650 billion short of N20 trillion last year. At N19.35 trillion in total earned revenue, the debt service to revenue ratio stood at 59.9 per cent (approximately 60 per cent). It was a decent deceleration from the 69.2 per cent recorded in 2023, when the total revenue was N12.5 trillion. It was also far less than the 73 per cent inherited by President Bola Tinubu (carried over from 2022).

Of course, a short-term trend analysis points to a downward-sloping debt service to revenue ratio. But long-term data paint a different picture entirely.

For instance, a decade earlier than last year, the Federal Government’s total debt service cost was N942 billion or 29 per cent of the government’s composite revenue, which stood at N3.42 trillion. But the real crisis that almost tipped the country off the fiscal cliff started in the intervening years when interest payment started taking nine or more from every 10 kobo that the Federal Government earned – an era that could be best described as fiscal horror.

Of course, there has been remarkable improvement – but to the extent that anybody could see. Perhaps, there is something that meets the eye in the current debt management disclosure framework. In 2023, the government said it spent N1.7 trillion to service its debt obligation to the Central Bank of Nigeria (CBN) through sundry overdrafts estimated at over N30 trillion at the close of Buhari’s administration.

In the twilight of the Buhari administration, the N22.7 trillion, in the first instance, was restructured into a 40-year bond in an agreement that was to cost the government a nine per cent interest rate compared to MPR plus 300 basis points that the government was paying before the securitisation.

The Debt Management Office (DMO), like the Federal Government, as well as the CBN, has kept a sealed lip over the current status of the controversial ways and means (W&M) facilities.

In a letter to the National Assembly requesting approval for the 2022 supplementary budget, Buhari said the bond that was to be issued to the CBN was negotiated at nine per cent. If the securitisation agreement is still valid, the FG should be servicing the accumulated budget support overdraft at nine per cent, which translates to over N2 trillion. This, added to other components of the debt burden, means the government would effectively spend about N13 trillion on interest rate payments last year.

But how the FG currently relates with the CBN, an institution it owns 100 per cent of, though, is one of the many grey areas in the fiscal status of President Tinubu’s administration.

Perhaps the government secured some forbearance from the apex bank, or the latter has written off the debt owned by its shareholder. As per the debt, no information is certain except that it adds up in the making of the era of selective information disclosure.

Curiously, available documents put the cost of servicing the CBN’s facilities in 2024 at a meagre N4 billion, raising questions about the credibility of the reports themselves and the extent of disclosure on the financial health of the government. Midway into Buhari’s two-term administration, when W&M’s financing window became awkward, there were allegations of multiple abuses against the government and the lender, the CBN. There were also different versions of information on the true statement of account of the debt. The current administration has been selective about what to disclose and the information that requires gagging on its overdrafts to the FG.

At the onset of the current administration, the Minister of Finance, Wale Edun, whose office oversees the government balance sheet, said the government had launched an investigation to “determine the true amount” accessed through the credit line.

The minister and the CBN Governor, Yemi Cardoso, also told Nigerians that the window had been shut down, recreating the usual old assurance until the lid is taken off. What both other key officials of the current administration have carefully avoided is the status of the bond issued to the CBN, which would not be fully liquidated until the next 38 years.

The FG was granted a three-year moratorium on principal, with interest payment expected to commence immediately. Both interest and principal, according to the government financial stewardship, may have been put on hold.

The fuss over high debt financing

AT the close of Q1 2025, national public debt ballooned to N150 trillion or 40.3 per cent of the country’s rebased gross domestic product (GDP). The debt-to-output level is significantly low compared to the global average, which has risen to 235 per cent, according to the International Monetary Fund’s (IMF) “Global Debt Database” report.

Some analysts suggest that the relatively low debt-to-output ratio has expanded the fiscal headroom. Unfortunately, the major drivers of the GDP – agriculture, especially, bring nothing to the revenue basket. Rather, it is a cost centre to the government. Industry, which controls a substantial portion of the GDP (about 10 per cent in the past decade), remains at an infant stage and contributes a little to public revenue. The mainstay of the economy, as it contributed a little above four per cent to the GDP as of the second quarter, raises questions on the relevance of the GDP size to debt sustainability disclosure.

But there is also more to debt concern than its size. First, at 60 per cent of the total revenue of the government, the cost of debt payment is crippling, with an unsettling, decaying effect on the infrastructure stock. More importantly, with the DMO issuing bonds monthly against zero savings for debt liquidation, the country may already be trapped in a debt cycle. Sinking fund is a strategic and integral part of the FG’s debt management culture, at least since the beginning of the current democratic sojourn, and was regularly funded in the days of President Olusegun Obasanjo.

But that was in the distant past. In the past 15 years, it has been added to the long list of non-priority fiscal items, just like the Excess Crude Account (ECA) buffer. The last time something close to significance was saved in the sinking fund account was 2017, when it received N177 billion. From 2022, the account has received zero savings – a red flag on the government’s ability to liquidate maturing debts.

Backed by the full faith of Nigerian sovereignty, the FG can only refinance its existing loans with fresh instruments without any repercussions except the risk of being mired in a debt cycle and burdening its posterity in endless debt.

From Africa to Europe and Asia, debt recycling, which is synonymous with building a pyramid of cards, is among the first steps in the journey to insolvency, whether of a sovereign entity or corporate organisation.

But does this mean every entity that recycles debt eventually goes insolvent? Many escape the repercussions by a hair’s breadth. Most will continue to toil with reckless debt indulgence and remain afloat for as long as the global debt market remains liquid and they are considered creditworthy. It means that Nigeria faces two risks.

One, the erosion of confidence in its ability to fulfill its obligation (something more severe than the 2021/2022 “blockade”) could pull the string of bankruptcy. It could also be caught in a systemic risk of the level of the COVID-19 pandemic that dries up the debt market overnight and leaves no sufficient room for refinancing.

The so-called “slow journey” to bankruptcy could accelerate overnight. A fall in oil prices, a sudden stop in portfolio inflows, or a spike in global rates could expose Nigeria’s fragility in weeks. Domestic unrest – fuelled by inflation and unmet promises – could force unsustainable subsidies back on the books. Each of these scenarios is plausible, and together, they make complacency extremely reckless.

Heated fiscal tension with its decay effects

THE Debt-to-GDP has climbed above 60 per cent (N11.6 trillion in absolute terms) — a threshold that, while lower than some other African countries, is already in the red flag zone and is catastrophic in a country that cannot mobilise more than 10 per cent of its GDP as revenue.

Whereas Nigeria borrows like a middle-income country, it earns like one of the poorest. Government officials dismiss the rising debt as a non-issue, but in the same breath, point to dismal, poor tax income as a challenge.

Of course, the debt-to-GDP ratio is less than 50 per cent in a global community that is grappling with nearly 240 per cent debt-to-output. Again, policymakers only hide under this deceptive metric, comparing the country with advanced economies, which can survive above 200 debt-to-GDP because of the robustness of their tax incomes.

For instance, the country’s tax-to-GDP ratio is only 10 per cent. Kenya’s debt-to-GDP is 71 per cent, but its tax as a percentage of GDP, at 17 per cent, is also much higher than Nigeria’s.

Ghana, a sub-regional peer, is also grappling with a debt-to-GDP ratio of above 70 per cent. But its tax revenue-to-GDP ratio is also far above that of Nigeria. The regional average of the index (tax-to-GDP ratio) is 16 per cent – six percentage points above that of Nigeria, which has taken 18 per cent as its target.

But the road to higher tax revenue is also fraught with constraints.

First, the country’s investment in infrastructure to increase the ability to pay (tax) of the economy is kneecapped by a heavy tax burden and bloated recurrent expenditure. Last year, the debt and non-debt recurrent expenditure was N19 trillion, as against N7.8 trillion disbursed for capital projects. This was not a random choice but a reflection of the government’s spending pattern. From 2020 to 2022, the total capital expenditure of the Federal Government was N19.3 trillion – less than 0.5 per cent of the $3 trillion yearly infrastructure deficit that Moody’s estimated in 2020.

Indeed, the growing cost of debt management means less funding for critical and growth-enhancing infrastructure such as power and road networks. This undermines the prospects of boosting company income tax (CIT) with the ongoing tax reform. The tax net, as some experts have warned, will not expand by a mere pronouncement of tax reform, but by a sincere economic recalibration that boosts the performance of economic agents and grows taxable incomes.

There are other channels through which the government’s debt accumulation inadvertently depresses the private sector, and the government hopes to leverage for higher tax revenue.

Indeed, the past decade has seen the government emerge as a dominant player in the local debt market, thus crowding out the private sector operators.

At its peak last November, net domestic debt to the government rose to N39.6 trillion – a staggering 55 per cent of the total credit to the private sector. About 10 years earlier – November 2014 – the ratio was 5.2 per cent. Then, credit to the private sector was N942.1 billion, showing how sharp the public sector debt indulgence has leapt in recent times.

Operators in the private sector need cheap and accessible credit to build more plants, create more jobs and increase tax revenue. But a growing list of requests from the government is a restraint. And it is worse that private businesses cannot compete with the government for funds as much as they can compete with themselves.

Of good numbers and weak appetite for change

SUCCESSIVE finance ministers had promised to “broaden revenue” and “control debt growth”. But the political class has no appetite for genuine change. Raising the value-added tax (VAT) to realistic levels, taxing the wealthy, and enforcing compliance on politically exposed firms are all avoided. Instead, Nigeria borrows domestically at punitive rates, pleasing banks but killing the real sector even as it borrows externally under undisclosed terms that compromise inclusive growth and suffocate future budgets.

While the government is pointing to improved revenue performance, some economists have also joined the fray. A former member of the Monetary Policy Committee (MPC), Prof. Adeola Adenikinju, summarily told The Guardian, “Nigeria is not broke”, leaning on the reported half-year revenue that shattered all historical records, growing by 40 per cent.

After churning out growth figures, Dr Chiwuike Uba, an economist, also concluded that “overall, Nigeria is not broke” even though its current financial status is fragile while the government operates under “severe fiscal constraints”.

“On the revenue side, there are encouraging signs. Between January and August 2025, non-oil revenues amounted to N20.59 trillion, representing a 40.5 per cent increase compared to N14.6 trillion during the same period in 2024. This reflects progress in broadening the tax base and reducing dependence on oil,” Uba, who has consulted for international development partners, noted.

David Adonri, another economist with a deep understanding of the dynamics in the debt market, also shared these views. With monthly “allocations to the federal and sub-nationals” expanding in nominal terms in the past few years and the government still up to speed with its financial obligation, being broke is overstating the fiscal strains.

This optimism often ignores the fast-growing contingent liabilities – same poison packaged differently.

The missing contingent liabilities

UNFORTUNATELY, the burden of governance is also severely understated. Today, power subsidy is one huge and poorly managed off-balance sheet liability that the government would need to confront sometime in the future. Like the fuel subsidy, there is no clarity on what the government owes in electricity subsidies, but different accounts estimate the figure in multiple trillions of naira. But the FG’s contingent liabilities transcend the power frontier. The last time that the government accounted for these implicit “debts” was during the administration of Buhari, when it was estimated at about N5 trillion.

Today, the government is indebted to all categories of public workers – frontline health professionals, primary school teachers, university lecturers, sportsmen and women and several others. These are debts by another name, with the current administration burdened with their full weight and significance.

But the fiscal vandalism often dressed up as governance is the government’s heaviest burden. When governance does not carry any sustenance beyond the next election, commitment to prudent resource management, fiscal discipline and public good take the back seat while elected official seeks extraversion, political expediency and clout, like when the president allocated some funds for some yet-to-be-created regional development commissions in anticipation in the 2025 budget – an appropriation still awaiting implementation three months left in its life.

Even with abundant expertise, programmes are sabotaged by choice, not by lack of capacity. Insolvency may be a financial misfortune, but if Nigeria falls into bankruptcy tomorrow, it will be the direct consequence of deliberate official choices—not chance.