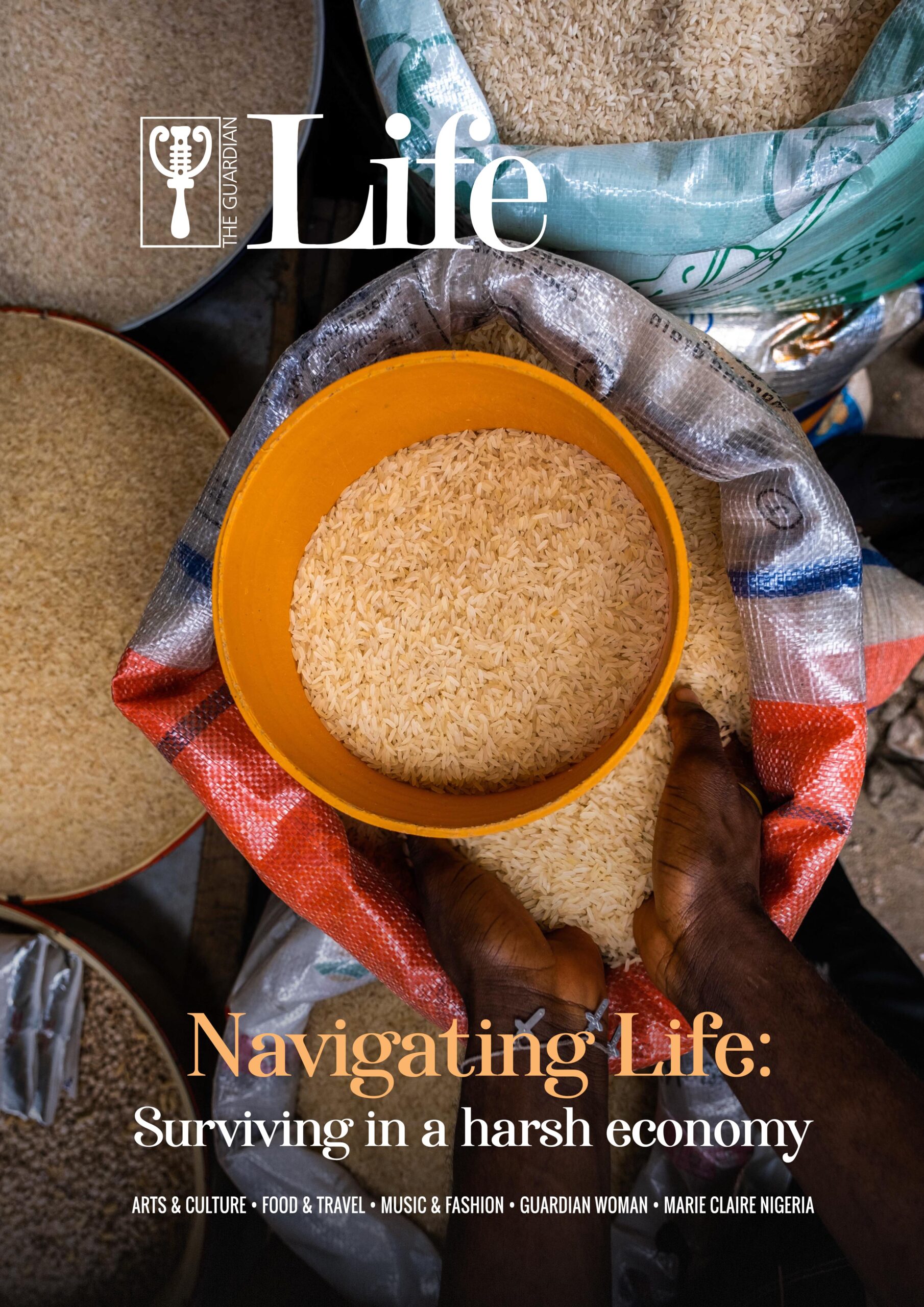

As inflation skyrockets and costs of living soar, individuals around the world—and particularly in Nigeria—are grappling with unprecedented financial stress. From trading in beloved SUVs for fuel-efficient cars to stretching salaries across multiple side hustles, people are devising new strategies for survival. In this cover story, CHIDIRIM NDECHE explores the roots of this economic crisis, examines its toll on everyday lives, and reveals how experts recommend navigating the storm to emerge stronger.

Rising costs, real lives

On a sweltering Monday morning in Lagos, 34-year-old Bukola* steps out of her cramped apartment and begins her daily race to the bus stop. Once accustomed to driving an older but beloved sedan, the steady climb in petrol prices has forced her to leave the car parked.

“I have a car, but it’s too expensive to drive now,” she laments. “Between high petrol costs and maintenance, it’s just not worth it when my salary hasn’t gone up.”

Bukola’s story illustrates the stark reality of countless Nigerians coping with inflation and limited earning potential. Owning a car, once a symbol of middle-class stability, now seems unattainable. Commuting has become a gamble, with buses and motorbikes overcrowded or charging unpredictable fares.

Beyond that, Bukola’s struggle is symptomatic of the broader frustration spreading across Nigeria, with inflation soaring to multi-decade highs—reaching 34.80 per cent in December from 34.60 per cent in November 2024. Petrol prices, previously around 195 naira per litre before President Bola Tinubu took office in May 2023, now range from 925 to 990 naira across various regions.

Inflation and reduced purchasing power

Multiple factors drive this inflation: supply chain disruptions, currency devaluation, and government policy changes. A key trigger was ending the fuel subsidy that had, for years, kept petrol costs relatively manageable. Additionally, free-floating the naira—originally intended to attract foreign investment—sparked significant currency volatility.

While economists and government officials maintain these moves are necessary for long-term sustainability, the immediate outcome has been shrinking disposable incomes and lowering purchasing power. More than 40 per cent of the population lives below the poverty line, and World Bank projections suggest numbers could rise further into 2025 before stabilising.

READ ALSO: Nigeria economy improving, will rebound in months – Shettima

Few aspects of day-to-day life remain untouched by the soaring costs of petrol, food, and other essentials. Private-vehicle commuters are increasingly turning to public transportation. Larger SUVs are often traded for smaller cars, and many cars remain parked. Car dealers report plummeting demand for bigger, pricier vehicles.

Meanwhile, traffic in major cities like Lagos has eased slightly, but this is no consolation to those who depend on private cars for mobility, family needs, or personal safety. In some parts of Nigeria, bicycles are making a modest comeback, though inadequate cycling infrastructure and the risk of accidents remain significant deterrents.

With electric power supply still largely unstable, homes, and businesses are shelling a large part of their disposable income and operation costs on alternative power supply.

“Food inflation rates can be traced to several factors,” explains Bunmi Bailey, Head of Research at SBM Intelligence. “Insecurity persists, affecting food production; energy costs inflate logistics costs; and naira devaluation pushes up import prices in a heavily import-dependent economy. Flooding and high farming input costs also hinder food production, and since production is low, prices remain high.”

Nnamdi Ehirim, the Head of Finance and Strategy at GoMoney, who closely monitors consumer behaviours, has observed significant shifts in people’s approach to finances.

“With the progressive nature of Nigerians, we see more people exploring ways to increase their income, either through education to give them a competitive edge in the job market, or quick-return investments, or even multiple sources of income.”

Side hustles on the rise

With salaries failing to keep pace with inflation, more people now juggle multiple jobs or side businesses to supplement their income. For instance, Bukola has taken on a weekend side hustle selling thrift clothing online to help offset her growing expenses. Some have started small-scale catering, digital freelancing, or e-hailing services to make ends meet.

“I used to think one stable job would be enough,” Bukola explains. “But inflation has eaten into my salary so much that I need another source of income.”

Families are cutting costs aggressively, often moving to cheaper neighbourhoods or sharing apartments. They cook in bulk, rely on cheaper protein sources, or cut out non-essential expenses like streaming services or gym memberships. Family outings, celebrations, and even small luxuries like coffee or snacks are now splurges.

Coping with the crisis

The financial strain exacts an enormous emotional toll, fuelling anxiety, depression, and chronic stress. Rising costs permeate nearly every decision—whether it is the type of milk to buy or whether to forgo medical checkups to save money. Conflicts in families over finances have become more frequent as financial pressures mount, and many Nigerians are experiencing burnout from working long hours across multiple jobs.

Ellar Gabriel, a therapist and psychologist, describes the mental toll: “There’s constant fear and anxiety: ‘I don’t want to fail; I have to provide.’ So because of this fear, people end up picking a lot of jobs. Imagine someone juggling work in a bank, doing virtual assistant tasks, and still running a catering business. There’s going to be so much heightened stress, leading to burnout, fatigue, and physical and mental strain. Because money is tight, self-care becomes a luxury because they’re just trying to survive.”

Burnout and fatigue are everywhere. However, people see therapy or even a spa date as optional because they’re just trying to survive. Nonetheless, self-care is crucial, whether it’s scheduling a fun activity once a month or seeking out free or subsidised counselling from NGOs.

READ ALSO: Work from home, gig economy and future of work

Personal finance experts urge strict budgeting, known as zero-based budgeting, where every naira is allocated and planned properly before the month begins. They also encourage automated savings, however small, to cushion short-term financial shocks. But that is also an arduous task.

“In general there has been a reduction in savings due to inflationary reasons,” says Ehirim.

In the current climate of uncertainty, these experts advise looking into stable, low-risk investments like government bonds or mutual funds, which can help preserve capital amid relentless inflation.

For some families, cost-cutting measures are now a priority.

“We do bulk purchases for essentials and everything else we need for the month, from meat to toiletries,” says Itoro Oladokun, a mother of two. “We also avoid eating out. Though we used to do that twice a month, I can’t remember the last time we did it because it takes a lot from my purse. During festive periods like Christmas, I buy pure water so I don’t spend so much on water.”

In addition, psychologists and therapists recommend mindfulness techniques—such as deep breathing exercises, journaling, and guided meditations—to manage stress. Seeking support from friends, family, or professional counsellors can also mitigate feelings of isolation. They also advise limiting exposure to alarming economic news.

Informal, community-based savings groups, known locally as ajo or esusu, provide valuable lifelines to many by pooling resources and offering mutual support. They help individuals weather immediate financial storms and foster a sense of collective resilience that could prove essential in the long run.

What’s the future saying?

Despite the grim outlook—double-digit inflation, sky-high petrol prices, and a cash crunch—many Nigerians remain resilient. They believe that current reforms, though painful, could eventually spur growth. As more mobile money agents enter the market, fees may drop due to increased competition. Similarly, as local businesses pivot to meet evolving consumer needs—like offering cheaper, more durable products—household budgets may find a new equilibrium.

Ehirim points to incremental positive signs: “Early indicators suggest incomes are increasing—no matter how little—because employers are adjusting to the changes. We can also see the effects of foreign exchange rates getting more favourable. With the government prioritising non-oil revenues, we’re expected to see an influx of more forex revenue, which would have a significant impact on the economy and, in tandem, ease the economic pressures.”

Ultimately, navigating life and surviving in a harsh economy demands flexibility, resourcefulness, and collective support. From disciplined personal finance to innovative mental health strategies and supportive government policies, multiple factors must align for true relief. While the road remains steep, many Nigerians—and others in similar situations—are forging new paths toward stability, offering hope that they can not only navigate these pressures but also emerge stronger.

*Name changed for privacy