• Naira breaks N1500/$ barrier first time since June 2024

• Naira breaks N1500/$ barrier first time since June 2024

• Foreign-dominated investments see rise in liquidation

• Investors dump dollar-assets as ‘buy Nigeria’ gains traction

• Boggled BDC reform poses near-term regulatory risk

The consistent appreciation of the exchange value of the naira has sent a shockwave through the foreign exchange (FX) market, especially among the parallel segment traders who are wary of being trapped in a replay of last year’s March/April positive feedback loop.

With the naira coasting home with a bullish run, it started the year with, there are fears that the currency could be in for a sustained appreciation that could trim off a substantial value from the net worth of FX portfolio holders.

The gradual appreciation of the local currency in the past two weeks has inflicted significant losses on black market traders with some expert assessments already putting the total financial loss at between N10 and N20 billion.

The Guardian learnt that many traders who warehoused hard currencies ahead of January when high demand by Nigerians in the diaspora (who are returning to Europe and America) historically pushes up the exchange value have got their hands burnt.

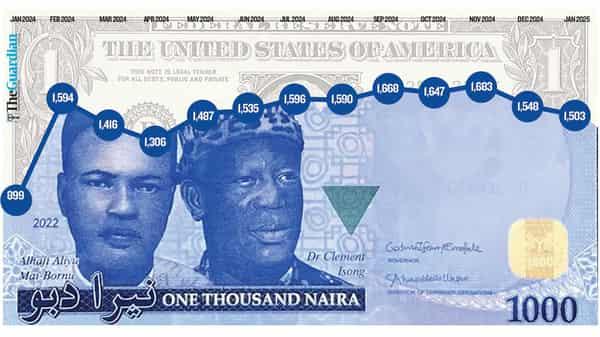

As of last weekend, sources said they were convinced that January and February had turned out to be a winter market for the dollar, as those with substantial volume started dumping holdings, triggering a rally by the local currency from about N1600/$ last weekend to about N1560/$.

It would be the first time in about eight months that the naira would rise above the N1600/$ mark. The currency had traded between the N1600 and 1,800/$ band for eight months until last weekend.

At the official market, the dollar also dropped below N1500/$ during last week’s trading sessions. It was the first time the naira would break the psychological ceiling, which marks a N1,400 exchange value is no longer a remote possibility.

The first halves of quarter one (Q1) are not particularly the months of naira. During the pegged era, the parallel market saw enormous pressure owing to a spike in demand from returning Nigerians.

Last year, the first time the pro-market era was tested, the naira lost about 43 per cent of its value from January to late February when it peaked at below N1600/$ before the March/April breather.

But so far, the dollar has lost about N100 or six per cent against the naira at the parallel market, falling from the yearly open range of N1660-1640/$ to last week’s 1550/$ closing. It also lost about N40 in the official window. The market, according to data by FMDQ, has traded at an average of N1,476.74/$.

The rebound of the local currency is being interpreted differently. The pessimists view it as a dead cat bounce, suggesting that it is a momentary recovery that would be wiped out when the depression resumes.

For instance, Comercio Partners, which unveiled its 2025 Macroeconomic Outlook, says the currency would end at N1800/$ by year-end – a 20 per cent deviation from the current market position.

But the majority, including some international research organisations, believe the gain is part of the broader correction and fair value discovery expected of the currency after two years of debauchery.

At a Lagos Business School Breakfast, the Chief Executive of Financial Derivatives Company (FDC), Bismarck Rewane, put the market value at N1107/$, suggesting it is trading about a quarter less than its true value. Rewane used purchasing power parity analysis, which discounts largely market sentiment.

Whatever the case, there seems to be a consensus among economists that naira is trading below its fair value. Even those who think the naira will lose this year agree that the naira is much cheaper than its true exchange except that they are not the currency that is ready for a sustained bull run this year.

In the short run, the market dynamics favour the naira. First, whereas the central banks of the developed world are winding down the long-running quantitative tightening, the Monetary Policy Committee seems committed to a sustained high-interest rate regime. On different occasions, the Central Bank of Nigeria (CBN) noted that it is not in a hurry to start loosening.

Projections suggest the authority could tarry till the last quarter before the first rate cut in over three years. Sources privy to MPC members’ thinking said the projections favour hold in the two to three meetings as the committee would need time to study global moves.

The January meeting was reportedly postponed to February, enabling the committee to factor in the expected rebased output and inflation level into the decision. Report another reschedule is being considered.

Since Donald Trump-instigated tariff war, inflation has become a major strand of the emerging international economic issues. With the concern building on the possible price uptick for the umpteenth time, some experts have suggested that the Federal Reserve will be forced to hold back any rate cut that would add to inflationary pressure.

Nigeria’s 12-month bond yields are close to 20 per cent. If inflation slows to less than 15 per cent of the rebased figures, real returns could return to a positive curve to give fund holders reasonable comfort.

If that happens, foreign portfolio investment (FDI), which is currently riding on the ‘Buy Nigeria’ campaign will continue to pour in to sustain the current liquidity level.

Locally, FX balances held by both commercial and investment banks are dwindling with many investors said to be taking positions in naira-denominated assets.

A bank source who spoke with The Guardian, yesterday, said calls on dollar savings have increased significantly since the beginning of the year. Our correspondent could not independently verify the claim, but insider sources said the attraction of saving in dollar accounts is on reducing balances with many people moving their money out to take positions in equities and other naira assets.

Even with some investment banks increasing their interest in dollar-saving products, a senior executive in one of the banks put the year-on-year (Y/Y) growth on a popular product at -40 per cent.

The source, who claimed the products have become a hard sell, told The Guardian: “Those who invest in them are constantly looking for a way to hedge against the risk of holding naira. But if holding the dollar is considered riskier even if what you consider is the short-term horizon, people will be wary of converting the naira to the dollar. Even when you offer 10 per cent interest, if the dollar falls to N1,200/$, they will be in a loss position.”

Another source disclosed that matured lock-ins have seen an unusual spike in liquidation as against the previous trend where they were rolled over. Asked whether the naira gain is not just correlated to asset liquidation without little or no causal relationship, the source said most investors rarely quit an investment window if they do not perceive there are more rewarding options.

Some investors might have divested from dollar-denominated assets or reduced the FX balances held in commercial banks as savings to take positions in bank equities ahead of the recapitalisation.

At the weekend, Fidelity Bank Plc said its public offer was oversubscribed by 238 per cent, raising N23.77 billion for its recapitalisation campaign.

Seven banks, which had concluded their processes earlier, raised a total of N1.3 trillion, The Guardian reported. Three out of the five systemically important banks (SIMs) – Access Bank, GTBank and Zenith Bank – raised jointly about N911 billion. Capital raised by UBA and First Bank of Nigeria may increase the total pool by the big five to over N1.5 trillion – from the market sceptics earlier said was overtasked to provide the fresh CBN capital call.

Indeed, it is a momentary triumph for the naira – thanks to some working policies, growing pro-Nigeria sentiment, bank capitalisation effect and many other factors. Still, the long-term outlook seems better on account of both endogenous and endogenous variables.

First, growing crude refining is cutting down the volume of FX needed for import even as the country is working on leveraging value chain development across sectors to improve its terms of trade.

On the external side, the dollar-naira exchange value index may have passed its peak. First, the network effect, a major strand of the dollar dominance is being punctured by the growing friends of BRICS, an economic bloc formed based on reducing the power share of the dollar. With the recent enlisting of Indonesia and Nigeria (as a partner member), the bloc now controls well over 50 per cent of the population.

More importantly, the bloc accounts for nearly 40 per cent of global gross domestic product (GDP) when measured on PPP, signalling the ascendancy of the anti-dollar reign, which Trump threatened to impose a 100 per cent tariff on before he assumed office.

Long before BRICS started gaining momentum, the dollar as a reserve currency had been sliding, from over 80 per cent a few years ago to 59 per cent. It currently serves as the dominant global means of exchange, but other currencies are also rising with 27 per cent of total trade in Chinese goods settled in the renminbi last year, according to data.

Today, the persistent external deficits of the United States have left it with substantial foreign liabilities. About 40 years ago, the Supper Power was a net creditor to the rest of the world. But it now owes foreign lenders to the tune of $20 trillion, estimated at around 70 per cent of its GDP.

These leave the dollar with significant vulnerability to other currencies, including the naira. Whereas these challenges faced by the dollar, including the huge supply, may not directly benefit naira in the nearer terms, they may indirectly reduce the decaying effect the greenback has on the local currency and change the market sentiment to the advantage of naira.

Interestingly, the naira gain is coming at a time when the dollar is at its strongest point since November 2022. As of press time, the dollar index (DXY), a metric that measures the relative strength of the currency, was at 108 points, a marginal decline from 109.5 points, where it peaked in January on the Trump assumption.

The new administration, headed by an individual with a significant reputation for impulsive policy choices, is already being considered as bad news for the dollar. If the global currency reverts to its five-year average (which will be about 100 points) in the life of the administration, it could lift the value of naira above its current exchange value relations.

But, in the meantime, the local currency faces tough challenges, including the political will and capacity of the regulator to stay his course. The planned implementation of the reform in the Bureau de Change (BDC) market and checking its excesses is a near-term test of the CBN’s commitment to broad market reform.

As part of the reform, tier-1 BDCs are expected to raise their minimum capital to N2 billion while tier-2 will increase to N500 million. However, the regulator seems to be hesitant with the implementation of the consolidation with the initial deadline already shifted. The exercise, market watchers have observed, would rein in anti-market activities and enhance regulation.