• As output surpasses World Bank, IMF projections

• Self-employed jobs jump to 85.6 per cent

• Rising debt poses major risk to private sector growth, says Muda Yusuf

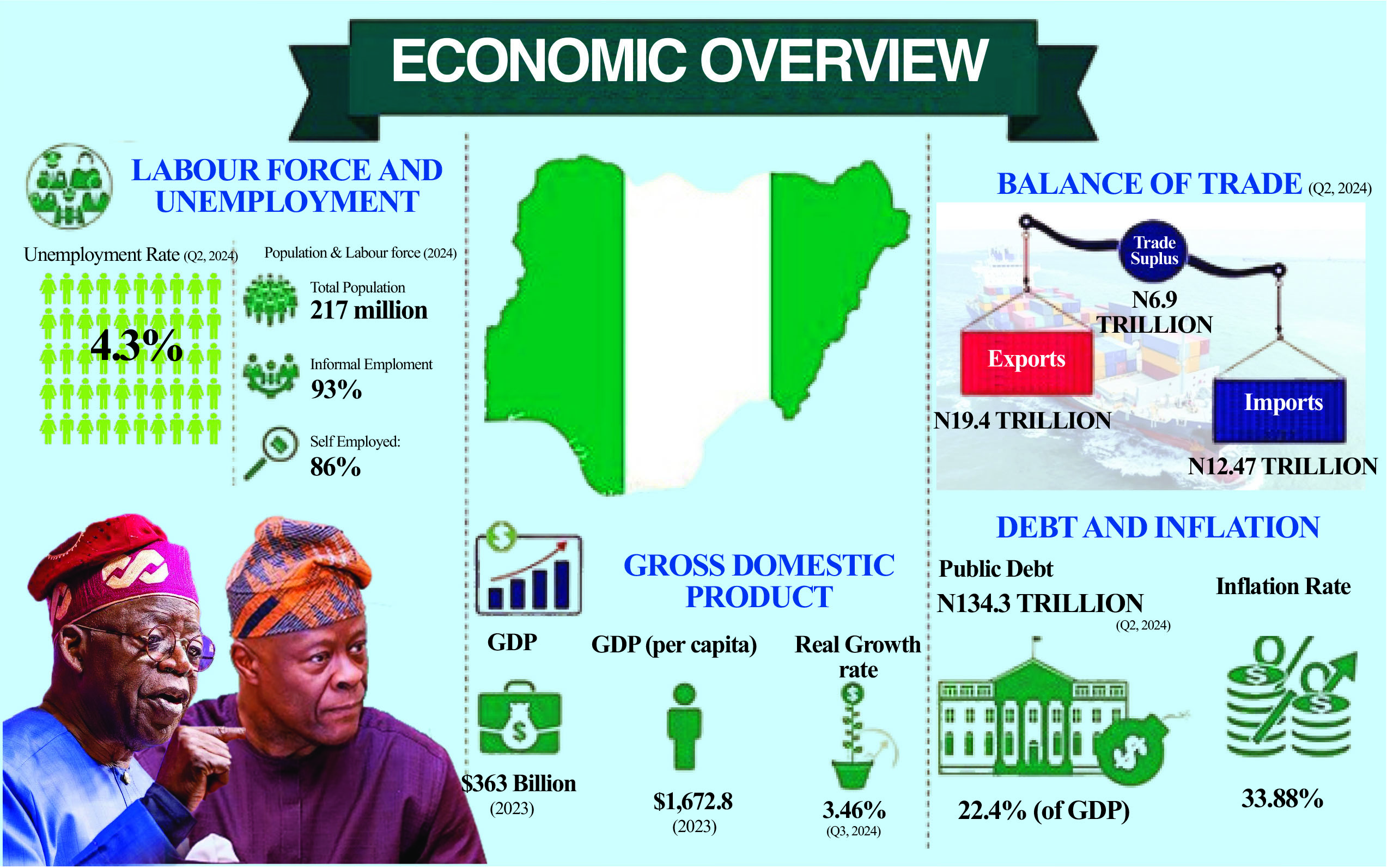

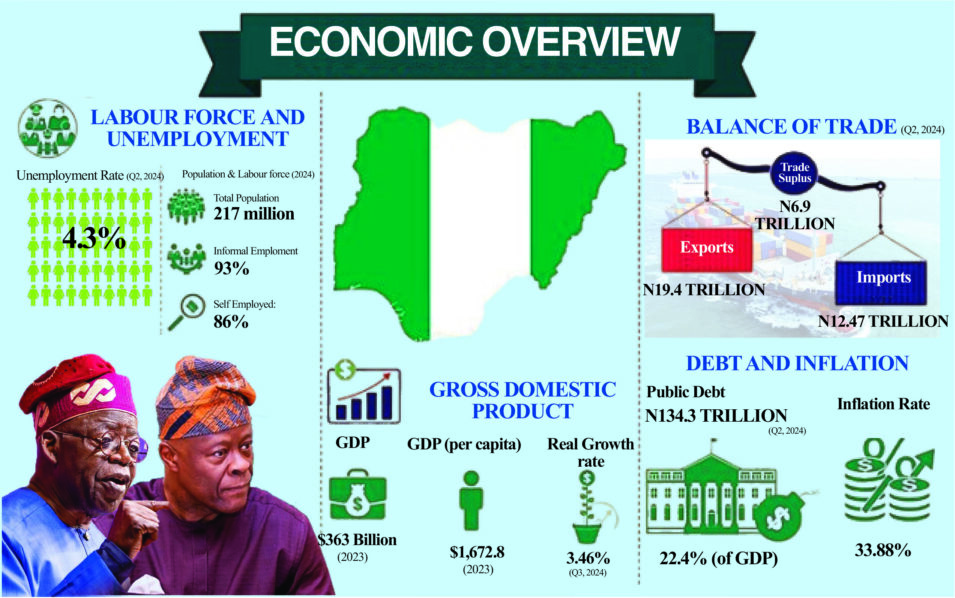

Notwithstanding the high inflation rate, rising interest rates and company closure, escalating energy, insecurity and several other headwinds have impacted the economy, the National Bureau of Statistics (NBS) said the country has defied projections to grow faster at 3.46 per cent and lower unemployment of 4.3 per cent in the second quarter.

At 4.3 per cent, Nigeria’s unemployment sits comfortably in the region of what economic theorists consider a normal or natural rate of unemployment and far below the global average, which closed last year at 5.1 per cent.

The labour data aligns with the gross domestic product (GDP) performance data for the third quarter, which was released yesterday by the NBS.

According to the data, the economy expanded 3.46 per cent overall. But the growth was mostly driven by the service sector with the inclusive sectors such as agriculture growing at less than average.

Like labour, the output performance, which outperformed projections by the International Monetary Fund (IMF), the World Bank and other research institutions, was contrary to market expectations.

Other data covering the same Q2 suggest the economy has continued to slide. For one, the Manufacturing Association of Nigeria (MAN)’s half-year (HI) report said capacity utilisation fell to 56.4 per cent in the period just as inventory saw the sharpest surge in recent years – rising by over 350 per cent to N1.24 trillion. A growth that suggested many manufacturers might have downsized workers as a coping strategy.

In line with expectations, the report disclosed, job creation fell by 37.8 per cent in the period with only 2,606 jobs created. The report was silent on the number of jobs lost in the period. But within the same period, Kimberly-Clark and many other manufacturing giants, closed shops throwing thousands of employees back to the labour market.

The corporate failure, which many believe would have increased the burden of unemployment, was worsened by the rising risk level, with insecurity compounding the crisis. For the first time in decades, the inflation rate, which is worsened by fuel subsidy removal and foreign exchange reform, has crossed the 30 per cent mark.

Interest rate has also reached an all-time high with maximum lending rate spiking to 30.28 per cent as of October. Experts have suggested that these are sufficient reasons to believe the number of jobless Nigerians has reached a new high and growth momentum sapped.

But against the odds, growth has firmed up to nearly 3.5 per cent while the unemployment rate also decelerated to 4.3 per cent. Both data were released yesterday, emboldening the current administration, whose reforms have come under criticism.

President Bola Tinubu on Monday said Nigeria is on track to becoming a $1 trillion economy by 2030, going by the recent GDP data.

The President said this performance once again shows that the reforms embarked upon by the Tinubu administration to reposition the economy and ensure better fiscal management are beginning to yield fruits.

The NBS reported that Nigeria has recorded more employment and reduced its unemployment rate to 4.3 per cent in Q2, contrary to MAN data.

The NBS’s Nigeria Labour Force Survey (NLFS) report for the second quarter of 2024 reported a drop in the unemployment rate from 5.3 per cent in the first quarter to 4.3 per cent.

This figure suggested that only about four people out of every 100 Nigerians are currently unemployed. However, considering the data that indicated a higher unemployment rate, experts have disagreed with the NBS, arguing that it fails to acknowledge the severe joblessness crisis in Nigeria.

The Assistant General Secretary of the Nigeria Labour Congress (NBS), Chris Onyeka, expressed disappointment with the NBS’s unemployment data, claiming that it is manipulated and not useful for planning. He lamented that all macroeconomic variables across the board are experiencing a downward trajectory.

Onyeka questioned how the unemployment rate could be decreasing while factories are closing, and businesses are reporting unsold inventories. He criticized the NBS for presenting this data as “voodoo disclosure” and “propaganda,” arguing that it serves only to mislead Nigerians.

The Deputy President of the Trade Union Congress of Nigeria (TUC), Dr Tommy Okon, also criticised the data, stating that the methodology used to arrive at the figure is not transparent.

Netizens have also criticised the bureau, accusing it of transforming into a new propaganda tool, producing unrealistic data.

An X user, @RanchoMedici, pointed out that the data is political and should be verified in the streets.

The report showed a rise in the labour force participation rate among the working-age population from 77.3 per cent in Q1 2024 to 79.5 per cent in Q2 2024, indicating increased workforce engagement.

The employment-to-population ratio also improved, climbing from 73.2 per cent in Q1 2024 to 76.1 per cent in Q2 2024, suggesting a higher proportion of the working-age population was gainfully employed.

Self-employment remained dominant, accounting for 85.6 per cent of total employment, an increase from 84 per cent in the previous quarter. The number of self-employed raised concern about the quality of jobs NBS’ new methodology considers in its report.

When people lose their jobs and there is no hope of getting new ones, they take to self-employment and are classified as employed even when their incomes can hardly take care of their basic needs.

The same argument goes for informal employment which also rose slightly to 93 per cent highlighting the economy’s reliance on informal jobs.

Urban unemployment decreased from six per cent in Q1 to 5.2 per cent, while rural areas recorded an even lower unemployment rate of 2.8 per cent, compared to 4.3 per cent in the previous quarter.

This disparity underscored the continued significance of agriculture and informal activities in rural employment, contrasting with the urban dependence on formal and service-oriented jobs.

The report also revealed gender disparities, with the unemployment rate for females at 5.1 per cent compared to 3.4 per cent for males, suggesting the need for targeted gender-inclusive policies to address the employment gap.

Unemployment, a component of labour underutilisation, rose to 4.3 per cent in Q2 2024, a 0.1 percentage point increase compared to the same period last year. Males accounted for 3.4 per cent of the unemployment rate, while females made up 5.1 per cent.

The unemployment rate varied according to places of residence. Urban areas had a rate of 5.2 per cent, while rural areas had a rate of 2.8 per cent. Notably, the youth unemployment rate decreased from 8.4 per cent in Q1 2024 to 6.5 per cent in Q2 2024.

Also, time-related underemployment, which measures workers seeking additional hours, decreased to 9.2 per cent in Q2 2024 from 10.6 per cent in Q1.

While the government is celebrating the positive signs, the Chief Executive Officer, Centre for the Promotion of Private Enterprise (CPPE), Dr Muda Yusuf, has warned that the increasing debts may have crowd-out effects on the private sector and worsen the performance of the economy.

In his reaction to the mounting debts, Yusuf noted that a situation where the private sector is unable to compete with the government within the financial space is uncomfortable to him.

“We are beginning to see a situation where the private sector cannot compete with government in the financial market because government borrowing is generally with minimum risk, so many investors would rather invest in government securities rather than corporate bonds. Even financial sector operators want to invest their funds in treasury bills and federal government bonds,” he explained.

He warned that Nigeria is gradually moving capital away from the real economy, which could be disastrous.

He added that this kind of macroeconomic condition also leads to further tightening of monetary policy, saying increasing deficits lead to higher inflation, which in turn elicits a tight monetary policy response from the central bank.

His argument: “When this happens, it is the private sector operators that suffer because they are the ones that borrow money to invest and are currently owing the banks. This is why interest rates are now above 35 per cent, and it’s a lot of pressure and burden on private sector investors. High interest rates also could trigger an increase in non-performing loans, which is not good for the banking system or for those who borrowed money from the banks.”

He decried the addition of about N132.4 trillion to Nigeria’s debt between 2015 and 2024 under the leadership of the All Progressive Congress (APC).

“In 2015, our total public debt was N12.6 trillion, and in 2024, our public debt alone, as of June 2024, was N134 trillion, an over 900 per cent increase.”

According to him, the government does not have tangible achievements to justify the huge borrowing.

Yusuf argued that debts collected are supposed to rebuild the capacity of the economy to repay accumulated debts, which has not been the case with Nigeria.

“The use to which these debts are committed is very important in evaluating the quality of debts or their sustainability. Furthermore, we need to worry about the sustainability of the debts, and two factors are critical here: the cost and tenor of the debts. The interest rates at which the government procures some of these debts are extremely prohibitive,” he stated.

He expressed worry about the tenor of the foreign debts, saying: “For multilateral and bilateral debts, tenors are much longer, which would have been good if we didn’t have our current FX situation and our currency wasn’t this badly depreciated. But with the current volatility in the exchange rate, the less exposure we have to foreign debts, the better for the economy and debt sustainability.”

He, however, expressed cautious optimism at the slight reduction in external debt, adding that in June 2023, total external debt was $43.2 billion and in June of this year, this had reduced marginally to $42.9 billion.

He urged caution concerning expenditure and optimisation of revenue to prevent the economy from suffering economic overheating.

Nigeria’s public debt, including external and domestic debt, stood at N134.30 trillion (US$91.35 billion) in Q2 2024 from N121.67 trillion ($91.46 billion) in Q1 2024, indicating a growth rate of 10.38 per cent on a quarter-on-quarter basis.

This is according to data sourced from the NBS. It went on to add that total external debt stood at N63.07 trillion ($42.90 billion) in Q2 2024, while total domestic debt was N71.22 trillion (US$48.45 billion).