• Spike in public spending pushes CBN to hike interest rate to 26.75%

• Blames energy insecurity, middlemen for high food prices

• We are working with fiscal authorities to tackle inflation, says Cardoso

• Public spending may exacerbate money supply

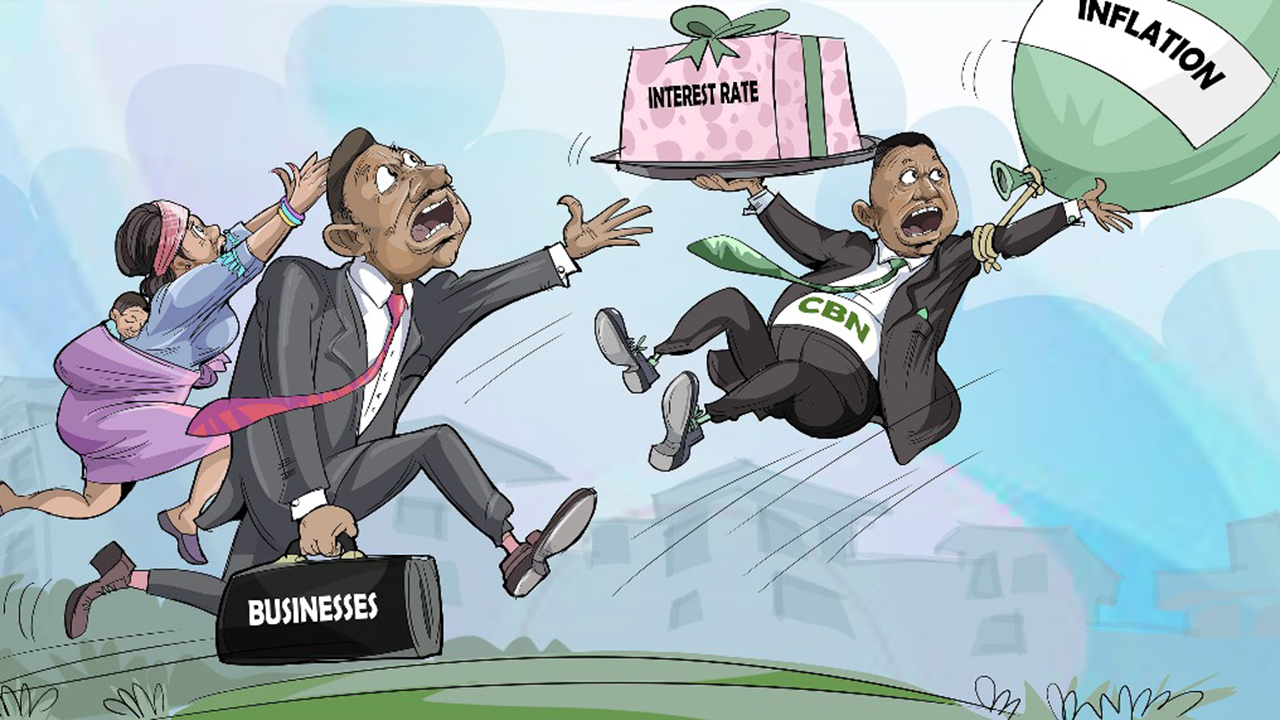

With help from the fiscal authorities slow in coming, the cost of borrowing is set to spike further as the Central Bank of Nigeria (CBN) has added 0.5 per cent to the already high monetary policy rate (MPR), taking it to a new height of 26.75 per cent in a bid to tame inflation.

While the MPR increase is moderate, the standard lending facility (SLF) rate, which determines the cost at which the CBN lends to banks, has been raised generously, from MPR plus one per cent to MPR plus five per cent.

That implies that unlike before, banks that have run into short-term liquidity shortfalls will borrow from the apex bank at 31.75 per cent. Previously, the rate was 27.25 per cent.

Also, banks would get higher interest from depositing excess liquidity at CBN through the standard deposit facility (SDF). Henceforth, banks would get 25.75 per cent from ‘lending’ to the apex bank.

Both scenarios would increase illiquidity and increase the cost of lending in the coming months. The Guardian had earlier reported that the transfer of dormant account proceeds would reduce the money supply by about N20 trillion, leaving the economy more starved of liquidity and raising the competition for funding.

At the end of the CBN’s Monetary Policy Committee (MPC) meeting in Abuja, yesterday, the governor of the CBN, Olayemi Cardoso, said the MPC adjusted the asymmetric corridor around the MPR from +100/- 300 basis points (bps) to +500/-100bps.

No explanation was given for the adjustment of the parameter, which explains the lending relationship between the regulator and banks. The liquidity ratio was retained at 30 per cent. The cash reserve ratio (CRR) of deposit money banks (DMBs) at 45 per cent and merchant banks at 14 per cent were all retained.

The governor said while the monetary and fiscal authorities are collaborating to halt inflation, insecurity, energy costs and middlemen play major roles in the high cost of food prices.

He added: “In its consideration, the Committee noted the persistence of food inflation, which continues to undermine price stability. It was observed that while monetary policy has been moderating aggregate demand, rising food and energy costs continue to exert upward pressure on price development.

“The prevailing insecurity in food-producing areas and the high cost of transportation of farm produce are also contributing to this trend. Members were, therefore, not oblivious to the urgent benefit of addressing these challenges as it would offer a sustainable solution to the persistent pressure on food prices.

He noted that there is an urgent need to put in check such activities to address the food supply deficit in the Nigerian market to moderate food prices. He added that the MPC resolved to sustain collaboration with the fiscal authority to ensure that inflationary pressure is subdued.

The committee expressed optimism that the 150-day duty-free import window for food commodities would moderate domestic food prices. “However, we were quick to caution that the step measures will not lead to direct injection of liquidity into the economy as to cause further inflation,” he said.

The MPC’s decision, as reported by The Guardian, may have taken into consideration, the implementation of the new minimum wage, which was approved by the Senate yesterday.

The minimum wage has been reviewed upward by 133 per cent, from N30,000 to N70,000. There are fears that the increase could cause a demand shock that could worsen inflation concerns.

The 50-basis points hike did not come to the Chief Executive Officer, Centre for the Promotion of Private Enterprise (CPPE), Muda Yusuf, as a surprise.

He observed that the step is a moderation in its aggressive tightening stance, adding that it is also a reflection of its responsiveness to the clamour by stakeholders in the real economy.

Yusuf stated that his preference was for a pause on the rate increases because of the enormity of the headwinds that businesses are grappling with, but the marginal increase marks a softening of the tightening stance. It is tolerable.

“I believe we should now accelerate the implementation of the fiscal policy measures to tackle inflation. Already the economic stabilisation plan contains some laudable fiscal policy measures that could reduce production costs in the economy.

It is also important and urgent for the government to adopt and quickly implement the recommendation of the Presidential Committee on Fiscal and Tax Reforms on the Customs duty exchange rate which proposed N800/dollar. The adoption of this recommendation would have a considerable impact on the cost of goods and services in the country,” he explained.

An economist, Kelvin Emmanuel, said the real issues driving inflation are shortage of supply in the real sector and excessive money supply. While economists believe that the new wage is likely going to worsen inflation, recent data suggests otherwise.

In 2019 after the wage moved from N18,000 to N30,000, the inflation rate remained around the 11 to 12 per cent band. In July, two months after the bill was passed, inflation slowed to 11.08 per cent.

However, it must be noted that the 2019 increment was around 66.7 per cent while a jump from N30,000 to 70,000 is over 130 per cent. Emmanuel argued that other than preventing the capital flight from naira to USD-denominated assets, the CBN also needs to make yield attractive in open market operation (OMO) instruments for mopping up excess liquidity, which is the reason the rate went further up.

“I don’t think there is a quick or immediate silver bullet, especially considering that in terms of energy and food security, the government is unable to provide primary input for commercial refining as well as provide the framework that will catalyse an increase in the production of key inputs for food processing.

“I however believe that it’s important for the MPC to adopt a model where CRR is determined by the performance of the LDR of banks,” he said.

A financial analyst, Abubakar Umar, said the slight rise in MPR is influenced by the marginal upward movement of inflation in June. He said: “My sentiment is for CBN to retain the current MPR but with the inflation data released by NBS this month, it swayed the sentiment of the committee members to vote for a little increase in the MPR.”

He lamented that businesses are already suffering under the yoke of high cost of borrowing and high energy costs. He refrained from blaming the CBN for taking the rate up by another 50 basis points, saying: “Businesses are suffering, the economy is harsh, but this is a choice between the devil and the deep blue sea, CBN option is only to increase and retain to preserve the financial market and keep its activities afloat.”

He agreed with Cardoso that the fiscal authority’s support is needed to tame inflation.

“Of course, many people agreed that MPR alone cannot moderate or reduce inflation, but it’s a necessary tool to preserve the value of the currency, reducing the MPR – popularly to what people want to hear – can destroy the financial market and reset all the reforms being done by the CBN,” he said.

He insisted that while the apex bank is on the right track, the fiscal side seems not to be at their duty posts. Prof. Godwin Oyedokun of Lead City University said the government needs to address the fundamental issues causing inflation, adding that using only monetary policy instruments to check inflation will not work. He noted that the more they increase the interest rate, the more it is difficult for businesses to access funds to do business.

“If a businessman borrows at a high interest rate to produce, he will most definitely pass on the extra cost to the consumers, which invariably increases the price of the goods,” he said.

On his part, Prof. Uche Uwaleke of Nasarawa State University said: “Having done 750 basis points between February and May this year, I had predicted they would do a minimum of 50bps or a max of 100bps in July. I am glad to note that they chose the floor, which is a sign that a complete halt is most likely in their next scheduled meeting in September. But the adjustment to the asymmetric corridor around the MPR is a major source of concern for me.” He noted that the MPC communique did not provide any explanation for increasing the SLR from +100 to +500 and the SDR from -300 to -100.

“By implication, with an MPR of 26.75 per cent, banks will now get loans from the CBN at 31.75 per cent while they will be remunerated for their excess deposits at 25.75 per cent. This will further squeeze liquidity from the banking system and jerk up the cost of credit with adverse consequences on output and the equities market.

“The MPC communique should have made it clear why it was better to mask the tightening in the asymmetric corridor than reveal it in the MPR. “May I observe that, unlike previous MPC communiques, recent ones are silent regarding how the members voted? This information is useful at this stage even before their statements are published. I submit that as far as taming the current elevated inflation in Nigeria is concerned given its major non-monetary drivers, the fiscal side holds the ace.”

The National President of the Nigerian Association of Chambers of Commerce Industry Mines and Agriculture (MACIMA), Dele Oye, had, in a statement, raised the alarm that further increases in the interest rates introduce higher costs and increase uncertainty for businesses which can have a range of negative impacts on their operations and growth prospects.

He said some consequences include increased cost of borrowing and reduced investment as well as decreased consumer spending, which impact cash flow. Similarly, the Manufacturers Association of Nigeria has expressed grave concern and called for caution from major actors, government agencies and regulators in the oil and gas sector of the economy over the recent debunked allegations of poor quality of diesel leveled against one of the largest private investments in Africa by NMDPRA, the Dangote Refinery.

According to Director General of the Association, Segun Ajayi-Kadir, mni, it is expected that agencies of government, that provide regulatory oversight functions should promote an enabling business environment for local investments to thrive. No regulatory agency should be seen to be casting a shadow over a homegrown investment like the Dangote Refinery.

“The allegations of poor quality, monopolistic tendencies and non issuance of license have since been roundly debunked. There may then be the need to issue a clarification that absolves the Dangote Refinery of the negative perception generated by the news report,” he said.

Ajayi-Kadir further stressed that local investors in Nigeria, particularly the Dangote Industries Limited (DIL), play a vital role in driving economic growth, they pay taxes, they create jobs and foster development within the country.

“As such, it is important that these investors are protected and given the necessary support to thrive in this business environment. He said a business colossus like Alhaji Aliko Dangote, with investments in diverse sectors of the economy and across the Continent of Africa, should be accorded all needed support to grow and invest in more sectors and positively impact the wellbeing of the people,” he said.